In the evolving landscape of the digital economy, both financial and digital literacy have become essential. This study investigates the mediating role of DFL in the relationship between financial attitude, financial socialisation, and personal financial management behaviour (PFMB) among working and non-working women in Punjab, India. Drawing on the Theory of Planned Behaviour, the research explores how psychological and social factors influence financial behaviour through the lens of digital competence. Using a structured questionnaire, data were collected from a representative sample of women across various districts in Punjab. The study employed Smart PLS 4.0 to examine direct and mediated relationships among the key constructs. The findings reveal that both financial attitude and financial socialisation significantly influence PFMB, and that DFL plays a partial mediating role in these relationships. Notably, working women exhibited higher levels of DFL and more proactive financial behaviours compared to their non-working counterparts. The results emphasise the importance of digital financial literacy as a critical enabler of financial empowerment for women, particularly in semi-urban and rural areas. This study contributes to the growing discourse on digital financial inclusion and offers practical implications for policymakers, educators, and financial institutions seeking to bridge gender and digital divides in financial access and decision-making.

| Published in | International Journal of Business and Economics Research (Volume 15, Issue 3) |

| DOI | 10.11648/j.ijber.20261503.11 |

| Page(s) | 58-70 |

| Creative Commons |

This is an Open Access article, distributed under the terms of the Creative Commons Attribution 4.0 International License (http://creativecommons.org/licenses/by/4.0/), which permits unrestricted use, distribution and reproduction in any medium or format, provided the original work is properly cited. |

| Copyright |

Copyright © The Author(s), 2026. Published by Science Publishing Group |

Digital Financial Literacy, Financial Attitude, Financial Socialisation, Personal Financial Management Behaviour, Women, Punjab, Financial Inclusion

Demographic Characteristics | Classes | Frequency | Percentages |

|---|---|---|---|

Age (Years) | 18 – 25 | 175 | 32.1% |

26 – 35 | 200 | 36.6% | |

36 – 45 | 125 | 22.9% | |

46 – 55 | 42 | 7.7% | |

55 & above | 4 | 0.7% | |

Educational Qualification | Matric | 34 | 6.2% |

Sr. Sec | 57 | 10.5% | |

Graduation | 201 | 36.8% | |

Post -Graduation | 245 | 45% | |

Other | 9 | 1.6% | |

Level of Income | Less than ₹ 5 lakh | 337 | 61.72% |

₹ 5 lakh - ₹10 lakh | 177 | 32.41% | |

₹ 10 lakh - ₹ 15 lakh | 27 | 4.94% | |

₹ 15 lakh - ₹ 20 lakh | 4 | 0.73% | |

Marital Status | Married | 195 | 35.7% |

Unmarried | 297 | 54.4% | |

Divorced | 14 | 2.6% | |

Separated | 29 | 5.3% | |

Widow | 11 | 2.0% | |

Current Status | Working | 306 | 56% |

Non- Working | 240 | 44% | |

Type of Family | Joint | 290 | 53.1% |

Nuclear | 256 | 46.9% | |

Area | Rural | 316 | 57.8% |

Urban | 230 | 42% |

Items Factor Loadings VIF | CA | CR | AVE |

|---|---|---|---|

Financial Attitude (FA) | 0.895 | 0.915 | 0.547 |

FA1 0.755 1.287 FA2 0.774 1.175 FA3 0.768 1.712 FA4 0.713 1.854 FA5 0.763 2.658 FA6 0.802 1.159 FA7 0.793 2.876 FA8 0.762 2.608 FA9 0.799 1.162 | |||

Financial Socialisation (FS) | 0.899 | 0.917 | 0.529 |

FS1 0.713 1.533 FS2 0.726 1.878 FS3 0.798 1.513 FS4 0.801 2.973 FS5 0.734 1.341 FS6 0.761 2.252 FS7 0.775 2.526 FS8 0.785 1.517 FS9 0.701 1.319 FS10 0.739 2.546 | |||

