6. Research Plan

To achieve the objectives of the research, it is divided into the following sections: -

6.1. Factors Affecting the Impairment in the Value of Fixed Assets

The international: No. (36),

| [16] | Kurt H Buerger, Linda M Nichols. “Accounting for im-pairments: Domestically and internationally” Oil, Gas & Energy Quarterly. New York: Jun 2001. Vol. 49, Issu. 4; pg. 839. |

[16]

and Egyptian: 31, standards for impairment in the value of assets refer to the definition of impairment as the amount of decrease in the recoverable value of the fixed asset from its book value

| [17] | Emanuel Bagna a b, Enrico Cotta Ramusino a b, "The impact of different goodwill accounting methods on stock prices: A comparison of amortization and im-pairment-only methodologies", International Review of Financial Analysis. Volume 85, January 2023. |

[17]

. To know this impairment, the standard requires a re-evaluation of the assets at the end of the fiscal year to determine the decline in their value for joint, sister or subsidiary projects, and for assets that are recorded in the books based on re-evaluation. Therefore, the meaning of impairment is a decline in value, that is, the disappearance of the value of the asset, and where the limitations of the study are the impairment of fixed assets only, which are defined by International Accounting Standard No. (16) and Egyptian Standard No. (10) as tangible assets that:

The company keeps them to use them in producing or providing goods or services, or to rent them to others or for their administrative purposes.

Expected to be used for more than one accounting period.

Therefore, the focus will be on the factors affecting impairment in the value of fixed assets only, as will be stated in the following subsections in the body of the research:

Factors affecting the estimation of use value

| [18] | Derarca Dennis. “Accounting for Impairments: A Prac-tical Guide” Accountancy Ireland. Dublin: Dec 2008. Vol. 40, Iss. 6; pg. 26, 3 pgs. |

[18]

.

1) Estimating the future cash flows that the entity expects to receive from the asset.

2) Expectations regarding changes in the values or timing of future cash flows.

3) The time value of possible money is represented by current market interest rates without risk.

4) The responsibility of the uncertainty inherent in the asset value.

5) Other factors such as the ability to liquefaction and filtering, which the market shows when determining the value of future cash flows that the entity originally expects to receive.

Factors that must be taken into consideration when estimating the use value

| [19] | Laurence Rivat. “Are your assets impaired?” Account-ancy. London: Jul 1998. Vol. 122, Iss. 1259; pg. 90, 1 pg. |

[19]

.

1) Estimating cash flow expectations based on reasonable and supported assumptions that represent management's best estimates.

2) The assessment is made considering the latest budgets and forecasts approved by management (excluding any future cash flows in or out that are expected to arise from restructuring in the future or from improving or supporting the performance of the asset).

3) Estimating expectations for cash flows beyond the period covered by recently issued budgets and forecasts approved by management.

4) Estimating expectations for cash flows beyond the period covered by recently issued budgets and forecasts for a maximum period of five years (or longer if it can be justified).

5) Expectations are estimated based on a constant or declining growth rate.

6) Growth rates should not exceed the average rates in the long term for products, industries, or the country in which the facility carries out its activity.

Indicators of decline in the value of the establishment’s assets

| [20] | Don Herrmann, Shahrokh M. Saudagaran, Wayne B. Thomas “The quality of fair value measures for property, plant, and equipment” Accounting Forum, Volume 30, Issue 1, March 2006, Pages 43-59. |

[20]

.

1) External Sources of Information.

2) A significant decline in the market value of the asset occurred during the period more than expected because of the passage of time or normal use.

3) The occurrence of tangible changes that have a negative impact on the facility during the period or will occur soon in the technological technology, the market, and the economic and legislative climate in which the entity operates.

4) An increase in market interest rates on investments or in other market rates of return during the period.

5) If the book value of the entity’s net assets exceeds its capital value (Market Capitalization) according to market prices.

Internal Sources of Information

| [21] | Shengyi Yang, Shaoying Zhu, "Motivation of discre-tionary goodwill impairments", Research in Interna-tional Business and Finance. Volume 66, October 2023. |

[21]

.

1) Providing evidence of aging or physical damage to the original.

2) The occurrence of tangible changes that have a negative impact on the entity during the period or are expected to occur soon during which the asset is used or expected to be used, such as scrapping the asset and plans to stop or restructure operations related to the asset or plans to dispose of or sell the asset before the expected date.

3) The availability of evidence from internal reports indicating that the economic performance of the asset will be bad or is expected to be bad.

6.2. Accounting Issues Aimed at Measuring Impairment in the Value of Fixed Assets

The principle of accounting based on historical cost is considered the best basis for evaluating the facility’s assets. The cost includes all costs and expenses incurred by the entity and for the purpose for which it was owned. There is general agreement among users and preparers of financial statements on the importance and necessity of using historical cost as a basis for measuring the elements of these financial statements

| [22] | Andrea Bellucci a, Serena Fatica b, "Liability taxes, risk, and the cost of banking crises", Journal of Corpo-rate Finance. Volume 79, April 2023. |

[22]

.

This means that these lists must be prepared according to the historical cost of obtaining these items. Historical cost is characterized by the ease of verifying its accuracy and objectivity, because the prices are specified and fully known when the deal or commercial transaction occurs, and they are not subject to debate or change. It is also realistic due to the availability of documents and documents supporting it, and hence the financial statements prepared according to the historical cost are accurate and have a real and objective basis that is valid and verifiable and is not subject to personal judgment.

Companies are exposed to risk due to rapid and successive changes in the economic environment because of the exposure of their long-term assets to a decline in value, and one of the most important of these variables

is

| [23] | LaSalle, Randall. “Impairment of long-lived assets” Management Accounting. Montvale: Mar 1996. Vol. 77, Iss. 9; pg. 14, 1 pg. |

[23]

:

1) The rapid technological development.

2) Increasing the scope of global competition.

3) Change in demand for industrial machinery and equipment because of change in consumer desires.

4) Lack of rationality in administrative decisions

International accounting publications have become increasingly vocal about the necessity of reevaluating the asset at the end of the financial period to determine the value of the impairment in it, if any, to direct it in an accounting manner so that the financial statements reveal the true value of the asset and the impairment in value that has occurred to it. Also, the large fluctuations in the purchasing power of the monetary unit during inflation led to a decrease in the benefit of the principle of replacement cost (or current value) to reach results that are more realistic and representative of the value of assets, and to provide better results for investment and development decision makers

| [9] | John Sorros a, Nicholas Belesis b, Alkiviadis Karagiorgos, "The Reliability of Impairment Tests: The Case of Vessels", Procedia Economics and Finance. Volume 32, 2015, Pages 1787-1793. |

[9]

.

