7. Contemporary Theories of Motivational Budgeting

This section discusses innovative budgeting theories herein described as contemporary theories of motivational budgeting (

See Table 2).7.1. Needs Ladder Affirmative Theory (Usen Umo, 2024)

Needs Ladder Affirmative Theory is built on the premises set out below:

1) People have quite wide variety of needs which can be arranged in a ladder of rungs.

2) People are motivated to satisfy the lower order needs, at least in reasonable part before they strive to satisfy the higher order needs.

3) People act to fulfill the needs that are yet to be satisfied

4) Although people tend to act in a way to satisfy more of the lower order needs, budget makers must consider the higher order needs of organizational members during the budget formation process.

Needs Ladder Affirmative Theory is the outgrowth of the works of Abraham Maslow in the later part of the twentieth century (20

th century) and the research pack developed by Usen Paul Umo in the first quarter of the twenty-first century (21

st century). Abraham Maslow was the proponent of Needs Hierarchy Theory. In his psychological literature (1970) titled “Motivation and Personality’’, Maslow published a theory of motivation in which he proposed that peoples’ behaviour is determined by a wide variety of needs

| [5] | Bittle, LR Business in Action, New York, McGraw Hill Book Company Inc., 2019. |

| [6] | Britt, TW & Jex, SM Organizational Psychology, Hoboke: New Jersey, John Wiley and Sons Limited, 2017. |

[5, 6]

.

Usen Paul Umo elaborated on Maslow’s work and in the first quarter of the twenty-first century, published some empirical works on motivation and the human side of the enterprise

| [20] | Umo, UP, Contemporary Theories of Motivational Budgeting. International Journal of Advanced Multidisciplinary Research and Studies, 2025. https/doi.org/10.62225/2583049x.2025.5.2.4180 |

| [31] | Umo, UP, The Management Accountant in Budgetary Process, Employees’ Motivation and Productivity: The Nigerian Case, Research Journal of Finance and Accounting, Hong Kong, 2014, 5(24): 178-184. |

| [32] | Umo, UP, Impact of Employees’ Behaviour on Budgetary Performance of Manufacturing Companies: A Study of Selected Quoted Firms in Nigeria, Ph. D. Dissertation, University of Port Harcourt Library, Port Harcourt, 2015. |

| [36] | Umo, UP, Essays in Human Side of the Enterprise: Management Systems, Financial Planning and Employees’ Reactions in a Developing Economy of the 21st Century, European Journal of Business and Management Research, London, 2022, 7(3): 1-12. |

[20, 31, 32, 36]

.

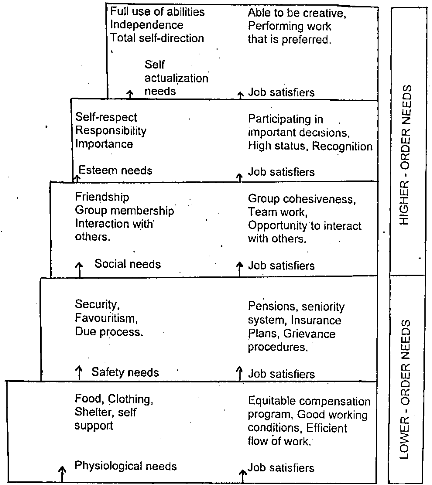

The works of Abraham Maslow as further developed by Usen Umo are condensed into this budgetary science theory called “Needs Ladder Affirmative Theory”. Needs Ladder Affirmative Theory does not see budgeting as a mere technique; it projects budgeting as an innovative and motivational technique for dealing with employees’ problems associated with physiological, safety, social, esteem and self-actualization needs in organizations. It is a theory that presents motivational budgeting as a process that brings human needs into “an orderly arrangement of power to motivate behaviour in the human side of the enterprise” called Ladder of Human Needs and Job Satisfiers in Business Organizations.

From

Figure 1 above, the following are discernible:

Rung 1 Physiological Needs

Physiological needs include the needs for food, shelter, clothing and other basic requirements of life.

Rung 2 Safety Needs

Safety needs are the needs for security or protection against threat and deprivation.

Rung 3 Social Needs

These include the needs for friendship, affection, belonging and love.

Rung 4 Esteem Needs

Esteem needs can also be described as ego needs and include the needs for self-respect, responsibility, recognition and achievement.

Rung 5 Self-actualization Needs

Self-actualization needs include the needs for realizing one’s full potential, that is, everything one is capable of becoming.

| [5] | Bittle, LR Business in Action, New York, McGraw Hill Book Company Inc., 2019. |

| [6] | Britt, TW & Jex, SM Organizational Psychology, Hoboke: New Jersey, John Wiley and Sons Limited, 2017. |

| [7] | Cascio, WF Managing Human Resources, New York, McGraw Hill Book Company, 2019. |

| [8] | Caplan, N; Doseh, P & Jekam, S Business Today, Enugu, New Era Publishers, 2018. |

| [20] | Umo, UP, Contemporary Theories of Motivational Budgeting. International Journal of Advanced Multidisciplinary Research and Studies, 2025. https/doi.org/10.62225/2583049x.2025.5.2.4180 |

| [39] | Umo, UP, Contextual Anatomy of the Human Side of the Enterprise: Management Systems, Financial Planning and Employees’ Reactions, Business Management and Economics - Research Progress Vol. I, United Kingdom, B P International, 2024. |

[5-8, 20, 39]

.

The ladder of human needs and job satisfiers (

Figure 1 above) presents two categories of needs called lower order needs and higher order needs. Each member of an organization is assumed to have needs in each category. Examples of job satisfiers that can fulfill the needs are also indicated in the figure. The Needs Ladder Affirmative Theory portrays a human being as a perpetually wanting animal. Accordingly, when needs on the lower order have been satisfied, at least in part, a person begins to strive for the next rung in the ladder

.

The starting point for understanding motivational budgeting relative to Needs Ladder Affirmative Theory is physiological needs. An employee who is hungry, tired or poorly paid is thinking of the basic needs of life (food, shelter, clothing, and sleep as applicable) and not work. But once physiological needs are fulfilled, they lose their power to motivate. Then safety needs become important. For example, enterprise workers become concerned about keeping their jobs and about being financially secured when they retire. People are motivated to satisfy the lower order needs before they strive to satisfy the higher order needs. But once a need is satisfied, it is no longer a powerful motivator. For example, labour unions negotiate for higher wages, benefits, safety standards and job security. These bargaining issues relate directly to the satisfaction of lower order needs. Once the physiological and safety needs are reasonably satisfied, the higher order needs (social, esteem, self-actualization) become dominant needs

.

Employees want to belong and to interact with other employees. Thus, friendly behaviour of individuals in small groups within the organization is a major source of satisfaction for social needs. In a small group, individuals support and encourage one another; as a by- product, they get a sense of being accepted members of the group. Needs Ladder Affirmative Theory vis-a-vis motivational budgeting (real participation in budget formation) is found very useful in this direction. Once social needs have been largely satisfied, they also begin to lose their power to motivate. Consequently, the need for other higher-level needs arise.

The esteem needs are needs for self-respect and respect from others. An important part of this area is that an employee’s work efforts and output be recognized and appreciated by others. When the need for esteem is strong, individuals (that is budget makers) will often set difficult budget goals, work hard to achieve the goals and expect to receive recognition for these efforts. Budget goals accomplishment and the resulting recognition lead to the feelings of self-esteem and self-confidence

| [31] | Umo, UP, The Management Accountant in Budgetary Process, Employees’ Motivation and Productivity: The Nigerian Case, Research Journal of Finance and Accounting, Hong Kong, 2014, 5(24): 178-184. |

| [39] | Umo, UP, Contextual Anatomy of the Human Side of the Enterprise: Management Systems, Financial Planning and Employees’ Reactions, Business Management and Economics - Research Progress Vol. I, United Kingdom, B P International, 2024. |

[31, 39]

.