Digital Financial Literacy (DFL) | 0.912 | 0.927 | 0.538 |

DFL1 0.593 1.427 DFL2 0.637 1.646 DFL3 0.719 2.085 DFL4 0.625 1.791 DFL5 0.673 1.059 DFL6 0.694 1.186 DFL7 0.762 2.451 DFL8 0.846 1.132 DFL9 0.788 2.952 DFL10 0.804 1.212 DFL11 0.867 1.492 | |||

Personal Financial Management Behaviour (PFMB) | 0.932 | 0.941 | 0.517 |

PFMB1 0.763 1.254 | |||

PFMB2 0.709 1.317 | |||

PFMB3 0.798 2.501 | |||

PFMB4 0.761 1.218 | |||

PFMB5 0.694 1.928 | |||

PFMB6 0.848 1.001 | |||

PFMB7 0.786 1.102 | |||

PFMB8 0.841 1.231 | |||

PFMB9 0.812 1.028 | |||

PFMB10 0.721 1.437 | |||

PFMB11 0.778 1.119 | |||

PFMB12 0.753 1.113 | |||

PFMB13 0.714 1.362 | |||

PFMB14 0.606 1.633 | |||

PFMB15 0.734 1.626 | |||

Constructs | DFL | FA | FS | PFMB | Construct | DFL | FA | FS | PFMB |

|---|---|---|---|---|---|---|---|---|---|

DFL | DFL | 0.733 | |||||||

FA | 0.836 | FA | 0.716 | 0.741 | |||||

FS | 0.814 | 0.803 | FS | 0.708 | 0.711 | 0.727 | |||

PFMB | 0.719 | 0.779 | 0.805 | PFMB | 0.702 | 0.719 | 0.714 | 0.819 |

Hypothesis | Beta | Standard deviation | T-Value | P-values Comment |

|---|---|---|---|---|

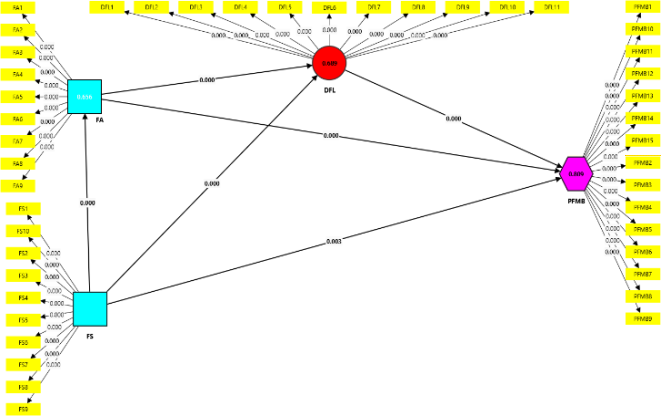

H1: FA -> PFMB | 0.308 | 0.053 | 5.795 | 0.000 Supported |

H2: FS -> PFMB | 0.175 | 0.059 | 2.944 | 0.003 Supported |

H3: FA -> DFL | 0.323 | 0.062 | 5.219 | 0.000 Supported |

H4: FS -> DFL | 0.547 | 0.059 | 9.316 | 0.000 Supported |

H5: FS -> FA | 0.811 | 0.022 | 37.14 | 0.001 Supported |

H6: DFL -> PFMB | 0.482 | 0.054 | 8.975 | 0.000 Supported |

Hypothesis | Original Sample | SD | T-value | P-value Comment |

|---|---|---|---|---|

H7: FA -> DFL -> PFMB | 0.196 | 0.044 | 4.46 | 0.000 Supported |

H8: FS -> DFL -> PFMB | 0.087 | 0.03 | 2.953 | 0.003 Supported |

Construct | R-square | R-square adjusted |

|---|---|---|

PFMB | 0.609 | 0.607 |

FA | Financial Attitude |

FS | Financial Socialisation |

DFL | Digital Financial Literacy |

PFMB | Personal Financial Management Behaviour |

| [1] | Lyons AC, Kass-Hanna J. A methodological overview to defining and measuring “digital” financial literacy. Financial planning review. 2021 Jun; 4(2): 1113. |

