1. Introduction

Microfinance institutions (MFIs) have been considered as the key drivers of economic expansion and poverty extraction, especially in developing nations where traditional banking is not accessible to a large percentage of the inhabitants

| [5] | Aladejebi, O. (2019). The impact of microfinance banks on the growth of small and medium enterprises in Lagos Metropolis. European Journal of Sustainable Development, 8(3), 261-261. |

[5]

. The last several decades have seen the world increasingly teem with MFIs, which have transformed the financial inclusion realm fundamentally and inextricably since they made it possible to feed millions of micros, small and medium enterprises (MSMEs) with the capital they need to grow, innovate, and create jobs

| [8] | Ben, I., & Mansouri, F. (2019). Performance of microfinance institutions in the MENA region: a comparative analysis. International Journal of Social Economics, 46(1), 47-65. |

[8]

. In Sub-Saharan Africa and Nigeria, in particular, the significance of the MFIs is even stronger due to the continued high rate of financial exclusion, as the World Bank (2022) indicates that more than 40 per cent of adults are still unbanked. The MSME sector of Nigeria generates about 48 per cent of the national income, provides more than 80 per cent of employment and also runs high activities of the informal economy of the country

| [4] | Akinyele, O. D., Oloba, O. M., & Mah, G. (2022). Drivers of unemployment intensity in sub-Saharan Africa: do government intervention and natural International Journal of Research in Agriculture and resources matter?. Review of Economics and Political Forestry, 5(8); 21-28. Science, (ahead-of-print). |

[4]

.

MSMEs in Nigeria also challenge access to finance, despite its critical importance to their economy, based on the evidence that policymakers are advocating the use of microfinance as an effective mechanism to overcome the financing gap. In addition to the availability of capital, the effectiveness of MFIs is essential as well: very inefficient MFIs may result in high operational expenses, an unviable lending strategy and eventually, ineffective contribution to the modified performance of MSMEs

| [11] | Bolarinwa, J. B., Ogundana, F. O, & Anjola, O. A (2018). Access to Credits by Rural Coastal Dwellers through Microfinancing: A Key to Tourism and Recreational Fisheries Development in Nigeria. |

[11]

.

Considering the ongoing macroeconomic issues in Nigeria, it is of high policy and academic concern to know whether MFIs are efficient in providing financial services and whether this will be converted into real MSME development. Accordingly, a comparative analysis which critically assesses the operational performance of various MFIs and directly correlates the same outcome of performance to the MSMEs is significant to the literature of both microfinance and development finance by filling the much-needed gap in knowledge

| [20] | Mata, M. N., Shah, S. S. H., Sohail, N., & Correira, A. B. (2023). The effect of financial development and MFI’s characteristics on the efficiency and sustainability of micro financial institutions. Economies, 11(3), 78. |

| [22] | Muthoni, M. P., Mutuku, L., & Riro, G. K. (2017). Influence of loan characteristics on microcredit default in Kenya: A comparative analysis of microfinance institutions and financial intermediaries. |

[20, 22]

.

Although microfinance institutions (MFIs) have expanded significantly in Nigeria and other emerging economies, researchers have increasingly pointed out a troubling disconnect between the perceived benefits of microfinance and the actual performance improvements experienced by micro, small, and medium enterprises (MSMEs) that access these services

| [29] | Sharif M. (2018). A Study on the Performance of Microfinance Institutions in India. International Academic Journal of Accounting and Financial Management, 5(4), 116-128. |

[29]

. MFIs are designed to provide affordable financial products to underserved entrepreneurs; however, their operational models often fall short, becoming inefficient and undermining their developmental mandate

| [10] | Blanco, A. J., Irimia-Diéguez, A. I., & Vázquez-Cueto, M. J. (2023). Is there an optimal microcredit size to maximize the social and financial efficiencies of microfinance institutions?. Research in International Business and Finance, 65, 101980. |

[10]

.

In Nigeria, several systemic issues plague the microfinance sector, including poor governance, limited technical capacity, regulatory non-compliance, and, in some cases, outright fraud. These challenges have led to widespread insolvencies and eroded client confidence

| [15] | Hasan, N., Singh, A. K., Agarwal, M. K., & Kushwaha, B. P. (2025). Evaluating the role of microfinance institutions in enhancing the livelihood of urban poor. Journal of Economic and Administrative Sciences, 41(1), 114-131. |

[15]

. Simultaneously, MSMEs struggle with a high failure rate estimated at 70% within the first five years, primarily due to limited access to finance, high interest rates, and inadequate business support services

| [13] | Ekpo, V., & Ebewo, P. E. (2024). The Influence of Microfinance Institutions on Nigerian Small, Micro, and Medium Enterprises. IJEBD (International Journal of Entrepreneurship and Business Development), 7(2), 209-214. |

[13]

.

Existing research has typically treated MFI efficiency and MSME performance as separate areas of inquiry, resulting in limited empirical evidence on how variations in MFI performance influence both financial and non-financial outcomes for their clients. Furthermore, few studies have conducted comparative analyses of different MFI models, such as cooperative societies, microfinance banks, and NGO-based lenders, despite their varying operational structures and target populations

| [20] | Mata, M. N., Shah, S. S. H., Sohail, N., & Correira, A. B. (2023). The effect of financial development and MFI’s characteristics on the efficiency and sustainability of micro financial institutions. Economies, 11(3), 78. |

[20]

.

This lack of integrated and comparative evidence restricts the ability of policymakers and stakeholders to design targeted reforms that enhance both institutional sustainability and MSME outcomes. Therefore, this study seeks to address a critical research gap by evaluating how differences in the efficiency of various MFIs influence MSME performance in Nigeria, and by extension, other emerging economies facing similar structural challenges.

1.1. Research Aim and Objectives

The aim of the study is to add value to the comparative analysis of the operational efficiency of microfinance establishments and the resultant effect on the performance of micro, small and medium enterprises through Nigeria as a proxy of emerging economies. To fulfil this purpose, this study will be undertaken with a view to fulfilling the following objectives:

i) In measuring the relative rate of efficiency among varieties of MFIs that have been run in Nigeria, the application of powerful quantitative tools like Data Envelopment Analysis (DEA) and Stochastic Frontier (SFA) to produce efficiency scores projected on the operation sustainability and optimisation of resources will be of benefit. ii) In the context of evaluating the performance of the MSMEs, which are sustained through the financing of these institutions, the main parameters should be based on the following aspects, such as revenue growth, employment generation, business survival rates, and productivity increases. iii) To examine the quality and the intensity of the connection between MFI efficiency and MSME performance. iv) To give evidence-based policy suggestions to regulators and MFI managers, and development practitioners to help in the assessment of institutional effectiveness and to support the resilience and growth of MSMEs.

1.2. Research Questions

In line with the above-stated aim and objectives, the present study attempts to answer a set of formulated research questions and to test the hypotheses that are formulated, which are based on the empirical independence of the study. The research questions are cascaded below:

i) What are the current efficiency levels of various categories of microfinance institutions operating in Nigeria, and how do they compare across institutional types and geographic regions? ii) To what extent do variations in MFI efficiency impact the financial and operational performance of micro, small and medium enterprises that depend on micro-finance services? iii) What contextual or institutional factors mediate or moderate the relationship between MFI efficiency and MSME performance outcomes?

1.3. Significance of the Research

Since no sufficient empirical research has been conducted on the impact of microfinance bank efficiency on MSMEs during the first six years of regulatory changes' initiation from 2018 to 2024, this study fills a significant gap in the literature. Most notably, the MSME fund intervention initiatives in Nigeria run by the Central Bank of Nigeria (CBN) and the following regulatory reforms: risk-based supervision, agent banking relationships, a national plan for financial inclusion (including consumer protection and financial literacy), and so on. This research looks at six states in southwestern Nigeria: Lagos, Oyo, Osun, Ogun, Ondo, and Ekiti. It also looks at the microfinance banks in these areas and the entrepreneurs that utilise them, especially those who have asked for government intervention loans.

Another important takeaway from the research is the expanded perspective it offers on the role of microfinance institutions in bolstering MSMEs. This study goes beyond previous research by investigating how the efficiency of microfinance banks affects the performance of micro, small, and medium-sized enterprises (MSMEs), as opposed to focusing just on the demand side of such evaluations. Issues about the demand and supply sides of microfinance will also be discussed, as well as how a well-functioning industrial subsector might improve its efficiency.

2. Literature Review

2.1. Theoretical Review

This study draws on a multi-theoretical framework comprising the Financial Intermediation Theory (FIT), Pecking Order Theory (POT), and Resource-Based Theory (RBT). These theories collectively provide a robust foundation for understanding how MFIs influence the performance of MSMEs, particularly through efficiency, access to finance, and resource optimisation.