At the top of the ladder of human needs and job satisfiers is self-actualization. Self-actualization implies the ability to display and use one’s full potential. This need takes over when an adequate level of satisfaction has been reached in the other four lower rungs of needs. An organizational member who reaches self-actualization has come close to using his full set of skills. In budgetary science, self-actualizing individuals display certain characteristics during budget formation and control processes, viz:

1) They tend to be serious and thoughtful.

2) They focus on problems outside themselves.

3) Their behaviour is unaffected and natural.

4) They are strongly ethical.

Because employees work to satisfy the more basic needs, budget makers (decision makers) often overlook employees’ self-actualization need. Reaching a level of complete self-actualization rarely occurs in budgetary science. Certainly, it is hard to achieve if other needs are not adequately satisfied. But an organization participant (member of an organization) is capable of partially satisfying the self-actualization need.

In organizations, members differ in the intensity of their needs. For instance, some employees have an intense security need that will dominate their behaviour no matter what the managers do. Other members of the organization are more strongly influenced by esteem needs. Budget makers (managers) have no stand program to follow when attempting to promote a high level of motivation. Differences in personal background, experience and education are powerful; the conditions that work for one individual may not work for another in an organizational setting. The ladder of human needs and job satisfiers in organizations is a convenient way to classify human needs but it should not be viewed as a rigid one-step-at-a-time procedure. Each rung of needs does not have to be completely satisfied (if that is possible) before an individual can be motivated by a higher need.

The needs ladder affirmative theory offers four important contributions, viz:

1) It identifies important categories of needs.

2) It is important to think of two general order of needs in which the lower order needs must be satisfied, at least in part, before the higher order needs become important to individuals.

3) It sensitizes budget makers (managers) to the importance of personal growth and self-actualization.

4) It emphasizes the task set before the budget makers in trying to satisfy the higher order needs through job enlargement and real participation of all levels of the organization during the budgeting process

.

7.2. Theory Alpha and Theory Beta (Usen Umo, 2024)

Theory Alpha and Theory Beta can be jointly described as twin theories of motivational budgeting. These theories evolve from the concerted works of Douglas McGregor on the human side of the enterprise (1960) and the related research album of Usen Paul Umo in the first quarter of the twenty first (21st) century. Douglas McGregor brought his work under the framework of two theories of management which he described as Theory X and Theory Y

| [5] | Bittle, LR Business in Action, New York, McGraw Hill Book Company Inc., 2019. |

[5]

. Usen Umo elaborated on the works of Douglas McGregor and in the first quarter of the twenty first centaury published related research albums on the human side of the enterprise

| [31] | Umo, UP, The Management Accountant in Budgetary Process, Employees’ Motivation and Productivity: The Nigerian Case, Research Journal of Finance and Accounting, Hong Kong, 2014, 5(24): 178-184. |

| [32] | Umo, UP, Impact of Employees’ Behaviour on Budgetary Performance of Manufacturing Companies: A Study of Selected Quoted Firms in Nigeria, Ph. D. Dissertation, University of Port Harcourt Library, Port Harcourt, 2015. |

| [34] | Umo, UP, Impact of Budgetary Process on Morale, Motivation and Productivity of Employees, MBA Thesis, Uyo, University of Uyo Library, 1999. |

| [35] | Umo, UP, Budgetary Systems in Organizations: An Anatomy of Management Views, Employees’ Behaviour and Productivity Trend of 21st Century Firms in a Tropical Nation, International Journal of Financial Research, Ontario, Canada, 2021, 12(4): 304-314. |

| [36] | Umo, UP, Essays in Human Side of the Enterprise: Management Systems, Financial Planning and Employees’ Reactions in a Developing Economy of the 21st Century, European Journal of Business and Management Research, London, 2022, 7(3): 1-12. |

| [37] | Umo, UP, Goal Internalization: An Innovative Management Strategy for Budgetary Performance in 21st Century Firms of Developing Economics, European Journal of Business and Management Research, London, 2022, 7(3): 1-6. |

| [38] | Umo UP, The Management Accountant in Budgetary Process, Values Inclination, Employees’ Motivation and Productivity: A Tropical Nation in Contextual View, Current Topics on Business, Economics and Finance, United Kingdom, B P International, 2023, (4): 99-122. |

| [39] | Umo, UP, Contextual Anatomy of the Human Side of the Enterprise: Management Systems, Financial Planning and Employees’ Reactions, Business Management and Economics - Research Progress Vol. I, United Kingdom, B P International, 2024. |

[31, 32, 34-39]

. He espoused the motivational function of budgeting and condensed his empirical submissions into the twin theories of motivational budgeting known as Theory Alpha and Theory Beta. Usen Umo affirms the following:

Traditional theories of motivation focus almost exclusively on the lower order needs and the organizational participants (employees) are expected to satisfy their higher order needs away from work. During the classical era, management focused almost exclusively on the lower order needs. People (organizational members) were expected to satisfy their higher order needs away from work. No wonder, from his empirical literature, Usen submitted inter alia:

1) Managers of firms complained that they paid their workers well and provided good job security but suffered poor productivity.

2) Managers of organizations must help their subordinates and employees to achieve their personal goals in order to motivate them to work towards the achievement of budget goals set in organizations.

3) The neoclassical (modern) theories of motivation recognize diversity of human needs and therefore focus on both the lower order needs and higher order needs emphasizing that satisfied needs cannot serve as motivators.

4)

Poorly paid workers may be inclined to work harder for more money than well paid ones. Labour unions become more concerned with job security (a safety need) once their members are receiving reasonable wages | [20] | Umo, UP, Contemporary Theories of Motivational Budgeting. International Journal of Advanced Multidisciplinary Research and Studies, 2025. https/doi.org/10.62225/2583049x.2025.5.2.4180 |

| [31] | Umo, UP, The Management Accountant in Budgetary Process, Employees’ Motivation and Productivity: The Nigerian Case, Research Journal of Finance and Accounting, Hong Kong, 2014, 5(24): 178-184. |

| [32] | Umo, UP, Impact of Employees’ Behaviour on Budgetary Performance of Manufacturing Companies: A Study of Selected Quoted Firms in Nigeria, Ph. D. Dissertation, University of Port Harcourt Library, Port Harcourt, 2015. |

| [34] | Umo, UP, Impact of Budgetary Process on Morale, Motivation and Productivity of Employees, MBA Thesis, Uyo, University of Uyo Library, 1999. |

| [35] | Umo, UP, Budgetary Systems in Organizations: An Anatomy of Management Views, Employees’ Behaviour and Productivity Trend of 21st Century Firms in a Tropical Nation, International Journal of Financial Research, Ontario, Canada, 2021, 12(4): 304-314. |

| [36] | Umo, UP, Essays in Human Side of the Enterprise: Management Systems, Financial Planning and Employees’ Reactions in a Developing Economy of the 21st Century, European Journal of Business and Management Research, London, 2022, 7(3): 1-12. |

| [37] | Umo, UP, Goal Internalization: An Innovative Management Strategy for Budgetary Performance in 21st Century Firms of Developing Economics, European Journal of Business and Management Research, London, 2022, 7(3): 1-6. |

| [38] | Umo UP, The Management Accountant in Budgetary Process, Values Inclination, Employees’ Motivation and Productivity: A Tropical Nation in Contextual View, Current Topics on Business, Economics and Finance, United Kingdom, B P International, 2023, (4): 99-122. |

| [39] | Umo, UP, Contextual Anatomy of the Human Side of the Enterprise: Management Systems, Financial Planning and Employees’ Reactions, Business Management and Economics - Research Progress Vol. I, United Kingdom, B P International, 2024. |

Once people have acquired a high degree of job safety and a reasonable salary, they look to other things. They become more concerned about social and personal needs (the respect of their peers, their self-esteem) which constitute the needs that cannot be satisfied on the job with money. Accordingly, top management must help their subordinates and employees to achieve their personal goals in order to motivate them to act in the firm’s best interest. Motivational budgeting is useful in this direction. In budgetary science, a close look at management views and employees’ reactions have created the typology of twin theories presented in a framework of Theory Alpha and Theory Beta. The assumptions of these two theories represent the views held by budget makers on what motivates employees during the budget formation process in organizations. More also, these assumptions correspond to the views held by budget makers (decision makers) that embrace either autocratic budgeting or participatory budgeting.