| [2] | OECD. G20/OECD INFE Policy Guidance on Digitalisation and Financial Literacy. 2018; pp. 1–25. |

| [3] | Goyal K, Kumar S, Xiao JJ. Antecedents and consequences of Personal Financial Management Behavior: a systematic literature review and future research agenda. International journal of bank marketing. 2021 Jun 1; 39(7): 1166-207. |

| [4] | Shim S, Serido J, Tang C, Card N. Socialization processes and pathways to healthy financial development for emerging young adults. Journal of Applied Developmental Psychology. 2015 May 1; 38: 29-38. |

| [5] | Singh C, Kumar R. Financial literacy among women: Indian Scenario. Universal Journal of Accounting and Finance. 2017; 5(2): 46-53. |

| [6] | Purohit H, Chutani R. Financial literacy and its effect on financial decisions of households in Punjab and Haryana State. International Journal of Business and Globalisation. 2022; 31(3): 251-71. |

| [7] | Yong CC, Yew SY, Wee CK. Financial knowledge, attitude and behaviour of young working adults in Malaysia. Institutions and Economies. 2018 Sep 14; 10(4). |

| [8] | Siswanti I, Halida AM. Financial knowledge, financial attitude, and financial management behavior: Self–control as mediating. The International Journal of Accounting and Business Society. 2020 Apr 30; 28(1): 105-132. |

| [9] | Coskun A, Dalziel N. Mediation effect of financial attitude on financial knowledge and financial behaviour: The case of university students. International Journal of Research in Business and Social Science. 2020; 9(2): 1-8. |

| [10] | SUYANTO S, SETIAWAN D, RAHMAWATI R, WINARNA J. The impact of financial socialization and financial literacy on financial behaviours: an empirical study in Indonesia. The Journal of Asian Finance, Economics and Business. 2021; 8(7): 169-80. |

| [11] | Sabri MF, Anthony M, Wijekoon R, Suhaimi SS, Abdul Rahim H, Magli AS, Isa MP. The influence of financial knowledge, financial socialization, financial behaviour, and financial strain on young adults’ financial well-being. International Journal of Academic Research in Business and Social Sciences. 2021 Dec 18; 11(12): 566-86. |

| [12] | Potrich AC, Vieira KM, Mendes-Da-Silva W. Development of a financial literacy model for university students. Management Research Review. 2016 Mar 21; 39(3): 356-76. |

| [13] | Manchanda P, Sukhija S. A Study on Factors affecting Financial Literacy among working women in Punjab. Journal of Emerging Technologies and Innovative Research. 2019; 6(1): 650-7. |

| [14] | Yahaya R, Zainol Z, Osman JH, Abidin Z, Ismail R. The effect of financial knowledge and financial attitudes on financial behaviour among university students. International Journal of Academic Research in Business and Social Sciences. 2019 Aug; 9(8): 22-32. |

| [15] | Adiputra IG, Patricia E. The effect of financial attitude, financial knowledge, and income on financial management behaviour. In Tarumanagara International Conference on the Applications of Social Sciences and Humanities (TICASH 2019) 2020 May 20 (pp. 107-112). Atlantis Press. |

| [16] | Syarif A, Putri A. The influence of financial attitude, financial knowledge, and personal income on personal financial management behaviour. Adpebi International Journal of Multidisciplinary Sciences. 2022 Aug 26; 1(1): 145-54. |

| [17] | Azidzul NA, Shahar NB, Yussoff NE, Fuzi SF. The influence of financial attitude, literacy, knowledge and skills on financial management behaviour among students in public university. International Journal of Advanced Research in Economics and Finance. 2023 Dec 1; 5(4): 50-60. |

| [18] | Kumar P, Ahlawat P, Deveshwar A, Yadav M. Do villagers’ financial socialization, financial literacy, financial attitude, and financial behaviour predict their financial well-being? Evidence from an emerging India. Journal of Family and Economic Issues. 2024 Jul 26: 1-9. |

