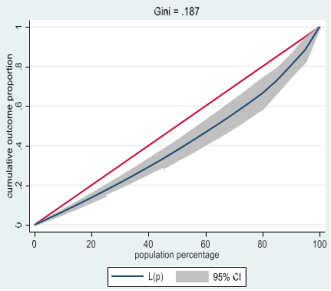

Protection against financial risk is an essential pillar of Universal Health Coverage (UHC), particularly through the reduction of out-of-pocket payments that can lead to catastrophic health expenditure (CHE). This study aims to identify the determinants of CHE among households in Côte d'Ivoire. We conducted a cross-sectional analytical study using data from the 2021 Harmonized Household Living Conditions Survey (HLCS) (secondary analysis). The survey is based on a two-stage probability sampling method; 1,084 clusters and 13,008 households were initially selected, and 12,965 households were retained after validation. CHE was defined according to the "ability to pay" approach: a dichotomous variable (CHE=1) when OOPCAP = OOP/CAP ≥ 40%, otherwise CHE=0. Descriptive statistics, a bivariate Chi² test and binary logistic regression were used (Stata 17). Households spend more than half of their consumption expenditure on food (52.2%). The frequency of CHE is low: 0.11% in the total sample (14 households) and 0.35% among those who received direct payments. The concentration curve indicates a relatively homogeneous distribution (Gini = 0.187). The logistic model is significant (Chi² = 38.38; p < 0.001; pseudo-R² = 0.094). The risk of CHE decreases significantly with household size (OR = 0.07 for 6–7 members; OR = 0.03 for >7). Conversely, households headed by a married person have an increased risk (OR = 5.27), as do those residing in rural areas (OR = 4.72). With regard to standard of living, the upper quintiles show odds ratios below 1 (Q2 to Q5), suggesting better financial protection, although some associations are of marginal significance. No significant link is observed for the gender of the head of household or for residence in Abidjan. CHE are rare, but their distribution remains socially differentiated: increased risk in rural areas, increased vulnerability when the head of household is married, and a protective effect of household size, linked to intra-family mutualization. A socioeconomic gradient also appears, with wealthier households being less exposed, but the significance is marginal. These results call for strengthening financial protection, especially in rural areas, and interpreting CHE with caution, given their rarity and sensitivity to methodological choices.

| Published in | International Journal of Health Economics and Policy (Volume 11, Issue 1) |

| DOI | 10.11648/j.hep.20261101.14 |

| Page(s) | 40-48 |

| Creative Commons |

This is an Open Access article, distributed under the terms of the Creative Commons Attribution 4.0 International License (http://creativecommons.org/licenses/by/4.0/), which permits unrestricted use, distribution and reproduction in any medium or format, provided the original work is properly cited. |

| Copyright |

Copyright © The Author(s), 2026. Published by Science Publishing Group |

Catastrophic Health Expenditure, Financial Protection, Universal Health Coverage, Côte d'Ivoire

Features | Rural (n=7722) (n,%) | Urban (n=4296) (n,%) | Abidjan (n=947) (n,%) | Total (n=12, 965) (n,%) | P | |

|---|---|---|---|---|---|---|

Sex | Male | 6608 (85.6) | 3358 (78.2) | 723 (76.3) | 10689 (82.5) | 0.027 |

Female | 1114 (14.4) | 938 (21.8) | 224 (23.7) | 2276 (17.6) | ||

Sex ratio | 5.93 | 3.58 | 3.23 | 4.70 | ||

Age (Year) | 15–24 | 235 (3) | 220 (5.1) | 33 (3.5) | 488 (3, 8) | 0.0001 |

25–34 | 1512 (19.6) | 889 (20.7) | 153 (16.2) | 2554 (19, 7) | ||

35-44 | 2235 (28.9) | 1228 (28.6) | 279 (29.5) | 3742 (28, 9) | ||

45-54 | 1670 (21.6) | 919 (21.4) | 249 (26.3) | 2838 (21, 9) | ||

55-64 | 1167 (15.1) | 620 (14.4) | 146 (15.4) | 1933 (14, 9) | ||

65 and over | 903 (11.7) | 420 (9.8) | 87 (9.2) | 1410 (10.9) | ||

Average age Standard deviation | 46 (14.1) | 44.8 (14) | 45.9 (12.7) | 45.6 (14) | ||