Accounting concepts contained in international publication:

International publications of American, British, international, and Egyptian accounting standards have agreed upon definitions of the most important concepts used when defining the concepts of value decline or impairment to provide comparability characteristics for published financial statements

| [24] | Prakash Pinto. “Accounting for Asset Impairment - Relevant Issues” Management Accountant. Calcutta: May 2005. Vol. 40, Iss. 5; pg. 395. |

[24]

.

1) Recoverable Amount

It is the net sales value of the asset or its value in use, whichever is greater.

2) Net Selling Value

It is represented by the fair value of the fixed asset, less the costs of selling. The fair value is determined by the amount that can be obtained from the sale of an asset or cash-generating units in a transaction between parties who have the desire to exchange, are aware of the facts, and deal with free will.

3) Assets Group

It represents the smallest level of cash flow generation that is largely independent of other groups of assets and other liabilities, meaning that the cash flows generated from this group can be identifiably distinguished from other groups.

4) Active Market

It is a market in which all the following conditions are met:

a. Homogeneity of items that are dealt with in the market.

b. The ease of having free-willed buyers and sellers at any time.

c. Prices must be available to the public.

5) Carrying Amount

It is the amount that is recognized for the asset after deducting any accumulated depreciation, amortization, or impairment losses in its value.

6) A Cash Generating Unit:

It is the smallest group of assets that generate cash inflows independently of cash inflows from other assets or groups of other assets.

7) Primary Assets

Tangible assets with specific useful lives other than intangible assets that contribute to the future cash flows of both the cash-generating unit under test and other cash-generating units.

6.3. Cost of Disposal

These are costs that are directly related to the disposal of an asset or cash-generating unit, excluding financing costs and income tax expenses.

1) Depreciable Amount

It is the cost of the asset or any other value that replaces the cost in the financial statements, minus the salvage value.

2) Depreciation

It is a systematic loading of the depreciable value of an asset over its productive life (or consumption of an asset over the estimated period of use from it). This is for a fixed asset. As for an intangible asset, it is called (Amortization).

3) Fair Value

The amount that can be obtained from the sale of an asset or cash-generating units in a transaction between parties who have the desire to exchange, are aware of the facts and deal freely.

4) Impairment Loss

It is the amount by which the book value of the asset or cash-generating unit exceeds its recoverable value. The recoverable value of the asset or cash-generating unit is determined by the fair value less costs of sale or its value in use, whichever is greater

| [25] | Jari Huikku a, Jan Mouritsen b, Hanna Silvola, "Rela-tive reliability and the recognizable firm: Calculating goodwill impairment value", Accounting, Organizations and Society. Volume 56, January 2017, Pages 68-83. |

[25]

.

5) Useful Life

It is: (a) The period during which the asset is expected to be used by the entity. Or (b) the number of production units or similar units that the entity is expected to obtain from the asset.

6) Value in Use

It is the present value of the future cash flows expected to occur from any asset or cash-generating unit.

6.4. Accounting Treatment According to the American Accounting Standard S.FAS. No: 144

Entities must recognize a decline in the value of an asset when:

1) The present value of the future flows expected to be obtained from the asset is less than the book value.

2) There will be a decrease in the economic level of the asset, which indicates a decrease in the efficiency of its operation

| [26] | Thomas A Gavin. “Implementation of SFAS No. 144: Accounting for the impairment or disposal of long-lived assets”. Commercial Lending Review. River woods: Jan 2003. Vol. 18, Issu. 1; p. 23 (11 pages). |

[26]

.

3) The value of the book assets is substantially greater than the fair value The standard considers fair value to be the value that can be obtained from a sale or exchange process to parties who can complete the deal, which requires the following:

a. Equal financial capacity of the parties to complete the deal.

b. Availability of a sufficient amount of information about the asset.

c. There is no relationship between the parties (related persons).

d. The desire of the contracting parties to complete the deal, and there is no intention to force or liquidate.

Methods that can be relied upon to determine fair value

| [27] | Steve Burkholder, Susan Webster. “FASB Issues Draft Guidance on Fair Value, Financial Asset Impairment”. Accounting Policy & Practice Report. Washington: Mar 20, 2009. Vol. 5, Iss. 6; pg. 255, 3 pgs. |

[27]

:

a. The price of the asset in the active market

b. Market prices of similar assets

c. Current value

The standard divided assets into three groups:

1) Long-term assets acquired for use.

2) Long-term assets acquired and will be disposed of, not by sale.

3) Long-term assets acquired and will be disposed of by sale.

The researcher will focus on long-term assets acquired for use, especially fixed assets used in operation to generate monetary units as a store of future benefits, and the standard requires that their value be tested permanently annually to calculate decline losses in their value. The process of decline in value requires the presence of evidence and factors indicating the existence of losses resulting from impairment, examples of which include the following

| [28] | Jack O Hall, C Richard Aldridge." Reporting the Dis-posal of Business Components and Segments - Changes Wrought by SFAS No. 144". Today's CPA. Dallas: Jul/Aug 2006. Vol. 34, Issu. 1; p. 34. |

[28]

:

1) The extent to which the asset can cover its book cost in the future.

2) The significant decrease in the market price

3) Continuous changes in the work climate and environment, including changes in legal, economic, and social factors.

Therefore, the standard presents the cases in which impairment losses must be recognized, and the entity must examine and test the asset to indicate its ability to recover its book value through a comparison between the book value and the undiscounted cash flows expected to be obtained from use in operation and service.

If the book value increases, the difference must be recognized immediately as a loss represented by the impairment of the value of the long-term asset (fixed asset). Therefore, the book value is adjusted with the new values to recalculate the depreciation according to the useful life of the new asset. If the opposite happens, an increase in the estimated value over the book value (i.e., an increase in its value in the market), the standard does not recognize it. Rather, it does not recognize the process of adjusting the previous value by recognizing the decline, and then the depreciable value becomes the new value according to the revaluation indicators.

The American standard also requires that assets be presented in independent, similar groups for the possibility of measuring cash flow generating units for each independent group of long-term assets. The justification for this may be to hide the decline of one asset at the expense of another asset, which fails the analytical ability to track the measurement of the asset’s efficiency ability and the extent of its contribution to achieving profits.

The standard explained that when estimating cash flows, several approaches can be relied upon, including:

1) The estimated approach: According to it, it is preferable to rely on logical and objective matters for estimation.