2.1.1. Financial Intermediation Theory

A study proposed the notion of financial intermediation to address the problems with direct funding

| [22] | Muthoni, M. P., Mutuku, L., & Riro, G. K. (2017). Influence of loan characteristics on microcredit default in Kenya: A comparative analysis of microfinance institutions and financial intermediaries. |

[22]

. Firms that would have trouble obtaining financing on their own could benefit greatly from the services of financial intermediaries like microfinance organisations, according to this hypothesis

| [10] | Blanco, A. J., Irimia-Diéguez, A. I., & Vázquez-Cueto, M. J. (2023). Is there an optimal microcredit size to maximize the social and financial efficiencies of microfinance institutions?. Research in International Business and Finance, 65, 101980. |

[10]

. According to this theory, organisations that act as middlemen between savers and borrowers can provide credit to businesses and people who may not have access to it otherwise

| [26] | Rajapakshe, W. (2021). The Role of Micro Finance Institutions on the Development of Micro Enterprises (MEs) in Sri Lanka. |

[26]

. When applied to the Nigerian microfinance sector, Financial Intermediation Theory clarifies the role of microfinance institutions in expanding MSMEs' access to capital. Mobilising savings and lending them out to borrowers are two ways these organisations help people and businesses become part of the formal financial system. According to the theory, small businesses can invest and expand because financial intermediaries make it easier for them to get the loans they need. It also gives a structure for figuring out how microcredit affected the efficiency of Nigerian MSMEs.

2.1.2. Pecking Order Theory

Donaldson proposed the pecking order theory (POT) in 1961, and Myers and Nicolas revised it in 1984. This theory explains how businesses get the funds necessary to make investments and capital expenditures. According to

| [20] | Mata, M. N., Shah, S. S. H., Sohail, N., & Correira, A. B. (2023). The effect of financial development and MFI’s characteristics on the efficiency and sustainability of micro financial institutions. Economies, 11(3), 78. |

[20]

, companies tend to finance their investments using internal funds first, then borrowed funds, and finally equity funds. The term "internal financing" describes how a business pays for new ventures and investments using its own retained revenues and other income. The pecking order hypothesis states that, in comparison to external finance, which is both more costly and hazardous, internal financing is preferable for enterprises

| [27] | Roslan, S., Zainal, N., & Mahyideen, J. M. (2021). Impact of macroeconomic conditions on financial efficiency of microfinance institutions: evidence from pre and post-financial crisis. Journal of Technology Management and Technopreneurship (JTMT), 9(1), 32-47. |

[27]

.

Internal financing allows businesses to save money on capital expenditures by avoiding the need to pay interest or dividends to outside investors. Additionally, the danger of financial trouble is reduced with internal financing since it does not require extra debt. The capacity of the pecking order hypothesis to describe corporate behaviour when it comes to financing choices is one of its strengths. A review of the literature reveals that companies would rather raise capital internally than from outside sources, and that when they do seek outside funding, they lean more toward debt than stock

| [22] | Muthoni, M. P., Mutuku, L., & Riro, G. K. (2017). Influence of loan characteristics on microcredit default in Kenya: A comparative analysis of microfinance institutions and financial intermediaries. |

[22]

.

According to the pecking order idea, businesses would rather use internal resources like savings, profits, and retained earnings to fund investments than use outside sources like loans or equity. When evaluating how microcredit impacts the productivity of Tanzania, this idea becomes pertinent. Before turning to microcredit providers for funding, MSMEs may want to spend money already on hand. Thus, while this theory might shed light on how MSMEs in Iringa Municipality, Tanzania, make their financing choices, it's crucial to take into account the specific institutional and economic elements that may impact these businesses' financing behaviour

| [17] | Ikechukwu & Elizabeth (2019). Formal credits access and farmers welfare in Plateau State, Nigeria. International Journal of Mechanical Engineering and Technology (IJMET), 10(2), 302-313. |

[17]

. To do this, there is a need to learn more about the regional market and the specific financing requirements of MSMEs.

2.1.3. The Resource-based Theory

Penrose first presented Resource-Based Theory (RBT) as a model for managing a company's resources, diversification strategy, and productive prospects effectively. According to the theory, a company may get an edge in the market and perform better overall by capitalising on its distinct strengths. A company's success is based on its ability to make good use of its resources, which may be either physical or intangible, according to the RBT

| [23] | Olarinwa, S. T., Akinyele, O., & Vo, X. V. (2021). Determinants of nonperforming loans after recapitalization in the Nigerian banking industry: Does efficiency matter?. Managerial and Decision Economics, 42(6), 1509-1524. |

[23]

. A valuable, rare, inimitable, and non-substitutable resource (VRIN) is one way that enterprises might gain and maintain a competitive edge, according to the RBT. This theory, as it pertains to microcredit and MSMEs in Kenya, postulates that businesses would be better able to compete and perform better if they use microcredit to build upon and improve their current resources and capacities.

MSMEs in Nigeria, and Plateau State in particular, might benefit from applying this approach to their evaluation of microcredit's impact on their performance

| [13] | Ekpo, V., & Ebewo, P. E. (2024). The Influence of Microfinance Institutions on Nigerian Small, Micro, and Medium Enterprises. IJEBD (International Journal of Entrepreneurship and Business Development), 7(2), 209-214. |

[13]

. Researchers and policymakers may learn more about what variables affect business performance in this setting by looking at the skills and resources of MSMEs in Plateau State and how well they are using microcredit resources.

| [24] | Onyekwelu, P. N., Ibe, G. I., Monyei, F. E., Attamah, J. I., & Ukpere, W. I. (2023). The impact of entrepreneurship institutions on access to micro-financing for sustainable enterprise in an emerging economy. Sustainability, 15(9), 7425. |

[24]

discovered that microcredit may SMEs in Tanzania improve their performance by expanding their skills.

2.1.4. Complementary Perspective of the Theories

Financial intermediation theory, resource-based theory (RBT), and pecking order theory are three theories that provide complementary viewpoints on how businesses manage their resources and make financing decisions. The role of financial institutions in transferring money from savers to borrowers is the main focus of financial intermediation theory, whereas RBT highlights how crucial a company's distinct assets and skills are to gaining a competitive edge. In contrast, a hierarchy of funding preferences is described by the pecking order theory, whereby businesses prioritise internal money before pursuing external loans and equity

| [25] | Primiana, I., Masyita, D., & Febrian, E. (2018). Comparative study οn sustainability of sharia microfinance institutions through financial and social efficiency. |

[25]

. Pecking order and financial intermediation theories draw attention to the intricate dynamics of business funding choices. While resource-based theory stresses the use of unique resources for a competitive advantage, financial institutions help to enable capital movement. According to the Pecking Order Theory, companies favour internal resources over outside funding.

2.2. Conceptual Review

2.2.1. Micro, Small and Medium Scale Enterprises

There is a consensus that small and medium-sized enterprises (SMEs) constitute the driving force behind economic growth

| [24] | Onyekwelu, P. N., Ibe, G. I., Monyei, F. E., Attamah, J. I., & Ukpere, W. I. (2023). The impact of entrepreneurship institutions on access to micro-financing for sustainable enterprise in an emerging economy. Sustainability, 15(9), 7425. |

[24]

. Their work is vital in boosting economic growth because it helps with things like reducing poverty, creating jobs, raising living standards, distributing income fairly, encouraging innovation, adding value, building connections across different regions' sectors, and encouraging local communities to accumulate capital. The criteria used to ascertain the size of a company differ from one country to another. When classifying MSMEs in Nigeria, the National Policy on MSMEs takes the whole workforce and assets (not including land and buildings) into account

| [10] | Blanco, A. J., Irimia-Diéguez, A. I., & Vázquez-Cueto, M. J. (2023). Is there an optimal microcredit size to maximize the social and financial efficiencies of microfinance institutions?. Research in International Business and Finance, 65, 101980. |

[10]

. Companies that have ten or fewer employees and assets of less than five million Nigerian naira are considered micro-businesses according to the regulation.