Median [Min - Max] | 44 [15-102] | 43 [15-100] | 45 [17-88] | 44 [15-102] | ||

Marital status | Bachelor | 851 (11) | 831 (19.3) | 225 (23.8) | 1907 (14.7) | 0.0001 |

Married) | 6034 (78.1) | 2990 (69.6) | 614 (64.8) | 9638 (74.3) | ||

Widowed/Divorced | 837 (10.8) | 475 (11.1) | 108 (11.4) | 1420 (11) | ||

Schooling level | None | 4967 (64.3) | 2199 (51.2) | 281 (29.7) | 7447 (57, 4) | 0.0001 |

Primary | 1582 (20.5) | 809 (18.8) | 153 (16.2) | 2544 (19, 6) | ||

Secondary 1 | 706 (9.1) | 574 (13.4) | 165 (17.4) | 1445 (11, 2) | ||

Secondary 2 | 324 (4.2) | 412 (9.6) | 128 (13.5) | 864 (6, 7) | ||

Superior | 142 (1.8) | 302 (7) | 220 (23.2) | 664 (5, 1) | ||

Household spending quintile | Q1 | 2025 (26.2) | 540 (12.6) | 28 (3) | 2593 (20) | 0.0001 |

Q2 | 1825 (23.6) | 718 (16.7) | 50 (5.3) | 2593 (20) | ||

Q3 | 1600 (20.7) | 878 (20.4) | 115 (12.1) | 2593 (20) | ||

Q4 | 1340 (17.4) | 1023 (23.8) | 230 (24.3) | 2593 (20) | ||

Q5 | 932 (12.1) | 1137 (26.5) | 524 (55.3) | 2593 (20) | ||

Employment situation (n=54924) | In employment | 7146 (92.5) | 3735 (86.9) | 763 (80.6) | 11644 (89, 8) | 0.0001 |

Unemployed | 576 (7.5) | 561 (13.1) | 184 (19.4) | 1321 (10, 2) | ||

CSP (n=11834) | Senior executive | 14 (0.2) | 33 (0.9) | 37 (4.8) | 84 (0.7) | 0.0001 |

Middle management | 119 (1.6) | 204 (5.4) | 76 (9.8) | 399 (3, 4) | ||

Worker or employee qualified | 158 (2.2) | 368 (9.7) | 170 (22) | 696 (5, 9) | ||