2) The period estimation approach, according to which the useful life remaining from the asset’s possession is estimated, considering the distinction between the methods of acquiring the asset, the type of investment, and the remaining life compared to the rest of the asset group.

3) Introduction to the type of asset and the expenses associated with it. The standard indicated that two types of assets are linked to expenses that represent capital expenditures that are closely related to the asset. Therefore, there are two types of these assets:

a. Assets developed considering their production capacity and the expenses required to maintain the level of services provided by the asset.

b. Assets under development. When determining their value, interest payments that are capitalized as part of the cost of the asset are considered.

6.5. Accounting Treatment According to the British Accounting Standard (ASB): FRS. No: 15

British Accounting Standard No. (15), entitled Measuring the Value of Fixed Assets, requires that the book value of the fixed asset represent its current value, which is measured according to indicators including its market value or its value in use at the date of preparing the budget, with the aim of

| [29] | Ron Paterson.” Financial Reporting: Ron Paterson - Capitalizing interest” Accountancy. London: Mar 2002. Vol. 129, Issu. 1303; pg. 100. |

[29]

:

1) Unifying the accounting treatments applied for measurement purposes.

2) Recognizing the economic benefits expected to be obtained during the economic life.

3) Revaluation in a way that reflects the current asset value.

4) Full publicity and effective disclosure of financial statements.

Standard (15) also defines the decline in the value of a fixed asset (impairment) as a decrease in the recoverable value of the fixed asset to a value less than its book value

| [30] | Conor Hickey a c e, John O'Brien c, Ben Caldecott b, "Can European electric utilities manage asset impair-ments arising from net zero carbon targets?", Journal of Corporate Finance. Volume 70, October 2021. |

[30]

.

6.6. Accounting Treatment According to International Accounting Standard IAS. No: 36

The recognition of impairment losses in the value of long-term assets received great attention from the International Accounting Standards Board (IASB), and it focused on that by developing a separate accounting standard for measurement, presentation, and disclosure, which is Standard 36, as the standard included indicators that reflect the decline in the value of assets, and the standard specified them in external and internal sources

| [31] | International Accounting Standards. IAS. "IAS 36: Im-pairment of Assets" London: 2004. p. 1405. |

[31]

.

If they exist, impairment in value must be recognized, including a decrease in the market value below the book value and the presence of evidence of obsolescence of the asset or the occurrence of physical damage to the asset, in addition to the necessity of re-evaluation at the end of each financial period to determine the value of the impairment, which is directed directly to the income statement as an impairment loss

| [32] | Samir Vanza, Peter Wells, Anna Wright, "Do asset im-pairments and the associated disclosures resolve uncer-tainty about future returns and reduce information asymmetry?", Journal of Contemporary Accounting & Economics. Volume 14, Issue 1, April 2018, Pages 22-40. |

[32]

.

The international standard requires calculating the impairment loss in the value of the asset annually and individually, and when it is proven that the recoverable value is less than the book value, the book value must be reduced to recognize the impairment loss so that the financial statements reveal the true value of the asset.

International Financial Reporting Standard IFRS No: 6

| [33] | Closer Look. K S Muthupandian. “IFRS 6: Exploration for and Evaluation of Mineral Resources” Management Accountant. Calcutta: Mar 2008. Vol. 43, Issu. 3; pg. 138. |

[33]

indicated indicators that if present, require a test of the value of the asset, including

| [34] | Max Williamson. “Impaired resources” Charter. Syd-ney: Jul 2007. Vol. 78, Issu. 6; pg. 68, 2 pgs. |

[34]

:

1) The expiration of the period for the concession right for the exploration and drilling area

2) If it is decided to stop exploration due to economic feasibility

3) If exploration expenses exceed the expected revenues (cost and return)

If these conditions are met, the facility must reconsider the value of the asset, which evidence and indicators indicate a decrease in its value

| [35] | Mike Brooks."IFRS 6 where next?" Accountancy. London: Jan 2008. Vol. 141, Issu. 1373; pg. 116. |

[35]

.

The value of impairment is measured under the standard by comparing the book value with the recoverable value. If the latter value is less than the book value, the impairment is calculated by the difference and directed directly to the income statement as a loss representing an impairment of the value of the fixed asset. The recoverable value is measured by whichever is greater, the value in use or the fair value less selling costs.

Determine the value in use:

It is determined through an estimate of the future cash inflows and outflows that can be obtained from using the asset or disposing of it at the end of its expected life, provided that an appropriate discount rate is used to calculate the cash flows by relying on the following elements:

1) Estimating the future flows expected to be obtained from the asset.

2) Expectations of possible deviations in the value or timing of those flows

3) The time value of money by using a risk-free interest rate.

4) The cost of uncertainty

5) Illiquidity reflected by participants in the active market.

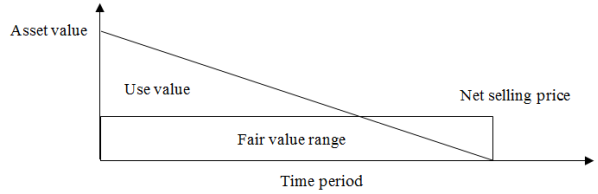

6) When calculating the value in use, the standard requires that it must consider its inclusion of all costs, and its estimation does not depend on the market but rather on the useful life of the asset, as shown in the following

figure 1, which was explained by some studies

| [36] | John McDonnell. “IAS 36 Impairment of Assets. Ac-countancy Ireland. Dublin: Dec 2005. Vol. 37, Issu. 6; p. 17 (3 pages). |

[36]

.

Relying on this form requires the managers’ commitment to conduct a value test for impairment. When estimating the value in use, the matter requires:

1) Estimating all cash inflows and outflows resulting from using the asset and disposing of it at the end of its useful life.

2) Use an appropriate discount rate for cash flows.

3) Considering the exclusion of the effect of taxes from the discount rate

Therefore, the international standard requires conducting a test of the value of the asset whenever indicators and evidence of its decline are available, which are recognized as impairment losses directed directly to the income statement. The fair value is relied upon whenever it is available. It does not require calculating the value in use in that case.