7.2.1. Theory Alpha

Theory alpha can also be called authoritarianism theory of motivational budgeting. This theory is rooted on the following precepts:

1) An average human being has an inherent dislike for work and will avoid it if possible.

2) Dislike for work requires that people must be coerced, controlled, directed and threatened with punishment in order to get them to work towards organizational goals set in the budget.

3) People work principally for money and do not derive any intrinsic satisfaction from work.

4) People generally prefer to be directed, attempt to avoid responsibilities, have relatively little ambition and desire security above all.

5) Two important jobs of managers are to control works through close supervision and to find more efficient ways for employees to accomplish their tasks (especially through making their works simpler).

6) The role of the accounting/finance department in an organization is to develop the budget and also provide information that helps management to control their subordinates by highlighting inadequate performance.

The six precepts highlighted above constitute the bases of authoritarianism in budgetary science and portray the human as a being of very limited dimensions, very nearly like a beast of burden. The implications for management were articulated by the scientific management school that flourished in the early part of the twentieth century pioneered by Winslow Taylor (the father of scientific management of jobs), Adam smith (the classical economist) and their contemporaries

| [20] | Umo, UP, Contemporary Theories of Motivational Budgeting. International Journal of Advanced Multidisciplinary Research and Studies, 2025. https/doi.org/10.62225/2583049x.2025.5.2.4180 |

| [21] | Lounderback, JG, & Hirsch, ML. Cost Accounting: Accumulation, Analysis and Use, Homewood, Richard D. Irwin Inc., 2016. |

| [34] | Umo, UP, Impact of Budgetary Process on Morale, Motivation and Productivity of Employees, MBA Thesis, Uyo, University of Uyo Library, 1999. |

| [35] | Umo, UP, Budgetary Systems in Organizations: An Anatomy of Management Views, Employees’ Behaviour and Productivity Trend of 21st Century Firms in a Tropical Nation, International Journal of Financial Research, Ontario, Canada, 2021, 12(4): 304-314. |

| [36] | Umo, UP, Essays in Human Side of the Enterprise: Management Systems, Financial Planning and Employees’ Reactions in a Developing Economy of the 21st Century, European Journal of Business and Management Research, London, 2022, 7(3): 1-12. |

| [37] | Umo, UP, Goal Internalization: An Innovative Management Strategy for Budgetary Performance in 21st Century Firms of Developing Economics, European Journal of Business and Management Research, London, 2022, 7(3): 1-6. |

| [38] | Umo UP, The Management Accountant in Budgetary Process, Values Inclination, Employees’ Motivation and Productivity: A Tropical Nation in Contextual View, Current Topics on Business, Economics and Finance, United Kingdom, B P International, 2023, (4): 99-122. |

| [39] | Umo, UP, Contextual Anatomy of the Human Side of the Enterprise: Management Systems, Financial Planning and Employees’ Reactions, Business Management and Economics - Research Progress Vol. I, United Kingdom, B P International, 2024. |

[20, 21, 34-39].

Theory Alpha is synonymous with downward flow (authoritative top-down) approach to budget formation in organizations. Authoritative top-down approach to budget formation is autocratic budgeting. Firms that imbibe Theory Alpha can be likened to organizations that prepare budgets without the full participation of operating personnels. Such organizations prepare their budgets in such a manner that allows monetary rewards for those who meet the budget requirements and punishment for those who do not. Thus, in these organizations budgets are imposed and not self-imposed

| [13] | Garrison, RH; Noreen, EW & Brewer, PC, Managerial Accounting, New York, McGraw Hill Book Company, 2021. |

| [16] | Horngren, CT & Foster, E. Cost Accounting: A Managerial Emphasis, New Delhi, Prentice Hall Inc., 2022. |

| [38] | Umo UP, The Management Accountant in Budgetary Process, Values Inclination, Employees’ Motivation and Productivity: A Tropical Nation in Contextual View, Current Topics on Business, Economics and Finance, United Kingdom, B P International, 2023, (4): 99-122. |

| [39] | Umo, UP, Contextual Anatomy of the Human Side of the Enterprise: Management Systems, Financial Planning and Employees’ Reactions, Business Management and Economics - Research Progress Vol. I, United Kingdom, B P International, 2024. |

[13, 16, 38, 39]

.

In organizations where Theory Alpha is upheld, the managers attempt to structure, control and closely supervise their subordinates and employees with a strong emphasis on the implementation of the budget at whatever cost. Thus, budget makers in these organizations believe that their main duty is to set the budget goals for the subordinates. This is a unilateral approach anchored on the traditional behavioral assumptions and the tenets of the crude authoritarian management during the classical era

| [9] | Drucker, P Management: Tasks, Responsibilities and Practices, New York, Harper and Row, 2018. |

| [20] | Umo, UP, Contemporary Theories of Motivational Budgeting. International Journal of Advanced Multidisciplinary Research and Studies, 2025. https/doi.org/10.62225/2583049x.2025.5.2.4180 |

| [36] | Umo, UP, Essays in Human Side of the Enterprise: Management Systems, Financial Planning and Employees’ Reactions in a Developing Economy of the 21st Century, European Journal of Business and Management Research, London, 2022, 7(3): 1-12. |

[9, 20, 36]

. In budgetary science and organizational behaviour, the determinants of theory Alpha are outlined below:

1) Imposed Budgets

Organization that embrace Theory Alpha operate imposed budgets. Imposed budgets are budgets forced on subordinate managers from above. Such budgets lack the full participation of operating personnels during the formation process. The different motivational results on employees’ behavior in organizations that uphold Theory Alpha have been highlighted. One result emphasizes alienation. Alienation arises when an employee feels that the management is thinking very low of him. Such employee looks frustrated and regresses. Work morale and motivation are adversely affected and productivity falls. Another motivational result on employees’ behavior in organization that imposes budgets from above is disillusion. Imposed budgets destroy employees’ belief in enterprise management. Employees in such firms do not accept the budget as theirs; they usually say that the budget is management’s, and the job belongs to management too. Goal congruence and goal internalization will suffer in organization that imbibe Theory Alpha because budget is not accepted but imposed

| [12] | Garrison, RH Management Accounting, Boston, Richard D. Irwin Inc., 2020. |

| [13] | Garrison, RH; Noreen, EW & Brewer, PC, Managerial Accounting, New York, McGraw Hill Book Company, 2021. |

| [16] | Horngren, CT & Foster, E. Cost Accounting: A Managerial Emphasis, New Delhi, Prentice Hall Inc., 2022. |

| [31] | Umo, UP, The Management Accountant in Budgetary Process, Employees’ Motivation and Productivity: The Nigerian Case, Research Journal of Finance and Accounting, Hong Kong, 2014, 5(24): 178-184. |

[12, 13, 16, 31]

.

2) Discriminatory and Unfair Devices

In organizations that embrace Theory Alpha, budgets are viewed as discriminatory and unfair devices. The implication is that employees’ morale will suffer. Furthermore, if already disgruntled employees learn that they are striving to attain sham budget goals, the effectiveness of future budgets, real or phony, might be seriously impaired

| [12] | Garrison, RH Management Accounting, Boston, Richard D. Irwin Inc., 2020. |

| [13] | Garrison, RH; Noreen, EW & Brewer, PC, Managerial Accounting, New York, McGraw Hill Book Company, 2021. |

| [36] | Umo, UP, Essays in Human Side of the Enterprise: Management Systems, Financial Planning and Employees’ Reactions in a Developing Economy of the 21st Century, European Journal of Business and Management Research, London, 2022, 7(3): 1-12. |

| [39] | Umo, UP, Contextual Anatomy of the Human Side of the Enterprise: Management Systems, Financial Planning and Employees’ Reactions, Business Management and Economics - Research Progress Vol. I, United Kingdom, B P International, 2024. |

[12, 13, 36, 39]

.