2.2.2. Microfinance

Microfinance is defined by

| [15] | Hasan, N., Singh, A. K., Agarwal, M. K., & Kushwaha, B. P. (2025). Evaluating the role of microfinance institutions in enhancing the livelihood of urban poor. Journal of Economic and Administrative Sciences, 41(1), 114-131. |

[15]

as the provision of financial services to MSMEs unserved by traditional banks. As such, it is a genuine means of reducing poverty and increasing employment opportunities. Lack of capital is a major obstacle for MSMEs in Nigeria. Most MSMEs lack the collateral necessary to obtain accessible credit facilities. As a consequence, many of them have closed their doors, cutting into Nigeria's workforce of both highly trained professionals and others with less formal education

| [24] | Onyekwelu, P. N., Ibe, G. I., Monyei, F. E., Attamah, J. I., & Ukpere, W. I. (2023). The impact of entrepreneurship institutions on access to micro-financing for sustainable enterprise in an emerging economy. Sustainability, 15(9), 7425. |

[24]

. Loans, deposits, payment services, and insurance are all part of microfinance's extensive list of financial offerings to low-income families and microenterprises (MEs). The low-income have benefited greatly from microfinance organisations' ability to increase their income and, by extension, their quality of life

| [16] | Hermes, N., Lensink, R., & Meesters, A. (2018). Financial development and the efficiency of microfinance institutions. In Research Handbook on Small Business Social Responsibility (pp. 177-205). Edward Elgar Publishing. |

[16]

.

A number of characteristics distinguish microfinance credit from other types of credit, including the accessibility of the loans, the modest amount of the loans, and the absence of collateral requirements. In 2005, the Microfinance Policy Regulatory and Supervisory Framework (MPRSF) was established in response to the early inadequacies of community banks in providing sufficient lending facilities

| [26] | Rajapakshe, W. (2021). The Role of Micro Finance Institutions on the Development of Micro Enterprises (MEs) in Sri Lanka. |

[26]

. The number of MFIs in Nigeria increased after this, since MFIs were required to get licenses in 2018. Just as with previous community banks, the new MFIs had problems that led to their demise. In 2020, 324 MFIs had their licenses revoked due to poor performance, which ultimately led to the bankruptcy of these institutions. Undercapitalization, ineffective management, and regulatory and supervisory gaps were among the difficulties encountered by MFIs

| [21] | Mia, M. A., Rangel, G. J., Nourani, M., & Kumar, R. (2023). Institutional factors and efficiency performance in the global microfinance industry. Benchmarking: An International Journal, 30(2), 433-459. |

[21]

.

2.3. Empirical Review

The relationship between Microfinance Institutions (MFIs) and the financing of Micro, Small, and Medium Enterprises (MSMEs) is well-documented in the literature. However, scholars report mixed empirical evidence regarding the developmental impact of MSMEs supported by microfinance, particularly in emerging economies like Nigeria. For instance, a study conducted in Damaturu, Yobe State, by

| [22] | Muthoni, M. P., Mutuku, L., & Riro, G. K. (2017). Influence of loan characteristics on microcredit default in Kenya: A comparative analysis of microfinance institutions and financial intermediaries. |

[22]

investigated the role of MFIs in fostering SME growth. Using a survey method, the researchers distributed 50 questionnaires, of which 41 were validly completed and returned. The data were analysed using chi-square tests, which revealed that stringent borrowing requirements imposed by banks significantly discouraged MSMEs from accessing traditional financial institutions. This suggests that access constraints persist, and MFIs, despite their intended function, may not fully bridge the financial inclusion gap if lending conditions remain unfavourable.

Using Jos Metropolis as a case study,

| [19] | Lwesya, F., & Mwakalobo, A. B. S. (2023). Frontiers in microfinance research for small and medium enterprises (SMEs) and microfinance institutions (MFIs): a bibliometric analysis. Future Business Journal, 9(1), 17. |

[19]

investigated how microfinance impacted the development of entrepreneurial businesses in Nigeria. The study was conducted using a descriptive approach, and the hypotheses were tested using one-sample t-test statistics. Researchers found that entrepreneurial businesses' market share was significantly affected by microfinance money transfer, and that entrepreneurial businesses' diversification was significantly affected by microfinance loans.

Finally, the impact of microfinance financial assistance on the operational efficiency of entrepreneurial companies was clearly shown. The impact of microfinance bank loans on MSMEs in Alimosho LGA, Lagos State

| [17] | Ikechukwu & Elizabeth (2019). Formal credits access and farmers welfare in Plateau State, Nigeria. International Journal of Mechanical Engineering and Technology (IJMET), 10(2), 302-313. |

[17]

. In order to test the research hypotheses, 387 SMEs in Alimosho LGA, Lagos State, participated in the study. Data was collected using a structured questionnaire. The data was analysed using descriptive statistics and a basic regression technique. The results showed that the profitability of chosen SMEs in the Alimosho local government area of Lagos State is strongly affected by MFB loans and MFB loan debt payments.

The effect of microfinance services on the productivity of SMEs in the Zaria metropolitan area was investigated by

| [10] | Blanco, A. J., Irimia-Diéguez, A. I., & Vázquez-Cueto, M. J. (2023). Is there an optimal microcredit size to maximize the social and financial efficiencies of microfinance institutions?. Research in International Business and Finance, 65, 101980. |

[10]

. This study used a descriptive and cross-sectional research strategy. Within the Zaria Metropolis, 300 SMEs who are clients of Cred Microfinance Bank were chosen at random. A questionnaire was used as the primary data-gathering tool. The data was processed using SPSS 20.0 for regression analysis. The research found that MSMEs in the Zaria metropolis' entrepreneurial activity levels are significantly affected by microfinance services. Research conducted in the West District, Ghana, by

| [26] | Rajapakshe, W. (2021). The Role of Micro Finance Institutions on the Development of Micro Enterprises (MEs) in Sri Lanka. |

[26]

examined the impact of microfinance and small loans on alleviating poverty. We used a single case study design. Forty MASLOC beneficiaries and officials participated in the data collection process via observation and interview.

By applying thematic analysis to the data, interesting themes and patterns were unearthed. As a result of its effects on income, consumption, access to basic needs, and asset accumulation, MASLOC was determined to have been an important factor in reducing poverty. Particular difficulties were also brought to light by the results. Problems with employment and loan repayments surfaced as limitations of the MASLOC model.

| [24] | Onyekwelu, P. N., Ibe, G. I., Monyei, F. E., Attamah, J. I., & Ukpere, W. I. (2023). The impact of entrepreneurship institutions on access to micro-financing for sustainable enterprise in an emerging economy. Sustainability, 15(9), 7425. |

[24]

looked at how the actions of microfinance institutions affected the happiness of female business owners. They used a causal design for this investigation. The research surveyed four hundred and two (402) female business owners in Yola metropolitan using questionnaires.

Descriptive statistics, including tabular presentations of percentages and frequencies, and inferential statistics, with the aid of SPSS at a 0.05 (5%) level of significance, were applied to the data acquired for this study. Credit facilities, loan repayment plans, interest rates, skill training, and supervisory positions all had a major impact on the happiness of women entrepreneurs in Adamawa State, Nigeria, according to the study's results. Micro and small businesses in Cavite were studied by

| [3] | Agaba, A. M., & Mugarura, E. (2023). Microfinance Institution Services and Performance of Small and Medium Enterprises in Kabale District Uganda. International Journal of Entrepreneurship and Business Management, 2(1), 1-18. |

| [9] | Bharti, N., & Malik, S. (2022). Financial inclusion and the performance of microfinance institutions: does social performance affect the efficiency of microfinance institutions?. Social Responsibility Journal, 18(4), 858-874. |

| [19] | Lwesya, F., & Mwakalobo, A. B. S. (2023). Frontiers in microfinance research for small and medium enterprises (SMEs) and microfinance institutions (MFIs): a bibliometric analysis. Future Business Journal, 9(1), 17. |

[3, 9, 19]

to see how microfinance institutions affected their growth.

The research used a descriptive approach and a purposive sample strategy. Fifty microfinance institutions in the Cavite region made up the study's sample size. In terms of implementation, the research found that microfinance institutions helped micro and small businesses thrive by increasing their capital. Micro and small businesses that were in need of assistance were helped by microfinance institutions via monitoring

| [1] | Abdullah, W. M. Z. B. W., Zainudin, W. N. R. A. B., Ismail, S. B., & Zia-Ul-Haq, H. M. (2022). The impact of microfinance services on Malaysian B40 households’ socioeconomic performance: A moderated mediation analysis. International Journal of Sustainable Development and Planning, 17(6), 1983-1996. |

| [19] | Lwesya, F., & Mwakalobo, A. B. S. (2023). Frontiers in microfinance research for small and medium enterprises (SMEs) and microfinance institutions (MFIs): a bibliometric analysis. Future Business Journal, 9(1), 17. |

[1, 19]

. The importance of MFIs in assisting micro and small businesses in innovating their capital goods was also outlined in the sustainability of operations report.