| [19] | Miglani, V. Understanding the Effect of Peers on the Financial Attitude and Financial Behaviour of Women in Kaithal, Haryana. International Journal of Social Science Research and Review. 2024: 7(8), 151-164. |

| [20] | Barus IS, Lasniroha T, Bayunitri BI. Navigating the Digital Financial Landscape: The Role of Financial Literacy and Digital Payment Behaviour in Shaping Financial Management Among Generation Z Students. Journal of Logistics, Informatics and Service Science. 2024; 11(7): 302-23. |

| [21] | Gudmunson CG, Danes SM. Family financial socialization: Theory and critical review. Journal of family and economic issues. 2011 Dec; 32: 644-67. |

| [22] | Jamal AA, Ramlan WK, Karim MA, Osman Z. The effects of social influence and financial literacy on savings behaviour: A study on students of higher learning institutions in Kota Kinabalu, Sabah. International Journal of Business and Social Science. 2015 Nov; 6(11): 110-9. |

| [23] | Antoni ZL, Rootman C, Struwig FW. The influence of parental financial socialisation techniques on student financial behaviour. International Journal of Economics and Finance Studies. 2019; 11(2): 72-88. |

| [24] | Ameliawati M, Setiyani R. The influence of financial attitude, financial socialisation, and financial experience to financial management behaviour with financial literacy as the mediation variable. KnE Social Sciences. 2018 Oct 22: 811-32. |

| [25] | Khawar S, Sarwar A. Financial literacy and financial behaviour with the mediating effect of family financial socialization in the financial institutions of Lahore, Pakistan. Future Business Journal. 2021 Dec; 7: 1-1. |

| [26] | Goyal K, Kumar S, Hoffmann A. The direct and indirect effects of financial socialization and psychological characteristics on young professionals' personal financial management behaviour. International Journal of Bank Marketing. 2023 Dec 1; 41(7): 1550-84. |

| [27] | Kaur G, Singh M. Pathways to individual financial well-being: Conceptual framework and future research agenda. FIIB Business Review. 2024 Jan; 13(1): 27-41. |

| [28] | Nanda, S. Financial Socialisation and Promotion of Financial Inclusion, among Women Self-Help Group Members: An analysis. Journal of Informatics Education and Research. 2024: 4(1). |

| [29] | Showkat M, Nagina R, Baba MA, Yahya AT. The impact of financial literacy on women’s economic empowerment: exploring the mediating role of digital financial services. Cogent Economics & Finance. 2025 Dec 31; 13(1): 2440444. |

| [30] | Tiwari CK, Gopalkrishnan S, Kaur D, Pal A. Promoting Financial Literacy through Digital Platforms: A Systematic Review of Literature and Future Research Agenda. Journal of General Management Research. 2020 Dec 1; 7(2). |

| [31] | Azeez NA, Akhtar SJ. Digital financial literacy and its determinants: empirical evidence from rural India. South Asian Journal of Social Studies and Economics. 2021; 11(2): 8-22. |

| [32] | Prasad H, Meghwal D, Dayama V. Digital financial literacy: A study of households of Udaipur. Journal of Business and Management. 2018 Dec 1; 5: 23-32. |

| [33] | OECD. OECD/INFE 2020 International Survey of Adult Financial Literacy. 2020. |

| [34] | Walsh B, Lim H. Millennials' adoption of personal financial management (PFM) technology and financial behaviour. Financial Planning Review. 2020 Sep; 3(3): 1095. |

| [35] | Ravikumar T, Suresha B, Prakash N, Vazirani K, Krishna TA. Digital financial literacy among adults in India: Measurement and validation. Cogent Economics & Finance. 2022 Dec 31; 10(1): 2132631. |

| [36] | Qamar A, Rasheed N, Kamal A, Rauf S, Nizam K. Factors affecting financial behaviour of millennial Gen Z: Mediating role of digital financial literacy integration. International Journal of Social Science & Entrepreneurship. 2023; 3(3): 330-52. |

| [37] | Wijayanti TC, Naim S, Hendayani N, Alfiana A, Hanum F. Identify the use of economics for family financial management in digital days. Indonesian Interdisciplinary Journal of Sharia Economics (IIJSE). 2024; 7(1): 325-45. |