3) Pressure Device

Another popular assumption amongst budget makers in organizations that imbibe Theory Alpha is that budget should be used as a club. A club is a pressure device designed by the management and forced on employees to increase efficiency of performance (Umo, 2022). The belief is that employees are inherently lazy; they must be needled a bit and by increasing pressures, productivity will improve. This creates more problems when the subordinates and employees themselves understand and learn about the management’s assumptions. The implication is that, if a budget is used as a pressure device, it will probably generate resentment and ill-will rather than cooperation and increased productivity

| [24] | Pandey, IM, Financial Management, New Delhi, Vikas Publishing House PVT Limited, 2021. |

| [32] | Umo, UP, Impact of Employees’ Behaviour on Budgetary Performance of Manufacturing Companies: A Study of Selected Quoted Firms in Nigeria, Ph. D. Dissertation, University of Port Harcourt Library, Port Harcourt, 2015. |

| [38] | Umo UP, The Management Accountant in Budgetary Process, Values Inclination, Employees’ Motivation and Productivity: A Tropical Nation in Contextual View, Current Topics on Business, Economics and Finance, United Kingdom, B P International, 2023, (4): 99-122. |

[24, 32, 38]

.

The more pressure a budget brings, the less the productivity. That is, there exists inverse relationship between the pressure from budget and the productivity of organizational members directly affected by the budget. This is because the repressive nature of the budget makes the employee believe that the budget maker (decision maker) is thinking very low of him. He (the employee) therefore becomes frustrated and regresses. The writer states inter alia:

Instead of increased productivity, the pressure from budget brings informal group formation whose aim is to challenge the organization and its leadership.

Anthony Hopwood (2020) in his empirical work on “The Role of Accounting Data in Performance Evaluation” as further espoused by Umo (2024) affirmed that the pressure from budget brings increase in tension, resentment and fear amongst enterprise members. This result is not even limited to the lower class of employees but also found in the middle and lower level management of organization. Amongst the lower level management, pressure from budget might not result in unionization (formation of groups), it might create conditions negative to motivation and realization of set goals contained in the company’s budget. This is because every member of the lower level management becomes concerned only with the productivity of his own department in his bid to meet the budget requirements. This results in frequent interdepartmental strifes, quarrel with finance staff and a change of personality for the supervisors due to internal pressure

| [15] | Hopwood, AG. Accounting System and Managerial Behaviour, New Jersey, Prentice Hall Inc, 2020. |

| [39] | Umo, UP, Contextual Anatomy of the Human Side of the Enterprise: Management Systems, Financial Planning and Employees’ Reactions, Business Management and Economics - Research Progress Vol. I, United Kingdom, B P International, 2024. |

[15, 39]

.

4) Interdepartmental Anxiety

Another motivational result on organizational behaviour in firms that embrace Theory Alpha is interdepartmental anxiety. Anxiety arises when the budget is unilaterally prepared by a department, which creates the feeling that there is inequitable distribution of resources. This is a feeling prevalent in an organization where the budgeting process is relatively close and secret. This affects the motivation of subordinates as well as the middle level managers. It affects adversely the goal coordination between departments. A department whose allocation is cut will not try to work well with that whose allocation is approved or raised. This is because budget formation process is secret and unilateral. The affected department is unable to identify the grounds on which its budget is cut and that of the other approved or raised. This affects motivation adversely. These situations will create a lot of adverse effects on budget goal realization. Departmental conflicts will increase and managers will tend to withhold useful information from peers. The managers will also be overstating their annual estimates

| [20] | Umo, UP, Contemporary Theories of Motivational Budgeting. International Journal of Advanced Multidisciplinary Research and Studies, 2025. https/doi.org/10.62225/2583049x.2025.5.2.4180 |

| [30] | Ulrich, E. Human Resources Champions, Journal of Organizational Behaviour, Rotterdam, The Netherlands, 2016, 29(12): 201-213. |

| [35] | Umo, UP, Budgetary Systems in Organizations: An Anatomy of Management Views, Employees’ Behaviour and Productivity Trend of 21st Century Firms in a Tropical Nation, International Journal of Financial Research, Ontario, Canada, 2021, 12(4): 304-314. |

[20, 30, 35]

.

Generally, organizations that embrace Theory Alpha are identified with reduced work morale and decreased motivation. Since budget formation process is close and secret in such organizations, goals and aspirations of the employees are not considered in the budget. This triggers employee’s dissatisfaction on the job. Lack of goal-congruence is inevitable in organizations that imbibe Theory Alpha. This is because individual goals are not in line with organizational goals. The repressive nature of unilaterally prepared budget makes the employee to believe that the budget maker (decision maker) is thinking very low of him. The affected employee is disillusioned

.

The argument behind Theory Alpha is that it draws much from the tenets of the classical school of thought (the traditional management era). It is a theory that views subordinates and employees basically as children. Therefore, the writer submits Interalia:

Organizations that embrace Theory Alpha are identified with boredom. Their employees are viewed as indolent and indifferent robots that must be needled a bit, coerced by authoritarian power and closely supervised in order to make them perform in specified ways.

7.2.2. Theory Beta

Theory beta states as follows:

Individuals who are accountable for activities and performance under a budget must be allowed to participate really in the budget formation process and decisions by which that budget is established.

This theory is also known as Real Participatory Budgeting Theory. Accordingly, Theory Beta emphasizes real participation (real involvement in budgeting process). Real Participation refers to the budget formation process of joint decision making by two or more parties in which the decisions have future effects on those making them. As opposed to real participation, there is what is called pseudo participation. Pseudo participation is something that looks like participation but it is not full (real) involvement of all levels of the organization in budget formation and decision making process

. In all discussions made in this work, participation means real participation.

Theory Beta is based on modern accounting literature and postulates that underscore the following assertions:

1) Participatory budgeting process improves performance.

2) The participation or involvement of lower and middle management in the preparation of budgets and the establishment of clear targets against which performance can be judged are found to be motivating factors.

3) Participatory budgets are generally perceived positively by those who directly participate but negatively by employees who do not.

4) Real involvement in budgeting process cause organizational members to believe that they will advance their personal goals or aspirations by working towards the realization of organizational goals contained in the budget.

5) The influence of an enterprise budget on motivation may be greater if the budget is not imposed (forced on organizational members) but self-imposed (accepted by all organizational members directly affected by the budget)

| [5] | Bittle, LR Business in Action, New York, McGraw Hill Book Company Inc., 2019. |

| [7] | Cascio, WF Managing Human Resources, New York, McGraw Hill Book Company, 2019. |

| [31] | Umo, UP, The Management Accountant in Budgetary Process, Employees’ Motivation and Productivity: The Nigerian Case, Research Journal of Finance and Accounting, Hong Kong, 2014, 5(24): 178-184. |

| [36] | Umo, UP, Essays in Human Side of the Enterprise: Management Systems, Financial Planning and Employees’ Reactions in a Developing Economy of the 21st Century, European Journal of Business and Management Research, London, 2022, 7(3): 1-12. |

| [39] | Umo, UP, Contextual Anatomy of the Human Side of the Enterprise: Management Systems, Financial Planning and Employees’ Reactions, Business Management and Economics - Research Progress Vol. I, United Kingdom, B P International, 2024. |

[5, 7, 31, 36, 39]

.

Theory Beta portrays participation in budgeting process as a useful technique for dealing with the psychological problems of employees’ satisfaction, morale, motivation and productivity in the work place. It underscores the claim that participation can lead to high morale and increased initiative. Organizations that embrace Theory Beta believe that the most successful budgeting process is the one that permit managers with responsibility over cost control to prepare their own budget estimates. The budgets that they prepare become self-imposed in nature.