Worker or employee simple | 326 (4.5) | 461 (12.2) | 147 (19) | 934 (7, 9) | ||

Laborer | 208 (2.9) | 135 (3.6) | 5 (0.6) | 348 (2, 9) | ||

Boss | 87 (1, 2) | 114 (3) | 28 (3.6) | 229 (1, 9) | ||

Self-employed | 6219 (85.4) | 2336 (61.8) | 283 (36.6) | 8838 (74.7) |

Variables | Mean | Standard deviation | Median |

|---|---|---|---|

DACT | 0.5221288 | 0.1307095 | 0.5253643 |

Variables | Number | Standard error | Percentage (%) |

|---|---|---|---|

Presence of CHE | 14 | 0.0002884 | 0.11 |

Absence of CHE | 12951 | 0.0002884 | 99.89 |

Variables | Number | Standard error | Percentage (%) |

|---|---|---|---|

Presence of CHE | 14 | 0.0009291 | 0.35 |

Absence of CHE | 4006 | 0.0009291 | 99.65 |

DSC | Odds-ratios. | St.Err. | t-value | p-value | [95% Conf | Interval] | Sig |

|---|---|---|---|---|---|---|---|

Taille | 1 | . | . | . | . | . | |

2 à 3 | 0.237 | 0.189 | -1.81 | 0.071 | 0.05 | 1.129 | * |

4 à 5 | 0.119 | 0.102 | -2.49 | 0.013 | 0.022 | 0.637 | ** |

6 à 7 | 0.066 | 0.063 | -2.87 | 0.004 | 0.01 | 0.424 | *** |

>7 | 0.025 | 0.027 | -3.39 | 0.001 | 0.003 | 0.21 | *** |

Situation Matrimoniale | 1 | . | . | . | . | . | |

Marié (e) | 5.27 | 3.388 | 2.59 | 0.01 | 1.495 | 18.58 | *** |

Veuf (ve)/Divorcé | 4.066 | 3.497 | 1.63 | 0.103 | 0.753 | 21.938 | |

Q1 | 1 | . | . | . | . | . | |

Q2 | 0.303 | 0.211 | -1.72 | 0.086 | 0.077 | 1.185 | * |

Q3 | 0.351 | 0.227 | -1.62 | 0.105 | 0.099 | 1.245 | |

Q4 | 0.35 | 0.22 | -1.67 | 0.095 | 0.102 | 1.201 | * |

Q5 | 0.257 | 0.188 | -1.86 | 0.063 | 0.061 | 1.076 | * |

: base Urbain | 1 | . | . | . | . | . | |

Rural | 4.718 | 3.537 | 2.07 | 0.039 | 1.086 | 20.509 | ** |

Abidjan | 2.657 | 3.297 | 0.79 | 0.431 | 0.233 | 30.239 | |

Sexe | 1 | . | . | . | . | . | |

Feminin | 1.083 | 0.462 | 0.19 | 0.851 | 0.469 | 2.499 | |

Constant | 0.001 | 0.001 | -5.59 | 0 | 0 | 0.012 | *** |

Mean dependent var | 0.001 | SD dependent var | 0.023 | ||||

Pseudo r-squared | 0.094 | Number of obs | 44422 | ||||

Chi-square | 38.382 | Prob > chi2 | 0.000 | ||||

Akaike crit. (AIC) | 398.730 | Bayesian crit. (BIC) | 520.550 | ||||

*** p<0.01, ** p<0.05, * p<0.1 | |||||||

ANstat | National Statistics Agency |

CAP | Capacity to Pay |

CHE | Catastrophic Health Expenditure |

HCLS | Household Living Conditions Survey |

MHFE | Monthly Household Food Expenditure |

MTE | Monthly Total Expenditure |

OOP | Out-of-Pocket |

OOPCAP | Out-of-Pocket Payments as a Share of Capacity to Pay |

RGPH | General Population and Housing Census |

ZD | Enumeration Areas |

| [1] | Kutzin J. Health financing for universal coverage and health system performance: concepts and implications for policy. Bull World Health Organ. 2013; 91(8): 602-611. |

| [2] | Wagstaff A, Flores G, Hsu J, Smitz MF, Chepynoga K, Buisman LR, van Wilgenburg K, Eozenou P. Progress on catastrophic health spending in 133 countries: a retrospective observational study. Lancet Glob Health. 2018; 6(2): e169-e179. |

| [3] | World Health Assembly. Sustainable health financing, universal coverage and social health insurance. Resolution WHA58.33. Geneva: World Health Organisation; 2005. |

| [4] | Carrin G, James C, Evans DB. Designing health financing policy towards universal coverage. Bull World Health Organ. 2007; 85(9): 652. |

| [5] | Abiiro GA, De Allegri M. Universal health coverage from multiple perspectives: a synthesis of conceptual literature and global debates. BMC Int Health Hum Rights. 2015; 15: 17. |

| [6] | Kimani JK, Ettarh R, Kyobutungi C, Mberu B, Muindi K. Determinants for participation in a public health insurance programme among residents of urban slums in Nairobi, Kenya: results from a cross-sectional survey. BMC Health Serv Res. 2012; 12: 66. |

| [7] | Khan JAM, Ahmed S, Evans TG. Catastrophic healthcare expenditure and poverty related to out-of-pocket payments for healthcare in Bangladesh—an estimation of financial risk protection of universal health coverage. Health Policy Plan. 2017; 32(8): 1102-1110. |

| [8] | Hsu J, Flores G, Evans DB, Mills A, Hanson K. Measuring financial protection against catastrophic health expenditures: methodological challenges for global monitoring. Int J Equity Health. 2018; 17: 69. |

| [9] | Xu K, Evans DB, Kawabata K, Zeramdini R, Klavus J, Murray CJL. Household catastrophic health expenditure: a multicountry analysis. Lancet. 2003; 362(9378): 111-117. |

| [10] | Nguyen HA, Ahmed S, Turner HC. Overview of the main methods used for estimating catastrophic health expenditure. Front Public Health. 2023; 11: 1065737. |