| [38] | Aryan LA, Alsharif A, Alquqa EK, Ebbini A, Mohammad M, Alzboun N, Alshurideh MT, Shelash Al-Hawary SI. How digital financial literacy impacts financial behaviour in Jordanian millennial generation. International Journal of Data & Network Science. 2024 Jan 1; 8(1). |

| [39] | Abdallah W, Tfaily F, Harraf A. The impact of digital financial literacy on financial behaviour: customers’ perspective. Competitiveness Review: An International Business Journal. 2025 Feb 11; 35(2): 347-70. |

| [40] | Shehadeh M, Dawood HM, Hussainey K. Digital financial literacy and usage of cashless payments in Jordan: the moderating role of gender. International Journal of Accounting & Information Management. 2025 Apr 28; 33(2): 354-82. |

| [41] | Imawan R, Putra WP, Alqahtani R, Milakis ED, Dumchykov M. Enhancing Financial Literacy in Young Adults: An Android-Based Personal Finance Management Tool. Journal of Hypermedia & Technology-Enhanced Learning. 2025 Jan 27; 3(1): 64-88. |

| [42] | Aulakh IK, Saluja R. Financial Autonomy of Women in Punjab: An In-depth Analysis. Journal of General Management Research. 2017 Jul 1; 4(2). |

| [43] | Chhillar N, Arora S. Personal financial management behaviour using digital platforms and its domains. Journal of Financial Management, Markets and Institutions. 2022 Dec 25; 10(02): 2250009. |

| [44] | Haudi H. The Role of Financial Literacy, Financial Attitudes, and Family Financial Education on Personal Financial Management and Locus of Control of University Students. International Journal of Social and Management Studies. 2023 Mar 1; 4(2): 107-16. |

| [45] | Kartini T, Sugeng B, Wahyono H, Wardoyo C. DETERMINANTS OF FINANCIAL TECHNOLOGY (FINTECH) ADOPTION BEHAVIOR IN PERSONAL FINANCIAL MANAGEMENT AMONG ECONOMICS EDUCATION STUDENTS IN EAST JAVA. JURNAL EKONOMI PENDIDIKAN DAN KEWIRAUSAHAAN. 2025; 13(1): 21-58. |

| [46] | Lusardi A, Mitchell OS. The economic importance of financial literacy: Theory and evidence. American Economic Journal: Journal of Economic Literature. 2014 Mar 1; 52(1): 5-44. |

| [47] | LeBaron AB, Kelley HH. Financial socialization: A decade in review. Journal of family and economic issues. 2021 Jul; 42(Suppl 1): 195-206. |

| [48] | Lai MM, Tan WK. An empirical analysis of personal financial planning in an emerging economy. European Journal of Economics, Finance and Administrative Sciences. 2009 Feb; 16(16): 102-15. |

| [49] | Dew, J., & Xiao, J. J. The financial management behaviour scale: Development and validation. Journal of Financial Counselling and Planning, 2011; 22(1), 43. |

| [50] | Hair JF, Ringle CM, Sarstedt M. Partial least squares structural equation modelling: Rigorous applications, better results and higher acceptance. Long-range planning. 2013 Mar 14; 46(1-2): 1-2. |

| [51] | Hair JF. A primer on partial least squares structural equation modelling (PLS-SEM). sage; 2014. |

| [52] | Patel AT, Kumar S. A Study of Awareness, Attitude and Factors influencing Personal Financial Planning for Residents of Gujarat. Unpublished doctoral dissertation. Gujarat Technological University, Ahmedabad (Gujarat), India. 2017 Nov. |

| [53] | Normawati R, Rahayu S, Worokinasih S. Financial knowledge, digital financial knowledge, financial attitude, financial behaviour and financial satisfaction on millennials. InICLSSEE 2021: proceedings of the 1st international conference on law, social science, economics, and education, ICLSSEE 2021 May 5 (p. 317). |