Real Participatory Budgeting Theory (Theory Beta) supports the postulation that participation in budget formation will increase the probability that organizational members involved will accept the budget as their own and become personally committed to the control system. Employees really involved in budgeting process will have more understanding of that particular budget and its needs. This is because employee’s morale and optimum participation are secured. Resistance to instructions, policies and programmes will reduce because employees are more likely to believe that the budget is theirs and not management’s

| [5] | Bittle, LR Business in Action, New York, McGraw Hill Book Company Inc., 2019. |

| [20] | Umo, UP, Contemporary Theories of Motivational Budgeting. International Journal of Advanced Multidisciplinary Research and Studies, 2025. https/doi.org/10.62225/2583049x.2025.5.2.4180 |

| [39] | Umo, UP, Contextual Anatomy of the Human Side of the Enterprise: Management Systems, Financial Planning and Employees’ Reactions, Business Management and Economics - Research Progress Vol. I, United Kingdom, B P International, 2024. |

[5, 20, 39]

.

Theory Beta supports the claim that the influence of a company’s budget on motivation may be greater if budget is not imposed but self -imposed. A budget is self-imposed if it is accepted by organizational members directly affected by the budget. Many organizations have found that the best way to make their budgets self -imposed is to have all levels of the organization participate in making the budget that affect them. This will trigger and secure goals internalization among organizational members. If goals are internalized by individuals responsible for making budgets, the probabilities of success are higher. Theory Beta submits that budgeting process provides a challenge and sense of responsibility needed to effectively motivate employees.

Two elements associated with the recommendations of Theory Beta are job enlargement and real participation. In budgetary science, job enlargement refers to the process of allowing subordinates and employees directly affected by budgets to control the way they prepare their budgets. It connotes the addition of one or more related tasks to raise work motivation during the budget formation process. Theory Beta submits that management of organizations should allow their subordinates and employees to take more responsibilities and also decide how to organize the budgeting process. This will reduce the psychological trauma associated with fatigue, low morale and apathy which occur because of the need for specialization in the work place. It boosts changes needed to increase the variety of tasks to be performed during the budgeting process. Job enlargement enables subordinate managers and employees to be given more varied tasks and increased scope for initiative and skill during the budget formation process. A subordinate manager who prepares his departmental budget should, in theory, increase performance and this leads to greater job satisfaction. Therefore, job enlargement reduces employees’ fatigue and relieves employees from boredom where work is specialized and repetitive in nature. It enables subordinates to exercise more control over the time span set for budget preparation and also promotes the use of a wide range of skills.

Real participation in budget formation is motivational in practice. It implies consultative management. It catapults various levels of the organization into the stream of decision making process, reduces boredom and secures employees’ commitment towards the realization of budget goals. Theory Beta emphasizes that the real value of participation at all levels is psychological. It is therefore, in the company’s best interest to attempt to meet the esteem and self-actualization needs of the participants by making budget formation process more challenging and giving individuals greater sense of responsibility. Participation in budget formation process relative to comparison and reviewing process often lead to motivation and improved performance. Real involvement in budgeting process attempts to get organizational participants’ ego involved, not just task involved

| [36] | Umo, UP, Essays in Human Side of the Enterprise: Management Systems, Financial Planning and Employees’ Reactions in a Developing Economy of the 21st Century, European Journal of Business and Management Research, London, 2022, 7(3): 1-12. |

[36]

.

7.2.3. Brief Comparative Dissection of Theory Alpha and Theory Beta

Both theories (Theory Alpha and Theory Beta) can be jointly described as twin theories of motivational budgeting. In relation to the concept of motivation, a close look at both theories reveals a common driving principle. People do what they are rewarded for doing. Both theories recognize diversity in human beings. People care about the kind of work they do.

Theory Alpha focuses almost exclusively on lower level needs (the needs that money can buy). People are expected to satisfy their higher order needs away from work. It is a little wonder, “managers complained that they paid their workers well and provided good job security, but suffered poor productivity”. In organizations that embrace Theory Alpha, their employees are seen as perpetually wanting animals. During budget formation, decision makers (budget maker) in such organizations view human beings as economic animals that are motivated by forces they cannot control. Budget makers that adopt Theory Alpha are authoritarian and strive to portray the human as a being of very limited dimensions, very nearly like the beast of burden.

In opposition to Theory Alpha is Theory Beta which supports the fact that organizations should no more offer the simple rules such as “Pay them well and watch them closely” as was practised during the classical era (the bedrock of Theory Alpha). Theory Beta emphasizes real participation in budget formation process which requires the management to provide information about budget formation activities, leaves the details of accomplishing them to the subordinates and stands ready to assist when problem arises. The decision maker does not watch everyone closely.

Theory Beta springs from the tenets of neo-classical era (the bedrock of modern behavioral assumptions in budgetary science). This theory supports the assertion that enterprise budgets are generally perceived positively by organizational members who directly participate in the formation process but negatively by those who do not. Subordinate managers and employees are both more productive and more satisfied with their jobs and colleagues when operating their budgets. This is psychological in terms of the associated benefits of budgeting in organizations. The writer submits inter-alia:

Indeed, there is a widespread belief, and belief is the appropriate term, that imbibing Theory Beta in organizations is a panacea: a cure for all the many ills associated with Theory Alpha.

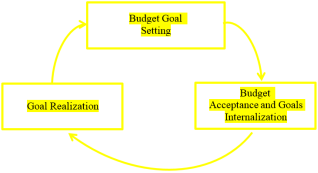

7.3. Goal Setting and Realization Theory (Usen Umo, 2024)

Goal setting and realization theory states as follows:

Budget goal should not only be set but should also be realized and the midpoint between goal setting and realization is the acceptance of the goal by all organizational members directly affected by the budget.

This theory can also be described as goal oriented theory of motivational budgeting. It emanates from the empirical pack of Usen Paul Umo in the first quarter of the twenty first (21

st) century

| [20] | Umo, UP, Contemporary Theories of Motivational Budgeting. International Journal of Advanced Multidisciplinary Research and Studies, 2025. https/doi.org/10.62225/2583049x.2025.5.2.4180 |

| [37] | Umo, UP, Goal Internalization: An Innovative Management Strategy for Budgetary Performance in 21st Century Firms of Developing Economics, European Journal of Business and Management Research, London, 2022, 7(3): 1-6. |

[20, 37]

. Goal setting and realization theory is anchored on the concept of budgetary system. It supports the claim that the true success of a budgetary system depends on the manner in which it is operated. A budgetary system is a hierarchical combination of the goal setting machine and the goal achieving machine of an enterprise.

Goal Setting and Realization Theory (Goal Oriented Theory) is very significant in motivational budgeting. It affirms the following assertions in the literature of modern business and accounting.

1) Goal setting focuses organizational activities in one direction.

2) Given that a budget goal is accepted and internalized, people tend to exert effort in proportion to the difficulty of the goal.

3) Difficult goals contained in the budget lead to more persistence than easy goals

| [20] | Umo, UP, Contemporary Theories of Motivational Budgeting. International Journal of Advanced Multidisciplinary Research and Studies, 2025. https/doi.org/10.62225/2583049x.2025.5.2.4180 |

| [25] | Pinder, CC, Work Motivation in Organizational Behaviour, New York, Psychology Press, 2018. |

| [37] | Umo, UP, Goal Internalization: An Innovative Management Strategy for Budgetary Performance in 21st Century Firms of Developing Economics, European Journal of Business and Management Research, London, 2022, 7(3): 1-6. |

| [39] | Umo, UP, Contextual Anatomy of the Human Side of the Enterprise: Management Systems, Financial Planning and Employees’ Reactions, Business Management and Economics - Research Progress Vol. I, United Kingdom, B P International, 2024. |

[20, 25, 37, 39]

.

The three dimensions (direction, effort and persistence) are central to the Goal Setting and Realization Theory. Persistence implies directed effort overtime. Direction implies a clear, defined and general manner of carrying out organizational activities through the enterprise members. It is a managerial function concerned with ensuring that employees do the jobs allotted to them with utmost cooperation usually through communication and orientation. Effort connotes the physical or mental energy made, committed or invested by organizational members for the purpose of achieving the goals contained in an enterprise budget. Therefore, persistence underscores the fact that an employee continues in his effort to perform a task in spite of difficulties, especially when other employees are against him. Motivation requires that employee’s persistence is finally rewarded when the enterprise management agree to pay for his committed effort

| [5] | Bittle, LR Business in Action, New York, McGraw Hill Book Company Inc., 2019. |

| [8] | Caplan, N; Doseh, P & Jekam, S Business Today, Enugu, New Era Publishers, 2018. |

[5, 8]

.