| [11] | World Health Organisation, International Bank for Reconstruction and Development/The World Bank. Tracking universal health coverage: 2023 global monitoring report. Geneva: World Health Organisation; 2023. |

| [12] | Attia-Konan AR, Oga ASS, Koffi K, Kouame J, Touré A, Kadio K, et al. Distribution of out-of-pocket health expenditures in a sub-Saharan Africa country: evidence from the national survey of household standard of living, Côte d’Ivoire. Int J Equity Health. 2019; 18: 152. |

| [13] | Leive A, Xu K. Coping with out-of-pocket health payments: empirical evidence from African countries. Bull World Health Organ. 2008; 86(11): 849-856. |

| [14] | Kruk ME, Goldmann E, Galea S. Borrowing and selling to pay for health care in low- and middle-income countries. Health Affairs (Millwood). 2009; 28(4): 1056-1066. |

| [15] | Eze P, Lawani LO, Agu UJ, Acharya Y. Factors associated with catastrophic health expenditure in sub-Saharan Africa: a systematic review. BMC Health Serv Res. 2022; 22: 1327. HYPERLINK |

| [16] | Koomson I, Abdul-Mumuni A, Abbam A. Effect of financial inclusion on out-of-pocket health expenditure: empirics from Ghana. Eur J Health Econ. 2021; 22(9): 1411-1425. |

| [17] | Wilson DR, Haas S, Van Gelder S, Hitimana R. Digital financial services for health in support of universal health coverage: qualitative programmatic case studies from Kenya and Rwanda. BMC Health Serv Res. 2023; 23(1): 1036. |

APA Style

Kouame, K., Regine, A. A., Jerome, K., Dramane, S. A., Serge, O. S., et al. (2026). Factors Associated with Catastrophic Health Expenditure Among Households in Côte d'Ivoire. International Journal of Health Economics and Policy, 11(1), 40-48. https://doi.org/10.11648/j.hep.20261101.14

ACS Style

Kouame, K.; Regine, A. A.; Jerome, K.; Dramane, S. A.; Serge, O. S., et al. Factors Associated with Catastrophic Health Expenditure Among Households in Côte d'Ivoire. Int. J. Health Econ. Policy 2026, 11(1), 40-48. doi: 10.11648/j.hep.20261101.14

@article{10.11648/j.hep.20261101.14,

author = {Koffi Kouame and Attia-Konan Akissi Regine and Kouame Jerome and Sangare Abou Dramane and Oga Stephane Serge and Kouadio Luc},

title = {Factors Associated with Catastrophic Health Expenditure Among Households in Côte d'Ivoire},

journal = {International Journal of Health Economics and Policy},

volume = {11},

number = {1},

pages = {40-48},

doi = {10.11648/j.hep.20261101.14},

url = {https://doi.org/10.11648/j.hep.20261101.14},

eprint = {https://article.sciencepublishinggroup.com/pdf/10.11648.j.hep.20261101.14},

abstract = {Protection against financial risk is an essential pillar of Universal Health Coverage (UHC), particularly through the reduction of out-of-pocket payments that can lead to catastrophic health expenditure (CHE). This study aims to identify the determinants of CHE among households in Côte d'Ivoire. We conducted a cross-sectional analytical study using data from the 2021 Harmonized Household Living Conditions Survey (HLCS) (secondary analysis). The survey is based on a two-stage probability sampling method; 1,084 clusters and 13,008 households were initially selected, and 12,965 households were retained after validation. CHE was defined according to the "ability to pay" approach: a dichotomous variable (CHE=1) when OOPCAP = OOP/CAP ≥ 40%, otherwise CHE=0. Descriptive statistics, a bivariate Chi² test and binary logistic regression were used (Stata 17). Households spend more than half of their consumption expenditure on food (52.2%). The frequency of CHE is low: 0.11% in the total sample (14 households) and 0.35% among those who received direct payments. The concentration curve indicates a relatively homogeneous distribution (Gini = 0.187). The logistic model is significant (Chi² = 38.38; p 7). Conversely, households headed by a married person have an increased risk (OR = 5.27), as do those residing in rural areas (OR = 4.72). With regard to standard of living, the upper quintiles show odds ratios below 1 (Q2 to Q5), suggesting better financial protection, although some associations are of marginal significance. No significant link is observed for the gender of the head of household or for residence in Abidjan. CHE are rare, but their distribution remains socially differentiated: increased risk in rural areas, increased vulnerability when the head of household is married, and a protective effect of household size, linked to intra-family mutualization. A socioeconomic gradient also appears, with wealthier households being less exposed, but the significance is marginal. These results call for strengthening financial protection, especially in rural areas, and interpreting CHE with caution, given their rarity and sensitivity to methodological choices.},