| [54] | Ardiandana M. R, Sriyono S, & Setiyono W. P. Financial Literacy, Financial Attitude, Education Level and Lifestyle on Personal Financial Management of Students in Sidoarjo. Journal IIMU Management Advantage, 2024; 8(1), 48-60. |

| [55] | Acharya P, Poudel O. Interplay of financial socialization, financial behaviour, and adult financial well-being. Management Dynamics. 2023 Oct 11; 26(1): 33-42. |

| [56] | Abdul Ghafoor K, Akhtar M. Parents’ financial socialization or socioeconomic characteristics: which has more influence on Gen-Z’s financial wellbeing? Humanities and Social Sciences Communications. 2024 Apr 18; 11(1): 1-6. |

| [57] | Pak T. Y, Fan L, & Chatterjee S. Financial socialization and financial well-being in early adulthood: the mediating role of financial capability. Family Relations. 2024: 73(3), 1664-1685. |

| [58] | Lewis M, Perry M. Follow the money: Managing personal finance digitally. In Proceedings of the 2019 CHI Conference on Human Factors in Computing Systems 2019 May 2 (pp. 1-14). |

| [59] | Kusumapradana BS, Aisyah S. The Effect of Financial Literacy and Financial Attitude on the Use of Digital Wallets Among Students in Surakarta City. AJAR. 2022 Aug 31; 5(02): 193-206. |

| [60] | Koskelainen T, Kalmi P, Scornavacca E, Vartiainen T. Financial literacy in the digital age—A research agenda. Journal of Consumer Affairs. 2023 Jan; 57(1): 507-28. |

| [61] | Moko W, Sudiro A, Kurniasari I. The effect of financial knowledge, financial attitude, and personality on financial management behaviour. International Journal of Research in Business & Social Science. 2022 Dec 1; 11(9). |

| [62] | Xolile Antoni. The role of family structure on financial socialisation techniques and behaviour of students in the Eastern Cape, South Africa, Cogent Economics & Finance. 2023: 11: 1, 2196844, |

| [63] | Dewmini EA, Wijekumara JM, Sugathadasa DD. Digital Financial Literacy on Financial Behaviour Among Management Undergraduates of State Universities in Sri Lanka. Journal of Management Matters. 2023 Dec 31; 10(2). |

| [64] | Dewi CS, Putri A, Situmorang SL. Role of Digital Financial Literacy and Digital Financial Behaviour on Financial Well-being in Indonesia. West Science Business and Management. 2024; 2(02): 293-303. |

| [65] | Mir MA. Digital Financial Literacy and Financial Well-Being. In Emerging Perspectives on Financial Well-Being 2024 (pp. 57-73). IGI Global. |

| [66] | Furinto A, Tamara D, Yenni Y, Rahman NJ. Financial and digital literacy effects on digital investment decision mediated by perceived socio-economic status. InE3S Web of Conferences 2023 (Vol. 426, p. 02076). EDP Sciences. |

| [67] | Ali M, Alamgir M, Nawaz MA. Emergence of the digital financial literacy, and its effect on the financial management behaviour among students of Pakistan. Pakistan Social Sciences Review. 2024 Apr 1; 8(2): 141-55. |

| [68] | Amnas MB, Selvam M, Parayitam S. FinTech and financial inclusion: Exploring the mediating role of digital financial literacy and the moderating influence of perceived regulatory support. Journal of Risk and Financial Management. 2024 Mar 7; 17(3): 108. |

| [69] | Kumar P, Pillai R, Kumar N, Tabash MI. The interplay of skills, digital financial literacy, capability, and autonomy in financial decision making and well-being. Borsa Istanbul Review. 2023 Jan 1; 23(1): 169-83. |

| [70] | Jusoh AM. Mediating effect of financial literacy on the influence of parental financial socialisation on subjective financial well-being of community college students. MOJEM: Malaysian Online Journal of Educational Management. 2024 Apr 1; 12(2): 28-49. |