Budgets are generally perceived positively by organization members who really participate in their formation process but negatively by members who do not. Subordinate managers and employees are more productive, more satisfied with their jobs and more goals oriented when operating their own budgets. The manager (budget makers) experience a great sense of accomplishment when implementing their own budgets and they also have a greater commitment to making them work. In other words, such managers try to make their budgets become self-fulfilling prophecies

.

After the preparation of budgets, managers have a greater understanding of the budget requirement and difficulties. As a result, there shall be fewer communication problems and consequent errors in following instructions. In a dynamic business environment, this could result in more rapid modification and adjustment to their budgets. More also, when enterprise managers implement their own budgets, less time is wasted on goal realization between budget formation and budget implementation.

Budget goals should not only be set but should also be achieved. The critical step between the setting of a goal and its achievement is the acceptance of the goal and its internalization by the goal achieving machine (subordinate managers and employees directly affected by the budget). Therefore, the involvement of all levels of the organization in budgeting process has the consequences for goal setting, goal acceptance, goal internalization and goal realization. A budget goal even if externally imposed must receive some internal recognition if it is to be at all effective. In his literature on the human side of the enterprise, Usen Umo stressed:

No matter how much power a changer may possess; no matter how superior he may be; it is the changee who controls the final change decision. It is the employee, even the lowest paid one who ultimately decides whether to show up for work or not.

Goal Setting and Realization Theory identifies two key players in the budgetary system of firms namely; the goal setting machine and the goal achieving machine

| [20] | Umo, UP, Contemporary Theories of Motivational Budgeting. International Journal of Advanced Multidisciplinary Research and Studies, 2025. https/doi.org/10.62225/2583049x.2025.5.2.4180 |

| [36] | Umo, UP, Essays in Human Side of the Enterprise: Management Systems, Financial Planning and Employees’ Reactions in a Developing Economy of the 21st Century, European Journal of Business and Management Research, London, 2022, 7(3): 1-12. |

| [39] | Umo, UP, Contextual Anatomy of the Human Side of the Enterprise: Management Systems, Financial Planning and Employees’ Reactions, Business Management and Economics - Research Progress Vol. I, United Kingdom, B P International, 2024. |

[20, 36, 39]

.

Goal-setting machine refers to the top management whose function is to set budget goals for the subordinates and employees in an organization. They constitute the changer in the context of budgetary system of firms and occupy the highest position in the hierarchy of decision making body for organizations.

Goal achieving machine comprises of the subordinates and employees of organizations whose function is to work for the accomplishment of budget goals set by the top management. They are the changee in budgetary system of firms. The Goal setting and Realization Theory describes the goal-achieving machine as organizational members that control the final change decisions. Therefore, it is disceamible that organization is created by people for people. A budgeting system which ignores the human element is likely to be much less successful than those which are concerned with aligning personal and business goals. The Goal Setting and Realization Theory will be found very useful in this direction.

A major area of concern involves the relationship between motivational budgeting, goal setting, budget acceptance and goal realization. As subordinate managers and employees are given a larger influence on budget formation and decisions, their commitment to budget goal realization improves, partly because of the ego involved which their involvement generates. In budgetary science, this may be interpreted to mean a greater willingness by employees to accept the budget. With difficult goal, this acceptance will result in improved performance and persistence toward budget goal realization. Thus, budget acceptance intervened between goal setting and goal realization.

The management of firm cannot be effective unless their subordinates and employees accept their authority and also believe that they will advance their own goals if they work towards the realization of their organizational goal. Organizations that embrace the Goal Setting and Realization Theory will find it very useful in this direction. Subordinate managers and employees will be more productive, more satisfied with their job and colleagues and above all more goal oriented when operating their own budgets

| [5] | Bittle, LR Business in Action, New York, McGraw Hill Book Company Inc., 2019. |

| [7] | Cascio, WF Managing Human Resources, New York, McGraw Hill Book Company, 2019. |

| [36] | Umo, UP, Essays in Human Side of the Enterprise: Management Systems, Financial Planning and Employees’ Reactions in a Developing Economy of the 21st Century, European Journal of Business and Management Research, London, 2022, 7(3): 1-12. |

[5, 7, 36]

.

Goal Setting and Realization Theory support the claim that the involvement of all levels of the organization in their budget information, combined with other initiatives, bring the various levels of the organization into the stream of decision making process, create an enabling atmosphere where employees can satisfy their needs and cause them to identify with organizational goals contained in the budget, rather than just their own goals.

Figure 2. Budget Goals Cycle.

7.4. Expectations Theory (Usen Umo, 2024)

Expectations theory states that employees behave in accordance with their expectations about the outcome from the various kinds of behaviours and the satisfaction they expect to gain form successful budgeting process in the form of satisfying their personal goals.

Two important aspects highlighted in this theory are:

1) ^Expectations about the out comes from various kinds of behaviours.

2) ^Satisfaction expected to be gained from successful budgeting process in the form of satisfying personal goals.

Expectations theory is the outgrowth of the research work of the following:

E. C. Tolman

In 1932, E. C. Tolman published his psychological literature on “Purposive Behaviour in Animals and Men”

| [5] | Bittle, LR Business in Action, New York, McGraw Hill Book Company Inc., 2019. |

| [7] | Cascio, WF Managing Human Resources, New York, McGraw Hill Book Company, 2019. |

| [34] | Umo, UP, Impact of Budgetary Process on Morale, Motivation and Productivity of Employees, MBA Thesis, Uyo, University of Uyo Library, 1999. |

| [39] | Umo, UP, Contextual Anatomy of the Human Side of the Enterprise: Management Systems, Financial Planning and Employees’ Reactions, Business Management and Economics - Research Progress Vol. I, United Kingdom, B P International, 2024. |

[5, 7, 34, 39]

.

Victor Vroom

In 1964 Victor Vroom espoused on the work of E. C. Tolman and published his research literature on “Work and Motivation”

| [28] | Skinner, SJ & Ivancevich, JM, Business, Homewood, Richard D. Irwin Inc., 2022. |

[28]

.

Usen Paul Umo

In the first quarter of twenty first (21

st) century, Usen Umo promoted the works of E. C Tolman and Victor Vroom by publishing some empirical literature focused on the human side of the enterprise

| [32] | Umo, UP, Impact of Employees’ Behaviour on Budgetary Performance of Manufacturing Companies: A Study of Selected Quoted Firms in Nigeria, Ph. D. Dissertation, University of Port Harcourt Library, Port Harcourt, 2015. |

| [36] | Umo, UP, Essays in Human Side of the Enterprise: Management Systems, Financial Planning and Employees’ Reactions in a Developing Economy of the 21st Century, European Journal of Business and Management Research, London, 2022, 7(3): 1-12. |

| [39] | Umo, UP, Contextual Anatomy of the Human Side of the Enterprise: Management Systems, Financial Planning and Employees’ Reactions, Business Management and Economics - Research Progress Vol. I, United Kingdom, B P International, 2024. |

[32, 36, 39]

.

A close look at the Expectations Theory reveals the following:

7.4.1. Expectation About the Outcomes from Various Kinds of Behaviours

This implies employees’ perceptions that their behaviours will lead to a certain outcome. The concept of expectations forms the basis for a general model of behavior in organizational settings. Thus, employees believe that they will meet their aspirations if the enterprise budget is successful. That is, good reward shall accompany a successful enterprise budget. In other words, “the belief that budget goal achievement will lead to rewards” is a prediction about what will happen in the future. However, for employees to make this kind of prediction, trust and shared feeling of confidence must exist in the budgetary system of an organization that is promising them reward. This connotes budgeting by commitment.