6.7. Accounting Treatment According to the Egyptian Accounting Standard AS. No: 3

The Egyptian accounting standard is like the international standard and is almost identical

| [37] | Minister of Investment Resolution No. 243 of 2006 regarding issuing Egyptian accounting standards. |

[37]

. Egypt became aware of the impairment standard in assets in 2006 with the issuance of Ministerial Resolution of the Minister of Investment No. 243 of 2006 regarding the issuance of Egyptian accounting standards, as this standard had not been applied before since the date of issuance of Egyptian accounting standards in 1997 under Ministerial Resolution of the Minister of Economy No. 503 of 1997. The standard aims to recognize assets at values that do not exceed their recoverable value and to apply impairment accounting to all assets other than Inventory (Standard 2), Assets Arising from Construction Contracts (Standard 8), Deferred Tax Assets (Standard 24), Financial Assets (Standard 26), Assets Arising from Employee Benefits (Standard 38), Real estate investment measured at fair value (Standard 34), biological assets related to agricultural activity measured at fair value less estimated costs at the point of sale (Standard 35), Deferred acquisition costs and intangible assets arising from contractual rights of insurance companies under insurance contracts (Standard 37), non-current assets classified as assets held for sale (Standard 32).

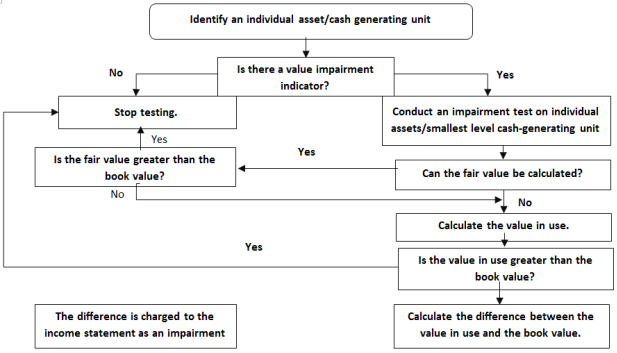

To measure the value of impairment, the standard requires that measurement be carried out according to the following indicators:

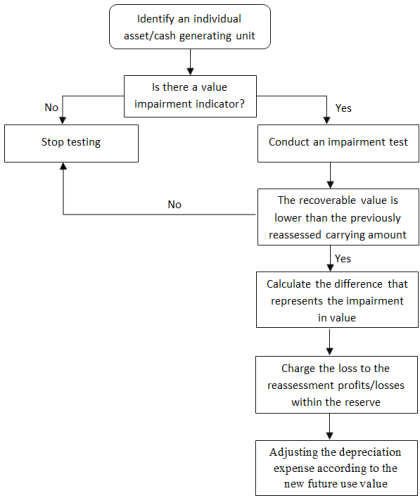

figures 2, 3. Regarding fixed assets that were revalued:

figure 4.

6.8. The Accounting and Tax Impact of Impairment in the Value of a Fixed Asset

The standard for impairment of the value of assets from accounting standards, whether international or Egyptian, stipulates that the assets are re-evaluated at the end of the financial year to determine the decline in their value for joint sister or affiliated projects, and for the assets that are recorded in the books based-on re-evaluation. In addition, the assets that are recorded at historical cost are tested for impairment in relation to their value at the end of the year. Accordingly, from an accounting standpoint, the company must, at the end of each financial period, evaluate the possibility of a decrease in the value of the assets and estimate the recoverable amount. This is done by comparing the book value with the recoverable amount at the end of each accounting cycle.

As previously indicated, the recoverable value of the asset may be the value in use or the net fair value, whichever is greater. From an accounting standpoint, when determining the value in use, the impairment standard allows the use of present value methods by estimating future cash flows discounted at an appropriate discount rate.

Elements of measuring present value according to the Egyptian Accounting Standard (Asset Impairment):

The standard provides a comparison between two approaches when calculating present value, and one of them can be used to estimate the value in use of an asset:

1) The traditional approach focuses on determining the discount price.

2) The expected cash flow approach focuses on the discount rate and uncertainty risks, which leads to adjusting when arriving at the expected cash flows after adjusting for the risks.

Whatever approach an entity takes to measure the value in use of an asset, the interest rates used to discount cash flows and the risks for which the estimated cash flows are adjusted must not reflect the effect of some assumptions. When the specified price for the asset is not directly available from the market, the entity uses alternatives to estimate the discount rate where the purpose is a market estimate that may be possible regarding the time value of money for periods until the end of the asset's useful life.

When it is available to everyone to find an option that is not available directly from the market and to change that to estimate the discount rate where the harvest is estimated to be the strength of the place about the value for the period of mice until the end of the productive era.

When making this choice, others may undoubtedly choose the following rates in their calculations when calculating the discount rate:

1) The average cost of the facility’s capital valve “Capital Asset Pricing Model”.

2) The cost of financing from third parties.

3) Prices of new trends in the market.

| [38] | International Financial Reporting Standards (IFRSs) “IFRS 6: Exploration for and Evaluation of Mineral Re-sources”. London: 2004. p. 573 |

[38]

Provided that the discount rate is before taxes, and therefore when the basis used is to estimate the discount rate, taxes are adjusted to show the price before taxes

| [39] | Scott M Susko, Khara Ashlynn Tusa. “OHIO: Court Rejects MCI Subsidiaries' Claims of Asset Impairment for Property Tax Valuations”, Journal of Multistate Taxation and Incentives. Boston: May 2009. Vol. 19, Issu. 2; pg. 43, 2 pgs. |

[39]

.

The accounting effect resulting from the impairment of fixed assets is considered a factor affecting the measurement of profit, The accounting rate decreased, which affects the tax base by decreasing, which has been determined by many studies and rulings. The ruling issued by the Ohio Court regarding the extent of the right of American companies, especially the parent company Courts, to deduct the impairment loss of the value of assets from the tax base. The objectivity of the deduction depends on the extent of accuracy in revaluing the asset. When a decrease in the value of the asset occurs, the loss is directed directly to the income statement according to accounting standards, even if it is the tangible asset, or any cash-generating unit, if it is recognized according to the publications of professional organizations because the assets represent because this affects the dividends of profits

| [4] | Oxner, Thomas, Oxner, Karen. “SFAS No. 121 asset im-pairments in oil companies” Oil & Gas Tax Quarterly. New York: Dec 1996. Vol. 45, Issu. 2; pg. 335. |

[4]

.

It is worth noting that in some opinions, a stock of future economic benefits that are reflected in future cash flows, so how can we not agree to deduct the impairment loss in the value of the asset from the tax base, as it is considered the most significant contributor to the cash flows obtained by the establishment and contributed to the disclosure of the net profit of the activity in previous financial periods

| [41] | Jack T Ciesielski, Thomas R Weirich. “Current SEC/PCOB Accounting and Auditing Issues” The Jour-nal of Corporate Accounting & Finance. Hoboken: May/Jun 2009. Vol. 20, Iss. 4; pg. 41. |

[41]

.