APA Style

Kaur, K. (2026). Impact of Financial Attitude and Financial Socialisation on Women’s Personal Financial Management Behaviour: Exploring the Mediating Role of Digital Financial Literacy. International Journal of Business and Economics Research, 15(3), 58-70. https://doi.org/10.11648/j.ijber.20261503.11

ACS Style

Kaur, K. Impact of Financial Attitude and Financial Socialisation on Women’s Personal Financial Management Behaviour: Exploring the Mediating Role of Digital Financial Literacy. Int. J. Bus. Econ. Res. 2026, 15(3), 58-70. doi: 10.11648/j.ijber.20261503.11

@article{10.11648/j.ijber.20261503.11,

author = {Kuldip Kaur},

title = {Impact of Financial Attitude and Financial Socialisation on Women’s Personal Financial Management Behaviour: Exploring the Mediating Role of Digital Financial Literacy},

journal = {International Journal of Business and Economics Research},

volume = {15},

number = {3},

pages = {58-70},

doi = {10.11648/j.ijber.20261503.11},

url = {https://doi.org/10.11648/j.ijber.20261503.11},

eprint = {https://article.sciencepublishinggroup.com/pdf/10.11648.j.ijber.20261503.11},

abstract = {In the evolving landscape of the digital economy, both financial and digital literacy have become essential. This study investigates the mediating role of DFL in the relationship between financial attitude, financial socialisation, and personal financial management behaviour (PFMB) among working and non-working women in Punjab, India. Drawing on the Theory of Planned Behaviour, the research explores how psychological and social factors influence financial behaviour through the lens of digital competence. Using a structured questionnaire, data were collected from a representative sample of women across various districts in Punjab. The study employed Smart PLS 4.0 to examine direct and mediated relationships among the key constructs. The findings reveal that both financial attitude and financial socialisation significantly influence PFMB, and that DFL plays a partial mediating role in these relationships. Notably, working women exhibited higher levels of DFL and more proactive financial behaviours compared to their non-working counterparts. The results emphasise the importance of digital financial literacy as a critical enabler of financial empowerment for women, particularly in semi-urban and rural areas. This study contributes to the growing discourse on digital financial inclusion and offers practical implications for policymakers, educators, and financial institutions seeking to bridge gender and digital divides in financial access and decision-making.},

year = {2026}

}

TY - JOUR T1 - Impact of Financial Attitude and Financial Socialisation on Women’s Personal Financial Management Behaviour: Exploring the Mediating Role of Digital Financial Literacy AU - Kuldip Kaur Y1 - 2026/05/13 PY - 2026 N1 - https://doi.org/10.11648/j.ijber.20261503.11 DO - 10.11648/j.ijber.20261503.11 T2 - International Journal of Business and Economics Research JF - International Journal of Business and Economics Research JO - International Journal of Business and Economics Research SP - 58 EP - 70 PB - Science Publishing Group SN - 2328-756X UR - https://doi.org/10.11648/j.ijber.20261503.11 AB - In the evolving landscape of the digital economy, both financial and digital literacy have become essential. This study investigates the mediating role of DFL in the relationship between financial attitude, financial socialisation, and personal financial management behaviour (PFMB) among working and non-working women in Punjab, India. Drawing on the Theory of Planned Behaviour, the research explores how psychological and social factors influence financial behaviour through the lens of digital competence. Using a structured questionnaire, data were collected from a representative sample of women across various districts in Punjab. The study employed Smart PLS 4.0 to examine direct and mediated relationships among the key constructs. The findings reveal that both financial attitude and financial socialisation significantly influence PFMB, and that DFL plays a partial mediating role in these relationships. Notably, working women exhibited higher levels of DFL and more proactive financial behaviours compared to their non-working counterparts. The results emphasise the importance of digital financial literacy as a critical enabler of financial empowerment for women, particularly in semi-urban and rural areas. This study contributes to the growing discourse on digital financial inclusion and offers practical implications for policymakers, educators, and financial institutions seeking to bridge gender and digital divides in financial access and decision-making. VL - 15 IS - 3 ER -

Department of Commerce & Management, Panjab University, Chandigarh, India

Information