People used Gujarat as a case study to assess the impact of microfinance on SMEs in the state. Sixty MFIs and one hundred forty MSMEs were selected for the research using a simple random selection technique

| [17] | Ikechukwu & Elizabeth (2019). Formal credits access and farmers welfare in Plateau State, Nigeria. International Journal of Mechanical Engineering and Technology (IJMET), 10(2), 302-313. |

| [25] | Primiana, I., Masyita, D., & Febrian, E. (2018). Comparative study οn sustainability of sharia microfinance institutions through financial and social efficiency. |

[17, 25]

. In order to facilitate the collection of relevant data for analysis, a structured questionnaire was developed. The employment of descriptive statistics, which makes use of simple bar graphs and pie charts to depict and analyse data, has been deliberate. MSMEs are reluctant to engage because, according to the study's results, financial institutions do not consider MSMEs' viewpoints when formulating loan regulations

| [16] | Hermes, N., Lensink, R., & Meesters, A. (2018). Financial development and the efficiency of microfinance institutions. In Research Handbook on Small Business Social Responsibility (pp. 177-205). Edward Elgar Publishing. |

[16]

. This is why it is poorly suited to the needs of MSMEs and why it contributes significantly to the problems plaguing credit management. High interest rates and other expenses make it hard for small and medium firms to produce strong profits to pay off their loans, according to the research.

In addition, the results showed that certain MSMEs are unable to get loans due to the preferred collateral of MFIs. Additionally, the majority of MSMEs are unable to seek loans from MFIs due to a lack of collateral.

| [23] | Olarinwa, S. T., Akinyele, O., & Vo, X. V. (2021). Determinants of nonperforming loans after recapitalization in the Nigerian banking industry: Does efficiency matter?. Managerial and Decision Economics, 42(6), 1509-1524. |

| [24] | Onyekwelu, P. N., Ibe, G. I., Monyei, F. E., Attamah, J. I., & Ukpere, W. I. (2023). The impact of entrepreneurship institutions on access to micro-financing for sustainable enterprise in an emerging economy. Sustainability, 15(9), 7425. |

[23, 24]

looked at how microcredit affected the performance of certain MSMEs in Iringa Municipality, Tanzania. The study used a descriptive research approach. A total of 874 MSMEs that have benefited from microcredit services offered by Iringa Municipality were the intended subjects of the study.

A total of 274 MSMEs were selected from this population by using a combination of stratified, simple random, and convenience selection techniques. The data was analysed using a quantitative technique. The results showed that MSMEs in Iringa Municipality can increase their performance thanks to the loans they obtain from financing institutions

| [15] | Hasan, N., Singh, A. K., Agarwal, M. K., & Kushwaha, B. P. (2025). Evaluating the role of microfinance institutions in enhancing the livelihood of urban poor. Journal of Economic and Administrative Sciences, 41(1), 114-131. |

| [22] | Muthoni, M. P., Mutuku, L., & Riro, G. K. (2017). Influence of loan characteristics on microcredit default in Kenya: A comparative analysis of microfinance institutions and financial intermediaries. |

[15, 22]

. Also, the research concluded that interest rate does not significantly affect the efficiency of MSMEs in Iringa Municipality. The results also showed that the impacts of starting capital on MSMEs' performance were statistically significant.

With an adjusted R2 of 0.698 for normal regression output, we may deduce that the model accounts for about 69.8 per cent of the variance in MSMEs' performance.

| [13] | Ekpo, V., & Ebewo, P. E. (2024). The Influence of Microfinance Institutions on Nigerian Small, Micro, and Medium Enterprises. IJEBD (International Journal of Entrepreneurship and Business Development), 7(2), 209-214. |

| [29] | Sharif M. (2018). A Study on the Performance of Microfinance Institutions in India. International Academic Journal of Accounting and Financial Management, 5(4), 116-128. |

[13, 29]

evaluated the role of microfinance institutions in helping Tanzanian SMEs expand. In order to gather all the necessary information, a cross-sectional study method was used, and 231 participants were polled. The data was analysed using descriptive statistics and Multiple Regression Analysis (MRA), and the findings were presented visually using graphs and tables. When it comes to providing services to SMEs, the results showed that MFIs are crucial.

With a focus on Cross River State, Nigeria,

| [12] | Deb, J., & Sinha, R. P. (2022). Impact of competition on efficiency of microfinance institutions: Cross country comparison of India and Bangladesh. International Journal of Rural Management, 18(2), 250-270. |

| [30] | Soldátková, N., & Černý, M. (2022). Microfinance in Sub-Saharan Africa: social efficiency, financial efficiency and institutional factors. Central European Journal of Operations Research, 30(2), 449-477. |

| [31] | Yahaya, A. A., & Kolawole, K. D. (2022). Impact of Microfinance Banks’ Facilities on Performance of Small and Medium Scale Enterprises in Nigeria. Lapai International Journal of Management and Social Sciences, 14(2), 34-43. |

[12, 30, 31]

studied how microfinance institutions affected the expansion of small businesses. The study used a descriptive survey as its research design. Questionnaires and in-person interviews were the means of data collection. Pearson product-moment correlation and simple percentage analysis were used to examine the gathered data. Microfinance banks' services influenced the growth of small businesses, according to the study's findings

| [20] | Mata, M. N., Shah, S. S. H., Sohail, N., & Correira, A. B. (2023). The effect of financial development and MFI’s characteristics on the efficiency and sustainability of micro financial institutions. Economies, 11(3), 78. |

[20]

. To boost customer loyalty, research shows that microfinance institutions aren't doing enough to raise public awareness. Research shows that small company owners who take out loans from microfinance institutions seldom utilise the money to expand their operations.

Microfinance institutions in Southeast Nigeria were studied by

| [11] | Bolarinwa, J. B., Ogundana, F. O, & Anjola, O. A (2018). Access to Credits by Rural Coastal Dwellers through Microfinancing: A Key to Tourism and Recreational Fisheries Development in Nigeria. |

| [27] | Roslan, S., Zainal, N., & Mahyideen, J. M. (2021). Impact of macroeconomic conditions on financial efficiency of microfinance institutions: evidence from pre and post-financial crisis. Journal of Technology Management and Technopreneurship (JTMT), 9(1), 32-47. |

[11, 27]

to find out how they affected savings mobilisation, credit intermediation, and job creation. Primary data for the research came from questionnaires administered using a survey technique of inquiry. Microfinance banks significantly improve savings mobilisation, credit intermediation, and job creation among rural residents of Southeast Nigeria, according to a Z-test analysis of the collected data. Microfinance bank development positively affects the economic activities of Nigerians living in rural areas, according to the study's authors

| [6] | Audu, I., Abubakar, A. M., & Baba, M. (2021). The Role of Microfinance Institutions’ Services on the Performance of Small and Medium Entreprises in Gombe State, Nigeria. Journal of Management Sciences, 4(1), 500-517. |

[6]

.

2.4. Identified Gaps in Literature

The debate about MFIs and their efficiency has become an area of serious scholarly research, with the former playing a significant role in achieving financial inclusion and triggering the development of micro, small, and medium-sized enterprises, especially in the emerging markets

| [4] | Akinyele, O. D., Oloba, O. M., & Mah, G. (2022). Drivers of unemployment intensity in sub-Saharan Africa: do government intervention and natural International Journal of Research in Agriculture and resources matter?. Review of Economics and Political Forestry, 5(8); 21-28. Science, (ahead-of-print). |

| [23] | Olarinwa, S. T., Akinyele, O., & Vo, X. V. (2021). Determinants of nonperforming loans after recapitalization in the Nigerian banking industry: Does efficiency matter?. Managerial and Decision Economics, 42(6), 1509-1524. |

[4, 23]

. The traditional theory of financial intermediation assumes that institutions such as MFIs neutralise market imperfection through the minimisation of information asymmetries and transaction costs of the underserved groups

| [7] | Babajide, A. A., Lawal, A. I., Somoye, R. O. & Nwanji, T. I. (2018). The effect of fiscal and monetary policies interaction on stock market performance: Evidence from Nigeria. Future Business Journal, 4(1), 16-33. |

[7]

. Nevertheless, through empirical studies, there has been mixed data on the reality of these goals being attained on a sustainable scale by MFIs.