Publications of accounting and auditing standards and reports of the American Stock Exchange indicate the importance of deducting the impairment loss for long-term assets from the tax base or recognizing deferred tax to offset the impairment loss. Some studies, based on those publications and reports, indicate how establishments pay income tax on the impairment value. Assets that have already been included in the balance sheet according to their recoverable value

| [42] | Andreas Oestreicher, Christoph Spengel. “Tax Harmoni-zation in Europe: The Determination of Corporate Tax-able Income in the Member States” European Taxation. Amsterdam: Oct 2007. Vol. 47, Issu. 10; pg. 437. |

[42]

.

Furthermore, there are tax harmonization procedures in European Union countries that strive to adopt the deduction of the impairment loss from the tax base, particularly for group companies, because it is not possible to pay income tax on the value of a loss resulting from asset impairment, so unifying these transactions affects tax rates in European Union countries

| [42] | Andreas Oestreicher, Christoph Spengel. “Tax Harmoni-zation in Europe: The Determination of Corporate Tax-able Income in the Member States” European Taxation. Amsterdam: Oct 2007. Vol. 47, Issu. 10; pg. 437. |

[42]

.

The tax impact of an impairment loss on long-term assets is regarded to be the outcome of an impairment of the tax base, which impacts the payment of a greater income tax than is necessary, hence increasing the tax burden.

To solve this, it must be referred to as deferred income tax if it is not subtracted from the tax base. Furthermore, when determining the worth in use, which is dependent on cash flows, the tax impact must be included when assessing those flows.

The tax impact is very clear in the Ministerial Decision of the Minister of Finance issued No. 779 of 2007 amending some provisions of the executive regulations of the Income Tax Law. Article Seven of the decision stated the following: No. (7) Without prejudice to the provisions of the previous clauses, the following shall be observed: No. [A] Impairment losses and what is included as income when these losses are recovered are not included in the taxable base. No. [B] Taxable revenues or deductible costs that are not included in the income statement are included in the taxable base.

It is abundantly obvious from this text that an impairment loss recorded in the income statement or in equity in the statement of financial position is not regarded as an expense that is deductible. Instead, businesses and establishments must include that loss when making their tax return and subsequently subject it to income tax, despite the fact that It was recorded in the income statement as an income loss due to impairment, and the net accounting profit was decreased as a result. However, because it is not a deductible expenditure, it is returned to the net accounting profit in accordance with that ruling, which raises the establishments' tax burden, especially given that deferred tax is not shown on the tax return and that the state's sovereign resources may be cared for and preserved because of this tax treatment.

7. Proposed Model to Test the Feasibility of Applying the Proposed Model for Measuring the Impairment of a Fixed Asset

The model employed in this study is a development of a mathematical model that was indicated in one of the foreign studies cited in the introduction to the study, and which the researcher relied on to quantify the amount of decay value.

7.1. Elements of the Proposed Model

The symbols used in the proposed model can be defined as follows:

Net Present Value: NPV, expressed by the symbol V.

The probability of the project’s success: p, which is represented by a percentage on a scale starting from: 1% to 100%

Probability of project failure: P-1

Cash flows: X

High project manager efficiency: PH, which is represented by a decimal number on a scale starting from: 0.5 to 0.99.

Low project manager efficiency: PL, which is represented by a decimal number on a scale starting from: 0.01 to 0.5.

The amount of change in the project manager’s efficiency: O > P = PL – PH

Cash flows in case of project success: ds

Cash flows in case of project failure: df

Asset value: A

Relative index of asset efficiency: Y

The approximate calculated value of the asset value: \A

7.2. Assumptions of Model

1- The goals of legalization depend on effective management

A- The decision is unnecessary: o> 1 – PHX

B- The disreputable manager: o< 1 – PLX

2- The loan lender provides the joint loan with a manager with a high tendency to carry out this action:

PH ds + (1 – PH) V (A) -1 ≥ o

3- To maximize the profitability of the project, this condition must be fulfilled:

The loss resulting from the impairment of the asset value is determined in the following cases:

1) The profitability of the project tends to decrease because of the decrease in the net present value of the asset, according to the following:

2) NPV = PH (X – 1)

3)

4) The asset is subject to a mortgage and the intention is to liquidate it.

5) Increase the value of:

This indicates a change in the efficiency of the project manager. The greater the degree of change in the efficiency of the project manager, the more the value of that indicator tends to decrease, which indicates a decrease in the value of the asset.

When determining an appropriate discount rate to calculate discounted cash flows, these equations can be used, which contribute to calculating the capital asset pricing rate.

Calculate the cost of capital: Cost of capital = risk-free rate of return + (β × market risk premium).

Where β: risk premium

Calculating the cost of debt:

Cost of debt = (Risk-free rate of return + credit risk allowance) x (1 - income tax rate).

Calculate the facility's weighted average cost of capital =

WACC: formula and calculation.

where:

E = Market value of the firm’s equity

D = Market value of the firm’s debt

V = E + D

Re = Cost of equity

Rd = Cost of Debt

Tc = Corporate tax rate

As a result, the weighted cost of capital can be employed as a discount rate to determine the present value of a fixed asset or to discount cash flows.

Second:

Field study to test the validity of the possibility of applying the proposed model.

Five private businesses that work in the chemical industry's industrial sector were subjected to the proposed model. These businesses were part of a sample that was chosen at random from among those that operate in Egypt. Their shares are listed on the stock exchange, and among their fixed assets are machines and equipment whose value declined (decreased) by more than book value.

The results obtained by the researcher are extremely close to the realistic estimate of asset prices in the market for the same assets that are similar in efficiency, and the experimental investigation demonstrated the validity of the model's assumptions and its applicability. When attempting to estimate the absolute worth of managers' technical efficacy and the stock market's beta variation, the researcher ran into issues. Due to the absence of market stability and the fact that the Egyptian stock market is a dormant market, the researcher examined how beta moved in relation to the market based on the shares of the companies selected for the sample to which it was applied.

7. 3. Objective of the Field Study

With regard to the significance of measurement and accounting disclosure in the financial statements about the financial differences between the fair value of the asset and the value of the asset according to the proposed model, which requires a change to the Egyptian accounting standard, the field study aims to test the research hypotheses and determine the extent to which the hypothesis is accepted or not (31) Accounting for the impairment of the value of assets, to determine the extent to which it fulfills the requirements for measuring the value of the impairment of fixed assets in accounting and its tax effects.

i. Study population:

Three groups make up the study population:

1) Auditors for industrial capital businesses make up the first group. In the areas of accounting, auditing, and taxes, where the foreign partnership element and its correspondents participate, they were chosen from among the top offices in Egypt that correspond to foreign offices.