Expectations Theory underscores budgeting by commitment. Budgeting by commitment is motivational. It triggers “trust” in the budgetary system of organizations. Employees are personally involved in the budget preparation process and therefore become personally committed to making the budget successful. Trust is raised amongst enterprise members if:

1) The budget formation process is participatory.

2) The enterprise budget is not imposed but self-imposed.

3) Budget is accepted and the goals are internalized by organizational members directly affected by the budget.

4) No secrecy is built around the budgeting process.

5) Anxiety is not raised in the organization.

If the above conditions prevail in an organization and the employees see the linkages between behaviours and rewards, then they will be motivated to perform better and budgets in organization will be successful

| [20] | Umo, UP, Contemporary Theories of Motivational Budgeting. International Journal of Advanced Multidisciplinary Research and Studies, 2025. https/doi.org/10.62225/2583049x.2025.5.2.4180 |

| [31] | Umo, UP, The Management Accountant in Budgetary Process, Employees’ Motivation and Productivity: The Nigerian Case, Research Journal of Finance and Accounting, Hong Kong, 2014, 5(24): 178-184. |

| [39] | Umo, UP, Contextual Anatomy of the Human Side of the Enterprise: Management Systems, Financial Planning and Employees’ Reactions, Business Management and Economics - Research Progress Vol. I, United Kingdom, B P International, 2024. |

[20, 31, 39]

.

7.4.2. Satisfaction Expected to Be Gained from Successful Budgeting Process in the Form of Satisfying Personal Goals

This precept connotes how much employees value the outcome of the budget. The more valued the outcome and the stronger the belief that an action will lead to the outcome, the stronger the employee’s motivation to perform the action.

Expectations Theory uses the term “utilities” to refer to the satisfaction derived from outcomes. This theory identifies two types of utilities namely intrinsic and extrinsic utilities.

1) Intrinsic Utilities

Intrinsic utilities come in two varieties viz:

1. The satisfaction associated with the work itself. The more an employee likes the work, the higher the utility derived.

2. The internal satisfactions that follow successful completion of the work

.

Examples of intrinsic utilities include enhanced self-esteem, self-confidence, the feeling of a task successfully completed (a job well done), the feeling of recognition through participation in budget formation process and the satisfaction gained by meeting the budget goals or objectives (5, 13m 20).

2) Extrinsic Utilities

Extrinsic utilities are rewards bestowed by others. Examples include praise, recognition, awards, bonuses, promotions and other forms of pay. Motivational budgeting vis-à-vis. Expectations Theory will be very useful in this direction. One of the central themes associated with Expectations Theory is that individuals usually assign probabilities of two types. One is the probability of success and the other is a set of probabilities associated with each extrinsic utility. That is, people will evaluate the likelihood that each extrinsic utility will actually be forthcoming upon successful completion of a task (successful realization of a budget goal). If a manager or employee has been told that accomplishing a particular task will yield a bonus, the probability will be close to 1. If the manager or employee believes that a promotion will follow successful completion of a task, but is not assured of it, the probability will be less than 1, perhaps even close to zero. The higher the probabilities of both types, the higher the motivation. Therefore,

The participation of all levels of the organization in their budget formation process is found to be motivational, brewing intrinsic and extrinsic utilities in organizational members, and the maximum motivation is achieved when the work itself is very satisfying, the intrinsic and extrinsic utilities are high, the probability of successful completion is high and the probabilities that extrinsic utilities will follow successful budget goal realization are also high.

7.5. Intended Effects Theory (Usen Umo, 2024)

Intended Effects Theory states as follows:

The manner in which an organization prepares its budget should either cause the employees to be satisfied with their jobs or prevent them from being dissatisfied with their jobs.

This theory can also be called Budget Incentive Theory. It springs from the research pack of Usen Paul Umo in the first quarter of the twenty first (21

st) century. It captures some related views on the early research work of F. V. Herzberg (1968) whose psychological literature provided an elaboration on “

Work and Nature of Man”. Budgeting must be seen in a much wider term than mere technique or procedure; it is a process that affects and in turn is affected by managerial and employees’ attitudes and behaviours

| [4] | Bateman, TS & Zeithaml, CP. Management: Function and Strategy, Homewood, Richard D. Irwin Inc., 2017. |

| [5] | Bittle, LR Business in Action, New York, McGraw Hill Book Company Inc., 2019. |

| [20] | Umo, UP, Contemporary Theories of Motivational Budgeting. International Journal of Advanced Multidisciplinary Research and Studies, 2025. https/doi.org/10.62225/2583049x.2025.5.2.4180 |

[4, 5, 20]

.

Intended Effects Theory points to the fact that the satisfaction of employees’ needs in budgeting process has one of two effects. It is a recipe for learning the law of effects in budgetary science and grows from the precept that employees aspire to satisfy two broad categories of needs namely the lower order needs and the higher order needs. Budget Incentive Theory (Intended Effects theory) attempts to show that the satisfaction of both categories of needs (lower order and higher order needs) at least in part, will secure employees” needs for achievement, affiliation or power in organizations

| [20] | Umo, UP, Contemporary Theories of Motivational Budgeting. International Journal of Advanced Multidisciplinary Research and Studies, 2025. https/doi.org/10.62225/2583049x.2025.5.2.4180 |

| [39] | Umo, UP, Contextual Anatomy of the Human Side of the Enterprise: Management Systems, Financial Planning and Employees’ Reactions, Business Management and Economics - Research Progress Vol. I, United Kingdom, B P International, 2024. |

[20, 39]

.

Beneficial changes will occur in organizations that embrace Intended Effects Theory. It is a theory that enables the organization to tap the benefits associated with employees’ involvement and real participation in budget preparation process. Intended Effects Theory supports changes in the manner which budgets are prepared in organizations. For example, a change from autocratic budgetary system to participatory budgetary system. If all levels of the organization participate in making the budget that affect them, motivation is secured. The employees will accept the budget as theirs and not management’s. Employees’ efforts will be geared toward budget goal realization. If enterprise management reward behaviours (such as high quality work, high productivity, timely reports or creative suggestions), these behaviours are likely to increase. However, the converse is also true. Managers should not expect sustained high performance from employees:

1) If they impose budget on employees.

2) If they ignore employees’ contributions during the budget formation process.

3) If they consistently refuse to reward employees’ behaviour.

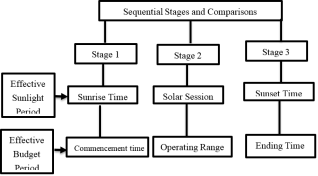

7.6. Effective Budget Period Theory (Usen Umo, 2024)

Effective budget period theory states as follows:

Effective budget period is a period which is definable; goal oriented and significantly affect all organizational members and activities under the budget.

This Theory springs from the research pack of Usen Paul Umo in the first quarter of the twenty first (21st) century. In relation to Effective Budget Period Theory, the following corollaries are discernible:

1) A budget period is effective if it is definable.

2) A budget period is effective if it is goal oriented.

3) A budget period is effective if it significantly affect all organizational resources and activities under the budget.

| [20] | Umo, UP, Contemporary Theories of Motivational Budgeting. International Journal of Advanced Multidisciplinary Research and Studies, 2025. https/doi.org/10.62225/2583049x.2025.5.2.4180 |

| [40] | Leong, GC. (2019), Certificate Physical and Human Geography, London, Oxford University Press. |

| [41] | Oboli, HON, An Outline Geography of West Africa, London, Harrap Publishers, 2008. |

| [42] | Wright, T, Positive Organizational Behaviour: Employee Happiness and health, Journal of Organizational Behaviour, Rotterdam, The Netherlands, 2014, 16(4): 79-88. |

[20, 40-42]

.