As an example,

| [5] | Aladejebi, O. (2019). The impact of microfinance banks on the growth of small and medium enterprises in Lagos Metropolis. European Journal of Sustainable Development, 8(3), 261-261. |

[5]

declare that a significant part of the MFIs are subject to the high cost structure because of the labour-intensive outreach and the bad economics of scale that bring down the self-sufficiency of operations. With a sample of the MFIs located in the MENA region,

| [3] | Agaba, A. M., & Mugarura, E. (2023). Microfinance Institution Services and Performance of Small and Medium Enterprises in Kabale District Uganda. International Journal of Entrepreneurship and Business Management, 2(1), 1-18. |

| [26] | Rajapakshe, W. (2021). The Role of Micro Finance Institutions on the Development of Micro Enterprises (MEs) in Sri Lanka. |

| [31] | Yahaya, A. A., & Kolawole, K. D. (2022). Impact of Microfinance Banks’ Facilities on Performance of Small and Medium Scale Enterprises in Nigeria. Lapai International Journal of Management and Social Sciences, 14(2), 34-43. |

[3, 26, 31]

points out how inefficiencies occur and are reflected through inefficient loan portfolio quality and excessive default rates that may undermine the welfare of clients and financial sustainability. In Sub-Saharan Africa, academic studies have found that there is frequently a trade-off between financial sustainability and social outreach, and more commercially oriented MFIs have been demonstrating an ability to reach out to fewer poor clients than NGOs or cooperative MFIs

| [8] | Ben, I., & Mansouri, F. (2019). Performance of microfinance institutions in the MENA region: a comparative analysis. International Journal of Social Economics, 46(1), 47-65. |

[8]

.

Choosing to focus on Nigeria, the ongoing problem of governance and capacity gaps amid MFIs, citing the problem of undercapitalization, fraud, and non-compliance with regulations that further drive inefficiency

| [2] | Adebola, B. Y. (2021). Microfinance banks, small and medium scale enterprises and COVID-19 pandemic in Nigeria. European Journal of Economics, Law and Politics, 8(2), 1-10. |

| [19] | Lwesya, F., & Mwakalobo, A. B. S. (2023). Frontiers in microfinance research for small and medium enterprises (SMEs) and microfinance institutions (MFIs): a bibliometric analysis. Future Business Journal, 9(1), 17. |

[2, 19]

. The Central Bank of Nigeria has ambitious goals of a regulatory reform intended to enhance the sub-sector, but despite that, prevalent institutional weaknesses restrain the role of the sector in facilitating the real growth of MSMEs

| [9] | Bharti, N., & Malik, S. (2022). Financial inclusion and the performance of microfinance institutions: does social performance affect the efficiency of microfinance institutions?. Social Responsibility Journal, 18(4), 858-874. |

[9]

.

Concerning effects on MSME performance, empirical evidence is divided as well: some studies can unequivocally state the fact that the access to microfinance does have a positive effect on the business growth, sustaining income, and job creation

| [4] | Akinyele, O. D., Oloba, O. M., & Mah, G. (2022). Drivers of unemployment intensity in sub-Saharan Africa: do government intervention and natural International Journal of Research in Agriculture and resources matter?. Review of Economics and Political Forestry, 5(8); 21-28. Science, (ahead-of-print). |

[4]

, and those that note the minimal effects or the effects that cannot be considered significant (reminding that the lack of the positive effects can be explained by such factors as insufficient values of the loans, high levels of the interest rates, and it is demonstrated in the literature that the variety of MFIs (NGO-MFIs, microfinance banks, cooperative societies) has different operational features and cost models, but few comparative studies have been conducted that give systematic evaluations of the comparative efficiency of the various sources and the associated consequences on the performance of MSMEs in Nigeria.

To close this gap, researchers have called for to use of statistical methods of measuring efficiency like Data Envelopment Analysis (DEA) and Stochastic Frontier Analysis (SFA), which are more efficient in estimating the efficiency score that is devoid of bias, and allow comparisons across institutions

| [10] | Blanco, A. J., Irimia-Diéguez, A. I., & Vázquez-Cueto, M. J. (2023). Is there an optimal microcredit size to maximize the social and financial efficiencies of microfinance institutions?. Research in International Business and Finance, 65, 101980. |

| [16] | Hermes, N., Lensink, R., & Meesters, A. (2018). Financial development and the efficiency of microfinance institutions. In Research Handbook on Small Business Social Responsibility (pp. 177-205). Edward Elgar Publishing. |

[10, 16]

. Combining these quantitative measures results in seeking the performance of MSMEs within the companies through which we can specifically determine how effective institutions can drive actual economic outcomes. This synergy in approach remains underdeveloped in the existing body of literature. Having overcome this gap, the present synthesis establishes itself at the frontier between the discourse of microfinance institutional performance and enterprise development on one hand, and the regulatory supervision and strategic management of MFIs in Nigeria on one hand, which is particularly relevant to the calls of the greater necessity to provide the contextualized, empirically grounded evidence to inform the regulation policy as well as the future of strategic behaviour of MFIs in energy-consuming environments of nascent economies

| [1] | Abdullah, W. M. Z. B. W., Zainudin, W. N. R. A. B., Ismail, S. B., & Zia-Ul-Haq, H. M. (2022). The impact of microfinance services on Malaysian B40 households’ socioeconomic performance: A moderated mediation analysis. International Journal of Sustainable Development and Planning, 17(6), 1983-1996. |

[1]

.

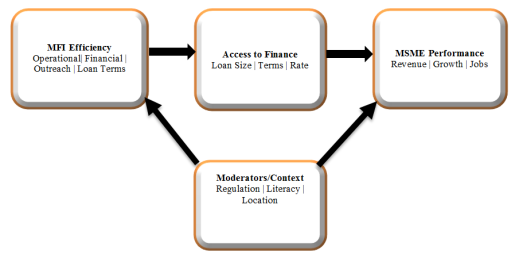

2.5. Conceptual Framework

Figure 1. Conceptual framework illustrating the relationship between MFI Efficiency, Access to Finance, and MSME Performance, moderated by contextual factors such as regulation and financial literacy.

3. Methodology

3.1. Estimation Procedures and Model Description

The effectiveness of microfinance institutions and the success of MSMEs in Nigeria were the subjects of this study. The research area encompasses the Southwestern geopolitical zone of Nigeria, which consists of six states and eighteen senatorial districts. Specifically, the microfinance institutions in the six states of Ekiti, Lagos, Ogun, Oyo, Osun, and Ondo, and the business owners who use these institutions, especially those who have sought government intervention loans. The Central Bank of Nigeria (CBN) reports that as of February 2024, 898 microfinance banks were operational in Nigeria. Among these microfinance institutions, 569 have full licenses and 329 have interim ones. Of these 359 microfinance institutions, 179 are operating under a provisional license and 180 are in the final licensing category; the majority, or 40%, are located in the Southwestern geopolitical zone.

In order to choose a sample for the multi-level sampling strategy, this research effort used a purposive sampling methodology. At its most fundamental level, descriptive research makes use of a deductive methodology in conjunction with an archival and documentary research strategy

| [18] | Kittur, J. (2023). Conducting quantitative research study: A step-by-step process. Journal of Engineering Education Transformations, 36(4), 100-112. |

[18]

. Microfinance banks make up one step of the sampling process, while the entrepreneurs who use their services make up the other. First, microfinance institutions are chosen at random from each senatorial district in all six states based on product type, size of client base, capitalisation, and balance sheet. Along with the specified number of microfinance operations, the placement of the microfinance banks in each senatorial district was also established by their business evaluation reports. Eighteen microfinance institutions were selected for the study, making up about 10% of the total licensed microfinance institutions in South-West Nigeria.

The second part of the research included taking into account a total of fourteen thousand MSMEs from eighteen senatorial districts in the states in the southwest of Nigeria. This population accounts for forty per cent of the thirty-seven million SMEs in Nigeria as a whole

| [14] | Ghanad, A. (2023). An overview of quantitative research methods. International journal of multidisciplinary research and analysis, 6(08), 3794-3803. |

[14]

. For sampling techniques, the advice of Krejcie and Morgan (1970) was followed, which states that a minimum acceptable sample size of 384 should be used when the population is 1,000,000 or more. Based on the available data, which shows that 36,770 company owners applied for the intervention loan, this research chose a sample of 1,000 microfinance bank entrepreneurs from the eighteen senatorial districts in Southwest Nigeria

| [28] | Sardana, N., Shekoohi, S., Cornett, E. M., & Kaye, A. D. (2023). Qualitative and quantitative research methods. In Substance use and addiction research (pp. 65-69). Academic Press. |

[28]

.

Government intervention loans and MSMEs' performance were the intended subjects of the questionnaire. The system was designed to gather comprehensive and accurate information on the operations of company owners who have taken out loans from microfinance institutions and have also sought out government intervention loans.