2) The second group consists of tax office auditors. They were selected among the staff members at the tax offices for joint-stock and investment businesses in Cairo and Alexandria as well as the Major Financiers' Mission.

3) The third category consists of academics with specialized tax interests who have contributed to several conferences on tax and accounting organized by Egyptian or Arab institutions and professional organizations.

ii. Study sample:

To determine the optimal sample, the researcher conducted an exploratory study, the main goal of which was to determine the clarity of the questionnaire questions within the limits of 25 questionnaires from auditors and auditors in the tax offices and academics. One of the most important conclusions that the researcher reached through those questionnaires is the homogeneity of the results of the study among each of the three groups. Therefore, random sampling tables were used, and the sample was determined with a degree of error (± 10%) due to the homogeneity of the results of the exploratory study. The optimal sample was 87 for auditors, 85 for auditors in tax offices, and 45 for academics (in light of the approximate numbers of the study population, which amount to about 2000 auditors, 1500 auditors, 1000 academics), 90 forms were distributed to auditors and the same to auditors at the tax offices, 50 forms to academics, and therefore the best sampling that would satisfy the study was natural random sampling.

In selecting the study sample, some demographic characteristics were considered, such as the length of experience (less than 5 years - 5 years - 10 years or more), and the educational level (Bachelor's - Diploma - Master's - Doctorate).

The questionnaires were sorted and incomplete ones as well as those that were not answered were excluded. The following table shows the actual study sample distributed according to the three study categories (auditors, academics, and tax offices). The following table:

Table 1. Frequency and percentage distribution of the actual study sample distributed according to the three study categories.

R | Characteristics of the study sample | auditors N = 80 | Auditors at the Tax Office N = 80 | Academics N = 40 |

number | % | number | % | number | % |

1- | Duration of experience: | | | | | | |

A. Less than 5 years | 10 | 12,5 | 14 | 17,5 | ـ | ـ |

B. 5 years | 40 | 50,0 | 52 | 65,5 | ـ | ـ |

C. 10 years | 30 | 37,5 | 14 | 17,5 | 40 | 100 |

2- | Educational level: | | | | | | |

A- Bachelor’s degree | 30 | 37,5 | 28 | 35,0 | ـ | ـ |

B- Diploma | 24 | 30,0 | 20 | 25,0 | ـ | ـ |

C - Master's degree | 22 | 27,5 | 26 | 32,5 | ـ | ـ |

D- Ph.D. | 4 | 5,0 | 6 | 7,5 | 20 | 100 |

Design the questionnaire list:

Each of the two portions of the survey list was created with the intention of evaluating a different research hypothesis. The following questions are addressed in each section and encompass various facets of the hypothesis whose validity is to be tested:

First Section: This questionnaire, which consists of questions 1 through 4, aims to test the research's first hypothesis regarding "the extent of the necessity of accounting disclosure in the financial statements of the accounting differences between the fair value of the asset and the value of the asset according to the proposed model in a way that affects the credibility of the evaluation method for the asset." at the conclusion of the fiscal period for both tax and accounting income.

Second section: includes questions from: (5 to 8) with the aim of testing the second hypothesis of the research related to “the extent of the importance of making an amendment to the Egyptian Accounting Standard No. (31) Accounting for the Impairment of Assets with regard to measuring the impairment of fixed assets by including a mathematical model for measurement that is an alternative.”

Statistical methods used:

The statistical analysis of the field study data, as non-standard descriptive data, was based on the following:

Statistical description of the data, including frequency and proportional distribution as well as some descriptive metrics like the weighted arithmetic mean and coefficient of variation.

Chi-2 analysis. The main presumptions underpinning this test are that observations are independent of one another, simple random sampling, and the degree of measurement. While the expected frequencies in each cell must be minimal, there are no constraints on the size of the observed frequencies. According to the predominant opinion, observed frequencies shouldn't be less than (6) in any cell.

The Kruskal-Wallis’s test, which evaluates the degree of statistically significant differences between three or more groups with ordinal data or that can be arranged, is carried out by solving the following equation. This test is essentially a one-way analysis of variance for ordinal data:

where:

n → number of all ranks (number of scores for all samples)

K → the sum of the square of the sum of the ranks of each sample divided by the column of sample members for that group.

This is with the following note:

A- Kruskal-Wallis test can be applied to first-order analysis of variance without requiring that the samples have an equal number of participants.

B- The chi-square the following tables is used to preview the calculated value with the theoretical value if the number of samples or tests exceeds (3), and the number of items for each sample must be no less than (6).

Results and testing of research hypotheses:

The outcomes of the first section:

This section contains questions (1-4) that are related to testing the research's first hypothesis, which is that "There is no need for accounting disclosure in the financial statements about the financial differences between the fair value of the asset and the value of the asset according to the proposed model in a way that affects the credibility of the evaluation method for the asset at the end of the financial period for accounting income and tax income."

The results of this section are as follows:

The first question addresses: the extent of the necessity of considering the financial effects resulting from the differences between accounting income and tax income when determining the value of the impairment of a fixed asset.

The results, as shown in

Tables 2 and 3, showed that there were no statistically significant differences between the three categories of the study, as the value of the Kruskal-Walli's test (calculated Ca2 = 3.38), which confirms its lack of significance given at least 0.05 degrees. Because it did not exceed the minimum that makes it a function at level of freedom 2. We also find that the value of the arithmetic means for the responses of the three study categories ranged between (3.90 - 4.22), which reflects that there is a very large degree of agreement among the three study categories.

Table 2. The extent of the differences between the three study categories About the financial implications of the differences Between accounting and tax income when determining the impairment value of a fixed asset Using the Kruskal-Walli's test.

Study categories Rank average | Account auditors | Auditors | Academics |

Rank average | 55.60 | 50.55 | 45.38 |

Ka2 = 3.38 significance level = 0.894 D. h = 2 it is a non-function |

Table 3. Frequency and relative distribution and some descriptive measures Responses of the three study categories on impacts Consequences of the differences between accounting and tax income Resulting from the impairment of the value of the fixed asset.