Effective Budget Period Theory underscores systematic analysis, observation and measurable time period during which organizational resources and activities under the budget relate. Thus, effective budget period is the time that the budget covers and which the budget is put into action. For instance, effective sunlight period is the time the sun covers in daylight. The course (operational direction or route that the sun moves), the time it takes and the use of solar energy it provides (effective sunlight) guide daily activities and individuals under the sum. The systematic analysis of the fundamentals, time and use of the solar period (sunlight) in relation to sunrise, daytime and sunset detect the basic intellectual foundation for understanding the Effective Budget Period Theory. In other words, Effective Budget Period Theory draws its basics from the appearance and time phenomenon of the shiny sun in the sky

| [5] | Bittle, LR Business in Action, New York, McGraw Hill Book Company Inc., 2019. |

| [7] | Cascio, WF Managing Human Resources, New York, McGraw Hill Book Company, 2019. |

| [20] | Umo, UP, Contemporary Theories of Motivational Budgeting. International Journal of Advanced Multidisciplinary Research and Studies, 2025. https/doi.org/10.62225/2583049x.2025.5.2.4180 |

[5, 7, 20].

A firm without a budget is just like a ship without a course. It does not know where it is going or where it should go. It does not know the next rock it is likely going to hit. Such a firm can also be likened to a team of community operatives in a given geographical area who decides to work in the daytime without the sun in the sky. Naturally, in such a situation, the community is devoid of sunlight and the community operatives may not succeed. This is because there are three observable, definable and identifiable time sessions exhibited by the shiny sun that are crucial to all humans and activities under the influence of light provided by the sum in the sky. These three-time sessions are the sunrise time, solar session and sunset time. These three-time sessions can also be described as the three sequential stages in effective sunlight period. As the presence of the sun in the sky determines the effective time available for use in carrying out activities under the direct influence of the sun, the budget in an organization determines the effective time available for activities under the direct influence of the budget

| [40] | Leong, GC. (2019), Certificate Physical and Human Geography, London, Oxford University Press. |

[40]

. This supports the reason why the budget is a financial plan that must be prepared and approved prior to a well-defined period of time

| [12] | Garrison, RH Management Accounting, Boston, Richard D. Irwin Inc., 2020. |

| [13] | Garrison, RH; Noreen, EW & Brewer, PC, Managerial Accounting, New York, McGraw Hill Book Company, 2021. |

[12, 13]

. The three time sessions associated with effective budget period are commencement time, operating range and ending time. The sequential stages and comparisons are given below:

Figure 3. Comparative Trend in effective sunlight period and effective budget period.

An analogy between effective sunlight period and effective budget period is given below:

7.6.1. Sunrise Time and Budget Commencement Time

Sunrise marks the emergence of the sun in the sky. It is the time when the sun first appears above the horizon in the morning. Sunrise can also be described as daybreak or sunup. It dictates the commencement time for those activities and humans under the influence of the sun to start using sunlight. That is, sunrise is the time which the rising sun brews incoming sunlight for all operational activities and humans under the direct influence of the sun

| [40] | Leong, GC. (2019), Certificate Physical and Human Geography, London, Oxford University Press. |

| [41] | Oboli, HON, An Outline Geography of West Africa, London, Harrap Publishers, 2008. |

[40, 41]

.

The budget commencement time is likened to the sunrise time. It marks the time that the organization starts to operate the budget that it earlier developed and approved

| [13] | Garrison, RH; Noreen, EW & Brewer, PC, Managerial Accounting, New York, McGraw Hill Book Company, 2021. |

| [24] | Pandey, IM, Financial Management, New Delhi, Vikas Publishing House PVT Limited, 2021. |

[13, 24]

. It is the time that organizational members start to put the budget into action. The budget commencement time defines the time that the budget begins to have effect on organizational members and activities under the budget

| [20] | Umo, UP, Contemporary Theories of Motivational Budgeting. International Journal of Advanced Multidisciplinary Research and Studies, 2025. https/doi.org/10.62225/2583049x.2025.5.2.4180 |

| [33] | Lucey, T, Casting, London, DP Publications Limited, 2017. |

| [39] | Umo, UP, Contextual Anatomy of the Human Side of the Enterprise: Management Systems, Financial Planning and Employees’ Reactions, Business Management and Economics - Research Progress Vol. I, United Kingdom, B P International, 2024. |

[20, 33, 39]

.

7.6.2. Solar Session and Budget Operation Range

Solar session refers to the period during the day, between the time it gets light and the time it gets dark. It is the effective sunlight period. The rising sun in the morning surely sets in the evening. The effective solar session is called sunlight or daylight. It is described as “the period of shiny sun in action”. It shows the time between which the sun rises from the east and sets in the west. Effective solar session implants in the minds of humans that sunlight period is the time available for use in accomplishing daily tasks, activities or functions under direct influence of the sun. It is the range of time between sunrise and sunset

| [40] | Leong, GC. (2019), Certificate Physical and Human Geography, London, Oxford University Press. |

| [41] | Oboli, HON, An Outline Geography of West Africa, London, Harrap Publishers, 2008. |

| [42] | Wright, T, Positive Organizational Behaviour: Employee Happiness and health, Journal of Organizational Behaviour, Rotterdam, The Netherlands, 2014, 16(4): 79-88. |

[40-42]

.

In a similar trend, the budget operating range is likened to the solar session under analogy. The time between which a budget starts (budget commencement time) and ends (budget ending time) is known as budget operating range

. This operating range of organizational budget is described as “the period of budget in action”. It is a period in which the budget affects and in turn is affected by all managerial and employees’ attitudes and behaviours. It marks the period that a budget has pervasive effect on all activities of the organization under the budget

| [21] | Lounderback, JG, & Hirsch, ML. Cost Accounting: Accumulation, Analysis and Use, Homewood, Richard D. Irwin Inc., 2016. |

| [34] | Umo, UP, Impact of Budgetary Process on Morale, Motivation and Productivity of Employees, MBA Thesis, Uyo, University of Uyo Library, 1999. |

| [36] | Umo, UP, Essays in Human Side of the Enterprise: Management Systems, Financial Planning and Employees’ Reactions in a Developing Economy of the 21st Century, European Journal of Business and Management Research, London, 2022, 7(3): 1-12. |

[21, 34, 36]

.

During the solar session, all humans and activities under the sun experience effect of the prevailing sunlight. Equally, during the operating range, all organizational members and activities are affected by the budget developed and approved for the period.

7.6.3. Sunset Time and Budget Ending Time

The rising sun shines and sets in the sky. The time that the sun sets in the sky is known as sunset time. It is the time when the sun slowly `goes down in the sky and night begins. At this time, the different parts of the earth that are directly influenced by the sun start to miss the setting sun alongside the prevailing sunlight. Sunset time marks the time when the sun slowly goes below the horizon and represents the particular time that the sun declines in the sky. It is also described as sundown

| [40] | Leong, GC. (2019), Certificate Physical and Human Geography, London, Oxford University Press. |

| [41] | Oboli, HON, An Outline Geography of West Africa, London, Harrap Publishers, 2008. |

[40, 41].

The budget ending time is likened to sunset time. It marks the time that an organization ends the operation of its budget. It is the particular time that the budget is put out of action. It is the time after which the approved budget does not have effect on organizational members and operational activities

| [12] | Garrison, RH Management Accounting, Boston, Richard D. Irwin Inc., 2020. |

| [13] | Garrison, RH; Noreen, EW & Brewer, PC, Managerial Accounting, New York, McGraw Hill Book Company, 2021. |

| [20] | Umo, UP, Contemporary Theories of Motivational Budgeting. International Journal of Advanced Multidisciplinary Research and Studies, 2025. https/doi.org/10.62225/2583049x.2025.5.2.4180 |

| [39] | Umo, UP, Contextual Anatomy of the Human Side of the Enterprise: Management Systems, Financial Planning and Employees’ Reactions, Business Management and Economics - Research Progress Vol. I, United Kingdom, B P International, 2024. |

[12, 13, 20, 39].

From Effective Budget Period Theory, it is deducible that effective budget period is the time the budget covers and which really comes into use for the purpose of successfully producing the intended results. Effective budget period spans through the budget commencement time, operating range and ending time.