There was a response rate of around 98% (or 988 out of 1000) to the survey of MSMEs in Southwestern Nigeria. The survey included comprehensive information from 988 of the 1000 questionnaires handed out. The parts that make up the instrument may be either closed or open-ended. Researchers may need to verify answers to closed-ended questions with other sources to utilise the data effectively, while open-ended questions elicit detailed information from respondents. Respondents' identifying information (age, marital status, occupation, number of employees, account transactions, etc.) is gathered by the instrument. The survey was sent out to everyone in a straight line, and they responded right away. This made sure that a lot of people responded to the analysis, and the results were presented.

3.2. Stochastic Frontier Analysis

This research makes use of SFA, which was first presented in empirical literature, to get our efficiency ratings. While taking random shocks into consideration, the SFA methodology seeks to estimate the unobservable inefficiency in a firm's production technology of the cost, revenue, profit, profit, production, and distance function, a fundamental tenet of neoclassical production theory

| [14] | Ghanad, A. (2023). An overview of quantitative research methods. International journal of multidisciplinary research and analysis, 6(08), 3794-3803. |

[14]

. The SFA technique differs from the non-parametric Data Envelope Analysis (DEA) and Free Disposal Hall approaches in that it uses a functional form to describe technical inefficiency and error terms separately. The empirical model is specified as:

(1)

Where:

Y is the output of firm ,

X is a k×1 vector of input variables (covariates),

is a vector of unknown parameters,

represents statistical noise (assumed to follow a normal distribution),

ui≥0 captures the technical inefficiency (assumed to follow a one-sided distribution, such as truncated-normal or half-normal).

In linear form, equation (

2) can be written as:

(2)

In this formulation:

The deterministic component is α0 + β′X𝑖,

The composite error term ε𝑖=− combines random noise and inefficiency .

An alternative way to express technical efficiency (TE) is by comparing the observed output with the output that would have been achieved had the firm operated on the frontier:

(5)

The possible values for technical efficiency (TE) ratings are -1 to 1. Inferentially, this compares bank i's cost efficiency to the lowest possible cost that a cost-efficient bank in the same industry might incur with the same input vector

| [18] | Kittur, J. (2023). Conducting quantitative research study: A step-by-step process. Journal of Engineering Education Transformations, 36(4), 100-112. |

[18]

. Because microfinance institutions in Nigeria are evaluated compared to the industry leader in terms of cost-efficiency, the efficiency ratings given to these institutions are subjective. Specifically, the stochastic frontier production function for the imbalanced panel is specified using the truncated normal random time-varying method

| [28] | Sardana, N., Shekoohi, S., Cornett, E. M., & Kaye, A. D. (2023). Qualitative and quantitative research methods. In Substance use and addiction research (pp. 65-69). Academic Press. |

[28]

. Here is the model's specification:

(6)

The given sentence describes the following: Ρίt is the logarithm of the total loans and advances of the i-th bank in the t-th time period of a scalar output; Xůt is a k×1 vector of the input quantities of the i-th firm in the t-th time period; β is a vector of unknown parameters; Vůt is noise; and uίt represents technical inefficiency.

As a result of running the likelihood ratio (LR) test to determine whether the specification was sufficient, the shortened time-varying specification was chosen. Additionally, there are two methods that are suggested in the banking literature for determining inputs and outputs. Banks accept deposits as part of the intermediation process, which involves the use of labour and capital to transform those deposits into loans. According to this production model, a bank is just like any other business: it uses labour and capital to make deposits and loans. The intermediation strategy is used in this study because it focuses on bank lending to the real sector.

SFA uses the subsequent efficiency score to rank the top-performing banks, from worst to best. The use of either parametric or non-parametric frontier analysis by microfinance sector banks may accomplish this arrangement. There are two types of approaches: parametric and non-parametric

| [18] | Kittur, J. (2023). Conducting quantitative research study: A step-by-step process. Journal of Engineering Education Transformations, 36(4), 100-112. |

[18]

. SFA, Tick Frontier, and DFA are examples of the former. A DEA and a free disposal hull are examples of the latter. Both of these complex approaches aim to compare and contrast how well different companies are doing, but they go about it in different ways according to the assumptions they make.

3.3. Panel Vector Autoregressive

A dynamic framework must be specified inside the model in order to account for the possibility that model variables are endogenous. Panel Vector Autoregressive (PVAR) using the Granger causality technique is thus used

| [14] | Ghanad, A. (2023). An overview of quantitative research methods. International journal of multidisciplinary research and analysis, 6(08), 3794-3803. |

[14]

. We have the following equations to describe a k-variate homogeneous PVAR of order p with panel-specific fixed effects

| [28] | Sardana, N., Shekoohi, S., Cornett, E. M., & Kaye, A. D. (2023). Qualitative and quantitative research methods. In Substance use and addiction research (pp. 65-69). Academic Press. |

[28]

.

(7)

The vector Y̯t has K= 3 variables and is defined as [∆EFF, ∆PSB, ∆LIQDL]. B0 is an invertible (nxn) matrix that contains the coefficient of the endogenous variable's contemporaneous relations; B1 are (nxn) matrix that represents the dynamic interaction between the K model variables; and t is a mean-zero (nxn) panel error term vector. P is the number of delays, and it is also called panel innovation or shocks.

(8)

Where:

= Change in Efficiency

Change in Public Sector Borrowing

Change in Liquidity-to-Deposit Ratio

Just like the autoregressive lag order polynomial, the model may also be expressed in a more compact form. It is common practice to normalise the panel error term's variance-covariance matrix so that.

Since the PVAR model cannot be seen, in order to estimate it, we must first get its reduced form representation. One way to do this is to express Yůt in terms of its delays. We pre-multiply the PVAR representation by B0−1 on both sides in order to get the reduced form representation. Therefore, we discover:

(10)

3.4. Data Collection and Source of Data

Using information gathered from 18 microfinance institutions in the state's southwestern region between 2018 and 2024, this research concludes. This research made use of both secondary and primary sources of information. Skilled personnel in the research area, which encompasses all six states in Nigeria's South-West region, administered questionnaires with the appropriate modifications to collect primary data. Microfinance bank entrepreneurs may find all the information they need in this questionnaire. Individual criteria included for estimation in this research include income, gender, credit rating, kind of work, association with Southwest State, and education. The survey also includes a lengthy series of questions about account ownership and usage. Secondary sources included the records of the small company owners studied and the archives of the microfinance institutions that were part of the survey. In addition, reports from the World Bank and publications from the CBN and the NBS were consulted for the statistics.

4. Results and Discussion

4.1. Unit Root Test

Regression analysis utilising non-stationary data has been found in the literature to provide erroneous results. Because of this, the stationary test must be performed. Our investigation used the Levin, Lin-Chu (LLC), Im, Pesaran’s and Shin (IPS), Augmented Dickey-Fuller- Fisher (ADF), and Philip Perron-Fisher (PP) unit root tests to comprehend the stationary form order of integration of our variables. The existence of a unit root is the null hypothesis that underlies each of these tests. When it comes to cross-sectional units, IPS, ADF, and PP assume that there is an imbalanced panel dataset and individual unit root processes, but LLC assumes that there is a balanced dataset and common unit root processes.

Table 1 shows that the model contains both the I(0) and I(1) variables, as determined by the tests. In terms of first differences, however, every single variable is stationary, even if they are all on the cusp of the integration orders I(0) and I(1). Through the use of LLC, IPS, ADF, and PP tests, it was shown that the majority of the data series may have the null hypothesis of a unit root's existence rejected at the 5% significance level.

Table 1. Unit root test.

Variables | Lag | LLC | R | IPS | R | ADF | R | PP | R |

CRISK | 1 | -2.46 | I(0) | -53.71 | I(0) | 99.92 | I(0) | 67.42 | I(0) |

PSB | 1 | -13.66 | I(0) | -5.13 | | 3.78 | | 53.02 | I(0) |

∆PSB | 1 | - | | -1.34 | I(1) | 52.78 | I(1) | - | |

EFF | 1 | -7.70 | I(0) | -1.47 | I(0) | 54.51 | I(0) | 57.86 | I(0) |

CAP | 1 | -2.99 | I(0) | -1.3E+e15 | I(0) | 47.49 | I(0) | 68.49 | I(0) |

LIQD | 1 | -3.29 | I(0) | -1.43 | I(0) | 69.68 | I(0) | 54.20 | I(0) |

ORG | 1 | -1.25 | I(0) | -1.1E+e14 | I(0) | 83.51 | I(0) | 69.60 | I(0) |

SIZE | 1 | -9176 | I(0) | -1.63 | I(0) | 86.73 | I(0) | 47.79 | I(0) |

Source: Author’s computation 2025

4.2. Lag Length Selection Criteria

The lag order selection statistics are also taken into account before the model estimate. Since the PVAR method responds to the number of delays used in its estimate, finding the optimal lag length is essential. Because it minimises the information criterion, the chosen lag length is lag 1 according to the results of the Bayesian information criterion (MBIC) and the Akaike information criterion (MQIC). Decisions are based on MBIC and MQIC criteria, even if MAIC criteria are lower when two lags are used in the research. The findings are shown in

Table 2. Following success with the over-identifying restriction test known as Hansen's J, the ideal lag time is determined by minimising the MBIC, MAIC, and MQIC information criterion

| [3] | Agaba, A. M., & Mugarura, E. (2023). Microfinance Institution Services and Performance of Small and Medium Enterprises in Kabale District Uganda. International Journal of Entrepreneurship and Business Management, 2(1), 1-18. |

[3]

.