Degree of approval Study categories | Strongly agree (1) | Agree (2) | I don’t know (3) | Disagree (4) | Strongly disagree (5) | Some descriptive metrics |

Auditors % | 28 | 42 | 10 | -- | -- | 42 ** |

35.0 | 52.5 | 12.5 | -- | -- | 15.60% * |

Academics % | 12 | 20 | 2 | 2 | -- | 4.05 ** |

30.0 | 50.0 | 15.0 | 5.0 | -- | 20.50% * |

Auditors at the Tax Office % | 16 | 46 | 12 | 12 | -- | 3.90 ** |

20.0 | 57.5 | 15.0 | 7.5 | -- | 20.80% * |

The second question deals with: The model for measuring the value of the impairment of a fixed asset. The results showed, as shown in

Table 4, that there are no statistically significant differences between the frequency and relative distribution of responses for categories 2 The third study on methods of measuring the impairment of a fixed asset, where the value of the Chi test reached The calculated value = 2.532) and therefore it did not reach the minimum level that would make it significant at the level of 0.05 at least. I also explained, according to the results, that the most important method used is the proposed model method (for the companies to which the model was applied) to measure the impairment of the fixed asset presented by the researcher, the importance of which he stressed. About (60% - 73%) of the three study categories. The following table:

Table 4. The extent of the difference between the three study categories regarding methods of measuring the value of a fixed asset.

Study Categories The most important methods used | Auditors | Academics | Auditors at the Tax Office |

No. | % | No. | % | No. | % |

Fair value | 12 | 15.0 | 6 | 15.0 | 18 | 22.5 |

The net realizable value method | 10 | 12.5 | 10 | 25.0 | 12 | 15.0 |

The model for measuring the impairment of the value of a fixed asset was presented by the researcher. | 58 | 72.5 | 24 | 60.0 | 50 | 62.5 |

Chi 2 = 2.533 | Significance level = 0.639 |

D H = 4 | it is a non-function |

The third question addresses the most important advantages resulting from using the measurement model provided by the researcher to measure the value of the impairment of a fixed asset, ranking it according to its importance. The results showed, as shown in

Table 5, the agreement of all three categories of the study on all the advantages and the degree of importance of each of them, which are:

Its agreement with generally accepted accounting principles and policies when preparing financial statements.

Its agreement with the concept of net present value.

Its importance in predicting future cash flows and the efficiency of managers in the facility.

Its reliance on discount rates is expected to prevail in the future. As the following table:

Table 5. Ranking of the advantages resulting from using the proposed model According to their degree of importance, they are distributed according to study categories.

| Auditors | Academics | Tax Officers |

Important advantages | M | Coefficient of variation % | Rank | M | coefficient of variation % | Rank | M | coefficient of variation % | Rank |

Its agreement with the concept of net present value | 2.08 | 42.8 | 2 | 2.00 | 48.5 | 2 | 2.00 | 41.5 | 2 |

Its agreement with generally accepted accounting principles and policies when preparing financial statements. | 1.55 | 44.5 | 1 | 1.40 | 35.7 | 1 | 1.44 | 38.2 | 1 |

Its reliance on discount rates expected to apply in the future. | 3.26 | 25.2 | 4 | 3.25 | 22.2 | 4 | 3.44 | 20.9 | 4 |

Its importance in forecasting future cash flows and the efficiency of managers. | 2.78 | 42.1 | 3 | 3.05 | 32.8 | 3 | 3.00 | 35.0 | 3 |

The fourth question deals with the justifications for non-recognition in Egypt when measuring the tax base by accounting for the impairment of the value of a fixed asset arising from the differences between accounting income and tax income. The results showed, as shown in

Table 6, that there is agreement between the degree of importance of the reasons referred to in the survey form among the three categories of the study, as there is agreement.

In order:

A- The state’s desire not to waste tax revenues.

B- Not applying Egyptian Accounting Standard No. (31) Impairment of the Value of Assets when measuring Tax Profit.

C- There is not fine for non-compliance with the application of accounting standards in Egyptian tax legislation.

On the other hand, there was a relative difference in the degree of importance of the remaining reasons. The following table:

Table 6. The relative importance of the reasons for non-recognition in Egypt Accounting for the tax decline in the value of a fixed asset Distributed according to study categories.

| Auditors | Academics | Tax Officers |

Reasons | M | Coefficient of variation % | Rank | M | coefficient of variation % | Rank | M | coefficient of variation % | Rank |

There is no paragraph for a mathematical model in the Egyptian Accounting Standard (31) to account for the impairment of the asset’s value according to the proposed model. | 34 | 42.5 | 2 | 24 | 60.0 | 1 | 34 | 35.0 | 2 |

The state’s desire to avoid wasting tax revenues. | 36 | 45.0 | 1 | 22 | 55.0 | 2 | 36 | 37.0 | 1 |

The presence of a fine for violating compliance with the application of accounting standards in legislation | 32 | 40.0 | 3 | 20 | 50.0 | 3 | 20 | 25.0 | 3 |

Egyptian tax. | | | | | | | | | |

D - The difficulty of applying accounting measurement according to fair value. | 16 | 20.0 | 4 | 8 | 20.0 | 5 | 20 | 25.0 | 4 |

E- The relative insignificance of the financial differences resulting from measuring impairment. | 16 | 20.0 | 5 | 8 | 20.0 | 4 | 12 | 15.0 | 5 |

The statistical analysis of the results of the first section’s questions showed that there is a need for accounting disclosure in the financial statements about the impairment of the value of the fixed asset resulting from the differences between accounting income and tax income, which indicates that the first assumption is incorrect.

The results of the statistical analysis of this section also showed the preference of the model that the researcher developed in measuring the value of the impairment of the fixed asset because of its many advantages, the most important of which is its agreement with the accounting principles and policies generally accepted when preparing the financial statements, and with the concept of net present value.

The results of the questions in this section also revealed that there are many reasons that led to non-recognition in Egypt of the tax impairment (loss) of the fixed asset, the most important of which is the state’s desire not to waste the tax proceeds, in addition to the lack of a standard for measuring the impairment of value according to a mathematical model such as the proposed model. Paragraph: While the study sample collectively agreed that the absence of a fine for non-compliance with the application of accounting standards in Egyptian tax legislation is one of the important reasons for non-compliance with their application at a time when the tax administration does not activate some articles of the standards for purposes related to not wasting tax proceeds.

Results of the second section:

This section includes questions from: (5 to 8) related to testing the second hypothesis of the research, which deals with:

“There is a necessity and utmost importance to make an amendment to the Egyptian Accounting Standard No. (31) Accounting for Impairment of Assets with regard to measuring the impairment of fixed assets by including a mathematical model for measurement that is an alternative for fair value.” The results of this section are as follows:

The fifth and sixth questions address the extent of the necessity of issuing an amendment to the Egyptian Accounting Standard (31) to measure the impairment of the value of a fixed asset according to the proposed model, and the justifications for issuing this amendment.