year = {2026}

}

TY - JOUR T1 - Factors Associated with Catastrophic Health Expenditure Among Households in Côte d'Ivoire AU - Koffi Kouame AU - Attia-Konan Akissi Regine AU - Kouame Jerome AU - Sangare Abou Dramane AU - Oga Stephane Serge AU - Kouadio Luc Y1 - 2026/03/19 PY - 2026 N1 - https://doi.org/10.11648/j.hep.20261101.14 DO - 10.11648/j.hep.20261101.14 T2 - International Journal of Health Economics and Policy JF - International Journal of Health Economics and Policy JO - International Journal of Health Economics and Policy SP - 40 EP - 48 PB - Science Publishing Group SN - 2578-9309 UR - https://doi.org/10.11648/j.hep.20261101.14 AB - Protection against financial risk is an essential pillar of Universal Health Coverage (UHC), particularly through the reduction of out-of-pocket payments that can lead to catastrophic health expenditure (CHE). This study aims to identify the determinants of CHE among households in Côte d'Ivoire. We conducted a cross-sectional analytical study using data from the 2021 Harmonized Household Living Conditions Survey (HLCS) (secondary analysis). The survey is based on a two-stage probability sampling method; 1,084 clusters and 13,008 households were initially selected, and 12,965 households were retained after validation. CHE was defined according to the "ability to pay" approach: a dichotomous variable (CHE=1) when OOPCAP = OOP/CAP ≥ 40%, otherwise CHE=0. Descriptive statistics, a bivariate Chi² test and binary logistic regression were used (Stata 17). Households spend more than half of their consumption expenditure on food (52.2%). The frequency of CHE is low: 0.11% in the total sample (14 households) and 0.35% among those who received direct payments. The concentration curve indicates a relatively homogeneous distribution (Gini = 0.187). The logistic model is significant (Chi² = 38.38; p 7). Conversely, households headed by a married person have an increased risk (OR = 5.27), as do those residing in rural areas (OR = 4.72). With regard to standard of living, the upper quintiles show odds ratios below 1 (Q2 to Q5), suggesting better financial protection, although some associations are of marginal significance. No significant link is observed for the gender of the head of household or for residence in Abidjan. CHE are rare, but their distribution remains socially differentiated: increased risk in rural areas, increased vulnerability when the head of household is married, and a protective effect of household size, linked to intra-family mutualization. A socioeconomic gradient also appears, with wealthier households being less exposed, but the significance is marginal. These results call for strengthening financial protection, especially in rural areas, and interpreting CHE with caution, given their rarity and sensitivity to methodological choices. VL - 11 IS - 1 ER -

Department of Analytical Sciences and Public Health, Felix Houphouet-Boigny University, Abidjan, Cote d’Ivoire

Research Fields: Healthcare funding and financial protection 1-1, Health Technology Assessment (HTA) 1-2, Request for care, access, and use of services 1-3

Department of Analytical Sciences and Public Health, Felix Houphouet-Boigny University, Abidjan, Cote d’Ivoire

Research Fields: Request for care, access, and use of services 2-1, Healthcare funding and financial protection 2-2, Equity, inequality and social justice in health 2-3

Department of Analytical Sciences and Public Health, Felix Houphouet-Boigny University, Abidjan, Cote d’Ivoire

Research Fields: Healthcare funding and financial protection 3-1, Request for care, access, and use of services 3-2

Department of Public Health, Felix Houphouet-Boigny University, Abidjan, Cote d’Ivoire

Department of Analytical Sciences and Public Health, Felix Houphouet-Boigny University, Abidjan, Cote d’Ivoire

Department of Analytical Sciences and Public Health, Felix Houphouet-Boigny University, Abidjan, Cote d’Ivoire

Information