Table 2. Lag length selection criteria.

Lag | J | J p-value | MBIC | MAIC | MQIC |

1 | 40.67 | 0.14 | -96.18 | -23.32 | -52.33 |

2 | 4.02 | 0.10 | -64.41 | -27.98 | -42.48 |

Source: Author’s computation 2025

4.3. Maximum Likelihood Estimate

We find that inefficiency is the main cause of the large divergence from the Cobb-Douglas function in this portion of the data. Inefficient use of capital, labour, and borrowed funds accounts for about 96% of the variance in loans and advances, as shown by gamma in

Table 3. The metric is insufficient to verify the stochastic frontier model's relevance, as

| [10] | Blanco, A. J., Irimia-Diéguez, A. I., & Vázquez-Cueto, M. J. (2023). Is there an optimal microcredit size to maximize the social and financial efficiencies of microfinance institutions?. Research in International Business and Finance, 65, 101980. |

[10]

pointed out. Restrictive and non-restrictive model estimates are highlighted by the likelihood ratio statistics, which they propose. Therefore, this number is close to 1. Technical inefficiency, rather than noise, is presumably accounting for many variants of the error term in the model relating to loans and advances to clients. Still, the noise impact from the combined error term accounts for 4% of the discrepancy between the two sets of data. The model's ability to accurately forecast technological inefficiency is supported by the statistical significance of the gamma findings, which align with previous research

| [27] | Roslan, S., Zainal, N., & Mahyideen, J. M. (2021). Impact of macroeconomic conditions on financial efficiency of microfinance institutions: evidence from pre and post-financial crisis. Journal of Technology Management and Technopreneurship (JTMT), 9(1), 32-47. |

[27]

. This finding demonstrates that microfinance institutions' performance is very sensitive to input variables like loans and advances, labour and capital costs, and the amount borrowed. According to

| [26] | Rajapakshe, W. (2021). The Role of Micro Finance Institutions on the Development of Micro Enterprises (MEs) in Sri Lanka. |

[26]

, choosing the right functional model form is crucial. The conducted likelihood ratio test met the assumption of the Cobb-Douglas function based on non-restrictive and restrictive modules, allowing us to investigate the functional form of the model. Instead of doing a translog to support the adoption of an alternative hypothesis, the Cobb-Douglas frontier was used for the model because the outcome reveals that the null hypothesis cannot be rejected. Unless one excludes the labour cost (pLAB), every single variable in the maximum likelihood estimate (pCAP, pBOR) is statistically significant at the 1% level. Furthermore, the coefficients may be thought of as elasticities due to the variables' implications in the natural logarithm form

| [22] | Muthoni, M. P., Mutuku, L., & Riro, G. K. (2017). Influence of loan characteristics on microcredit default in Kenya: A comparative analysis of microfinance institutions and financial intermediaries. |

[22]

.

As a result, the estimated elasticity of capital, labour, and the borrowed money for microfinance bank loans and advances to clients is 0.93, 0.10, and 0.52, respectively. In addition, except for the price of capital (pCAP), all of the explanatory factors have a negative connection with the dependent variable, loans and advances to consumers

| [25] | Primiana, I., Masyita, D., & Febrian, E. (2018). Comparative study οn sustainability of sharia microfinance institutions through financial and social efficiency. |

[25]

. Efficiency is defined as the creation of loans and advances with the lowest feasible staff cost, suggesting that banks pay less for labour as they generate more. To broaden their reach, however, banks may need more permanent assets, such as equipment. Therefore, it is possible to buy additional fixed assets via the extension of loans and advances

| [2] | Adebola, B. Y. (2021). Microfinance banks, small and medium scale enterprises and COVID-19 pandemic in Nigeria. European Journal of Economics, Law and Politics, 8(2), 1-10. |

[2]

. The bank will look for a less expensive way to raise capital to improve its bottom line as it increases the amount of loans and advances it provides for consumers.

Table 3. Maximum likelihood estimation.

Dependent | | | | |

| | Coefficient | Std. Error | Prob. Value |

Production | pLAB | -0.10 | 9.65 | 0.99 |

Frontier | pCAP | 0.93 | 0.03 | 0.00 |

pBOR | -0.52 | 0.16 | 0.01 |

CONSTANT | 2.20 | 0.47 | 0.00 |

Variance | Sigma_u | 14.78 | 13.37 | 0.27 |

Parameters | Sigma_v | 0.63 | 0.07 | 0.00 |

Lambda | 23.45 | 13.36 | 0.08 |

Gamma | 0.96 | | |

Unrestrictive LKH | -218.34 | | |

Restrictive LKH | -250.37 | | |

LKH Ratio | 64.09 | | |

Model | No of OBS | 144 | | |

Diagnostic | No of Groups | 18 | | |

Prob. Value | 0.000 | | |

Source: Author’s computation 2025

There will be fewer opportunities for banks to provide loans and advances as a result of the correlation between the rising cost of borrowing money and the corresponding increase in risk. Because of this, it is clear that low-quality human resources are a big issue for microfinance institutions, which is why the model's pLAB is so small. One of the possible justifications is insufficient capitalisation. This lines up with previous research

| [1] | Abdullah, W. M. Z. B. W., Zainudin, W. N. R. A. B., Ismail, S. B., & Zia-Ul-Haq, H. M. (2022). The impact of microfinance services on Malaysian B40 households’ socioeconomic performance: A moderated mediation analysis. International Journal of Sustainable Development and Planning, 17(6), 1983-1996. |

[1]

that found that consumers' access to loans and advances is negatively impacted by high capital and labour costs, in contrast to the positive effect on borrowed funds. It is anticipated that there would be a negative and statistically significant correlation between loans and debt. In a study conducted by

| [7] | Babajide, A. A., Lawal, A. I., Somoye, R. O. & Nwanji, T. I. (2018). The effect of fiscal and monetary policies interaction on stock market performance: Evidence from Nigeria. Future Business Journal, 4(1), 16-33. |

[7]

, it was found that the cost of borrowing funds decreases as more loans and advances are extended to customers. This is because an efficient microfinance institution will expand its outreach in a way that makes cheaper funds available to finance these loans and advances.

4.4. Technical Efficiency

Microfinance institutions in the Southwest achieved an average operational efficiency of 46.6% from 2018 to 2024. This means that microfinance institutions in the area were, on average, functioning at a level that was 53.4% lower than their full capacity. Microfinance institutions may be able to raise their loan and advance amounts to clients by 53.4% on average without increasing their use of borrowed funds, labour, or capital. The best-performing microfinance institution in the southwest was operating at 68%, which is around 32% below the border point, according to 144 observations (see

Table 4). It is for this reason that we must investigate the root of the inefficiency of microfinance institutions in the area and evaluate critically the majority of the supplementary initiatives included in the reform proposed by the Central Bank of Nigeria to address this issue.

4.5. Relationship Between Microfinance Bank Efficiency and Performance of Small Businesses

Using the PVAR method and the related granger causality approach, this study examines the link between microfinance bank (EFF) efficiency and small business (PSB) performance. This shift is based on the idea that efficiency metrics have an effect on a microfinance bank's performance year over year, as they are a long-term phenomenon. After determining that one lag is the optimal lag length and that the banks are cross-sectionally dependent, the researchers performed the first-order PVAR and Granger causality analyses.

Table 5 displays the outcomes. The PVAR's stability was verified once the eigenvalues fell inside the unit circle. According to

| [6] | Audu, I., Abubakar, A. M., & Baba, M. (2021). The Role of Microfinance Institutions’ Services on the Performance of Small and Medium Entreprises in Gombe State, Nigeria. Journal of Management Sciences, 4(1), 500-517. |

| [19] | Lwesya, F., & Mwakalobo, A. B. S. (2023). Frontiers in microfinance research for small and medium enterprises (SMEs) and microfinance institutions (MFIs): a bibliometric analysis. Future Business Journal, 9(1), 17. |

| [30] | Soldátková, N., & Černý, M. (2022). Microfinance in Sub-Saharan Africa: social efficiency, financial efficiency and institutional factors. Central European Journal of Operations Research, 30(2), 449-477. |

[6, 19, 30]

, this proves that our variables remain constant across time.