The results showed, as shown in

Table 7, that there are statistically significant differences between the responses of the three study categories regarding issuing an amendment to the Egyptian Accounting Standard for accounting for the impairment of assets, especially fixed assets, as the value of the calculated Chi2 test reached = 19.881, which confirms its significance at the level of 0.01 with 2 degrees of freedom.

The results showed that both auditors and academics support the necessity of issuing an amendment to the Egyptian Accounting Standard (31) to use a model that is suitable for measuring the impairment of the value of the fixed asset according to the proposed model, while the tax auditors do not tend to this opinion, and this was confirmed by the frequency and relative distribution of the three study categories. The following table:

Table 7. The extent of the difference between the three study categories About issuing an amendment to the Egyptian Accounting Standard (31) To use a model to measure the decline of a fixed asset according to the proposed model and justifications for issuing this standard.

Statement | auditors | Academics | Tax Officers | chi-square |

No. | % | No. | % | No. | % |

1- The necessity of issuing an amendment to the Egyptian accounting standard to account for the impairment of the value of an asset Constant according to the proposed model | | | | | | | **19.881 |

Yes: | 70 | 87.5 | 34 | 85.0 | 36 | 45.0 |

no: | 20 | 12.5 | 6 | 15.0 | 44 | 55.0 |

2 -Justifications for issuing an amendment to the standard | No. | Rank | No. | Rank | No. | Rank |

Proper measurement of business results | 62 | | 30 | | 36 | |

% | 77.5 | 1 | 75.0 | 1 | 45 | 1 |

Comparability of financial statements | 60 | | 30 | | 38 | |

% | 75.5 | 2 | 75.0 | 1 | 47.5 | 1 |

C- The possibility of forecasting flows future cash | 16 | | 8 | | 16 | |

% | 20.0 | 3 | 20.0 | 2 | 20.0 | 3 |

D- The possibility of predicting the return on Investment. | 8 | | 2 | | 10 | |

% | 10.0 | 4 | 5.0 | 3 | 12.5 | 4 |

The seventh question deals with the comparison between the proposed model and fair value methods used in measuring the impairment of the value of a fixed asset and the justifications for using each of them.

The results showed, as shown in

Table 8, that there were statistically significant differences between the three categories of the study regarding the two methods, as the two test values (calculated Chi2 = 40.365, 43.41), which confirms their significance at the 0.01 level, with 2 degrees of freedom. The results also showed Auditors at tax offices tend to use the fair value method, which may depend on the recognition of the exchange value, which is approximately equivalent to the net value, as 77.5% of them confirmed this, while both auditors and academics unanimously agreed to prefer the proposed model method, which depends on the recognition of the financial effects. Resulting from the net present value of the asset.

Fixed assets, future cash flows, and the efficiency of managers in the company that owns the fixed asset, as confirmed by about 84% of the total auditors and 90% of the total academics. Perhaps one of the most important justifications for using the proposed model method for auditors and academics is its agreement with generally accepted accounting principles and policies, while one of the most important justifications for using the fair value method for auditors in tax authorities is its ease of application. The following table:

Table 8. The extent of the difference between the study categories regarding the methods used in measuring the impairment of the value of a fixed asset and the justifications for using each of them.

statement | auditors | Academics | Tax Officers | chi-square |

No. | % | No. | % | No. | % |

1 The most important methods A- The fair value method, which depends on the recognition of the exchange value, may be equivalent to the net. Selling value approx. | 13 | 16.0 | 4 | 10 | 62 | 77.5 | ** 40.365 |

B- The proposed model method that relies on recognition with the financial effects resulting from the net present value Future flows and the efficiency of managers in companies that own fixed assets. | 67 | 84.0 | 36 | 90.0 | 14 | 12.5 | ** 34.416 |

2 Justifications for using methods. Agreement with accounting principles and policies: Ease of application | 65 | 81.0 | 28 | 70.0 | 19 | 23.75 | |

15 | 19.0 | 12 | 30.0 | 61 | 76.25 | |

The eighth question deals with the necessity of disclosing the justifications for not using the proposed model in measuring the impairment of the asset value in the entity’s financial statements. The study showed, as shown in

Tables 9 and 10, that there are no statistically significant differences between the different categories of the study, as confirmed by the value of the Kruskal-Wallis test (calculated chi2 = 0.894), which confirms their lack of significance as it is It did not exceed the minimum that makes it significant at the level of 0.05 at least, with degrees of freedom = 2. This was confirmed by the value of the arithmetic mean of the responses of the three study categories, which ranged between (4.25 - 4.40) among the three study categories, which reflects a very high degree of agreement on the necessity of disclosing Not using the proposed model to measure the impairment of fixed assets. The following tables:

Table 9. The extent of the difference between the three categories of the study regarding the disclosure of justifications for not using the proposed model in measuring the impairment of the value of the asset.

Study categories | auditors | Academics | Tax Officers |

Average rank | 53.50 | 48.95 | 48.28 |

chi-square = 0.894 Significance level = 0.640 D.H =2 Non-functional |

Table 10. Frequency and percentage distribution and some descriptive measures regarding disclosing justifications for not using the proposed model for measurement, distributed according to study categories.

Degree of approval Study categories | Strongly agree (5) | I agree (4) | I don’t know (3) | I don’t agree (2) | I strongly disagree (1) | Some descriptive metrics |

Auditors | 36 | 40 | 4 | --- | -- | 4.40 |

% | 45.0 | 50.0 | 5.0 | --- | -- | %13.40 |

Academics | 14 | 24 | 2 | --- | --- | 4.30 |

% | 35.0 | 60.0 | 5.0 | --- | --- | %13.3 |

Tax Officers | 32 | 36 | 12 | --- | --- | 4.25 |

% | 40.0 | 45.0 | 15.0 | --- | --- | %16.7 |

Through the results of the questions of the second section, it can be said that there is a need to issue an amendment to the Egyptian accounting standard for accounting for the impairment of the value of a fixed asset according to the proposed model, which indicates the invalidity of the second hypothesis of the research. The results of the statistical analysis also showed that the most important justification for issuing this amendment is the proper measurement of business results and the comparability of financial statements. The results also showed that the proposed model method is the best method that can be used to properly measure the impairment of the value of a fixed asset due to its agreement with generally accepted accounting principles and policies. The results of this section also made it clear that there is a need to disclose the justifications for not using the proposed measurement model in the facility’s financial statements.