Table 4. Technical efficiency score.

| Efficiency Score |

Obs. | 144 |

Mean | 0.47 |

SD | 0.13 |

Min | 0.28 |

Max | 0.69 |

Source: Author’s computation

Table 5. Panel Vector autoregreesive (PVAR) Model Results.

Variable | | EFF | PSB | LIQD |

PSB | L1 | 0.14 | 0.98 | 0.02 |

-0.18 | -0.12 | 0.05 |

EFF | L1 | 0.56 | -0.08 | 0.04 |

(0.11) | (0.07) | (0.03) |

LIQD | L1 | -0.85 | -1.01 | 0.97 |

(0.36) | (0.39) | (0.18) |

Source: Author’s computation 2025

The above shows that the lag of EFF, PSB, and LIQD are significant at 1% according to the findings of the PVAR. On the other hand, the EFF line of equation for microfinance banks does not include the PSB, but the LIQD is considerable at 1%. The PSB has a negligible effect on the microfinance bank’s efficiency, according to this. This theory has some merit, as inefficient businesses are not likely to repay their loans or maintain their savings accounts with microfinance institutions

| [17] | Ikechukwu & Elizabeth (2019). Formal credits access and farmers welfare in Plateau State, Nigeria. International Journal of Mechanical Engineering and Technology (IJMET), 10(2), 302-313. |

[17]

. Microfinance institutions will see a decline in efficiency as a result of decreasing profitability and a rise in non-performing loans. However, when looking at the small business (PSB) line of the equation, it is evident that the LIQD is considerable at 1%, but the EFF of the microfinance bank is also not significant on the PSB

| [31] | Yahaya, A. A., & Kolawole, K. D. (2022). Impact of Microfinance Banks’ Facilities on Performance of Small and Medium Scale Enterprises in Nigeria. Lapai International Journal of Management and Social Sciences, 14(2), 34-43. |

[31]

.

Among other things, this might be justified by the fact that the majority of the loans that have been approved do not meet the necessary standards with regard to their duration, nature, price, sufficiency, and funding distribution among different sectors. Thus, it is anticipated that the efficiency level of MFBs, which are currently in a growing stage, will improve as a result of the regulatory authority’s progressive policies

| [9] | Bharti, N., & Malik, S. (2022). Financial inclusion and the performance of microfinance institutions: does social performance affect the efficiency of microfinance institutions?. Social Responsibility Journal, 18(4), 858-874. |

[9]

. This, in turn, will lead to a more positive impact of microfinance bank efficiency on small business performance.

Table 6. Stability Check.

Real | Imaginary | Modulus |

0.93 | -0.18 | 0.95 |

0.93 | 0.18 | 0.95 |

0.68 | 0 | 0.68 |

Source: Author’s computation 2025

There is evidence that liquidity (LIQD) influences microfinance bank efficiency and small company performance in a favourable and statistically significant way. Microfinance banks are better able to lend money to MSMEs and improve their performance is consistent with the a priori anticipation that liquidity plays a significant role in this process. According to

| [16] | Hermes, N., Lensink, R., & Meesters, A. (2018). Financial development and the efficiency of microfinance institutions. In Research Handbook on Small Business Social Responsibility (pp. 177-205). Edward Elgar Publishing. |

| [19] | Lwesya, F., & Mwakalobo, A. B. S. (2023). Frontiers in microfinance research for small and medium enterprises (SMEs) and microfinance institutions (MFIs): a bibliometric analysis. Future Business Journal, 9(1), 17. |

[16, 19]

, bank liquidity is a key factor in microfinance institutions' effectiveness, which may explain why the Nigerian government has been working to loosen regulations and implement reforms that would increase bank liquidity. More liquid banks are less likely to collapse if their liquidity ratio is high

| [12] | Deb, J., & Sinha, R. P. (2022). Impact of competition on efficiency of microfinance institutions: Cross country comparison of India and Bangladesh. International Journal of Rural Management, 18(2), 250-270. |

[12]

. The model's stability is confirmed by the results in

Table 6.

4.6. Granger Causality Test Results

The research employs the Granger causality test, which is based on the Wald test. There is no causal relationship, according to the null hypothesis. All the building pieces of exogeneity analysis (ALL) also point to endogeneity.

Table 7 displays the findings of the Granger Causality Test, which show that the current level of small business performance (PSB) is not explained by the historical efficiency of microfinance banks (EFF)

| [16] | Hermes, N., Lensink, R., & Meesters, A. (2018). Financial development and the efficiency of microfinance institutions. In Research Handbook on Small Business Social Responsibility (pp. 177-205). Edward Elgar Publishing. |

[16]

. It seems that the results do not prove a causal link between PSB and EFF, either up or down the causal chain. Inferentially, the current level of EFF cannot be explained by previous PSB. Similarly, bivariate causality demonstrates that PSB is not granger-caused by the concurrent histories of EFF and LIQD. However, the results show a one-way causal link between PSB and LIQD; in other words, PSB Granger causes LIQD. Similarly, according to bivariate causality, neither the PSB nor the LIQD past nor present granger causes EFF, but EFF granger causes LIQD

| [3] | Agaba, A. M., & Mugarura, E. (2023). Microfinance Institution Services and Performance of Small and Medium Enterprises in Kabale District Uganda. International Journal of Entrepreneurship and Business Management, 2(1), 1-18. |

[3]

. It was confirmed by the results that LIQD and EFF are causally related in just one way. In terms of the direction of causality report, it is evident that there is no causal relationship between the efficiency of microfinance banks and the performance of small businesses. Instead, we found a unidirectional causality running from liquidity to the performance of small businesses.

| [18] | Kittur, J. (2023). Conducting quantitative research study: A step-by-step process. Journal of Engineering Education Transformations, 36(4), 100-112. |

[18]

found the same thing in their research of Morocco.

Table 7. Granger causality test.

Negative Effect of: | PSB | EFF | LIQD |

PSB | - | 1.180 | 6.61 |

EFF | 0.61 | - | 5.45 |

LIQD | 0.10 | 2.39 | - |

ALL | 0.76 | 2.46 | 11.90 |

Source: Author’s computation 2025

A study explains the results in Nigeria by saying that microfinance institutions aren't very good at what they do, so they give out loans to MSMEs that aren't suitable for them in terms of affordability, terms of repayment, and other factors. As a result, the SMEs don't get the money they need to grow, which hurts their relationship with the SMEs and their ability to get better loans in the future. On the other hand, it has been shown that liquidity is directly related to microfinance banks' efficiency, which in turn affects their capacity to provide credit and, therefore, makes capital accessible for the expansion of MSMEs. So, to increase microfinance institutions' liquidity, the government should do a better job of making more intervention funds accessible to them via wholesale financing.

| [19] | Lwesya, F., & Mwakalobo, A. B. S. (2023). Frontiers in microfinance research for small and medium enterprises (SMEs) and microfinance institutions (MFIs): a bibliometric analysis. Future Business Journal, 9(1), 17. |

| [27] | Roslan, S., Zainal, N., & Mahyideen, J. M. (2021). Impact of macroeconomic conditions on financial efficiency of microfinance institutions: evidence from pre and post-financial crisis. Journal of Technology Management and Technopreneurship (JTMT), 9(1), 32-47. |

| [30] | Soldátková, N., & Černý, M. (2022). Microfinance in Sub-Saharan Africa: social efficiency, financial efficiency and institutional factors. Central European Journal of Operations Research, 30(2), 449-477. |

[19, 27, 30]

examined the impact of microfinance on the expansion of small businesses in Nigeria, and his results are consistent with ours. The current size is insufficient to accomplish the suggested improvement in MSMEs' performance that may result from an increase in microloans. While this aligns with the goals of MSMEs, their current size prevents them from accomplishing them. Microfinance is a great way to boost growth, according to

| [13] | Ekpo, V., & Ebewo, P. E. (2024). The Influence of Microfinance Institutions on Nigerian Small, Micro, and Medium Enterprises. IJEBD (International Journal of Entrepreneurship and Business Development), 7(2), 209-214. |

[13]

, but the government needs to do more with its money power to make it a powerful tool for empowering vulnerable micro-entrepreneurs. While MFBs are still in their early stages, prior research, especially at the global level involving many microfinance institutions