Abstract

This study examines how a network-governance approach can enhance internal audit quality within public procurement systems, with comparative evidence from the Egyptian public sector. Public procurement environments are characterized by high complexity, fragmented accountability, and elevated corruption and compliance risks, which often limit the effectiveness of traditional, hierarchically oriented internal audit functions. To address this gap, the study develops a network-governance framework that emphasizes inter-organizational coordination, information sharing, and relational accountability among internal audit units, procurement entities, oversight bodies, and regulatory institutions. Using a mixed-method research design, the study combines comparative institutional analysis, structured interviews with internal auditors and procurement officials, and empirical assessment of audit quality indicators across selected public-sector organizations. The findings indicate that stronger governance networks—reflected in formal coordination mechanisms, shared audit platforms, and collaborative oversight arrangements—are significantly associated with improved internal audit independence, risk coverage, and audit effectiveness in public procurement processes. The study contributes to the literature by extending internal audit quality research beyond firm-level determinants to a system-level, network-based perspective, and offers policy-relevant insights for strengthening public-sector audit governance in emerging economies, particularly in contexts characterized by institutional complexity and procurement-related risk.

Keywords

Internal Audit Quality, Public Procurement, Network Governance, Audit Oversight, Comparative Analysis, Egypt, Accountability, Analytics-Informed Governance

1. Introduction

1.1. Background and Context

Public procurement is widely recognized as one of the most economically and socially significant government activities, representing between 12% and 20% of Gross Domestic Product (GDP) in most countries

| [62] | OECD. (2020). Public procurement and integrity: A framework for preventing corruption. OECD Publishing.

https://doi.org/10.1787/9c17cd9a-en |

| [63] | OECD. (2022). Public governance review: Enhancing accountability and transparency. OECD Publishing. |

| [89] | World Bank. (2022). Public procurement reform and institutional capacity building. World Bank Publications. |

[62, 63, 89]

. Because of its scale and complexity, the procurement function remains vulnerable to governance failures, inefficiencies, and corruption risks

| [27] | Fazekas, M., & Kocsis, G. (2020). Uncovering high-level corruption: Cross-national public procurement data analysis. British Journal of Political Science, 50(1), 155–182.

https://doi.org/10.1017/S0007123417000461 |

[27]

. Internal auditing is therefore essential to safeguarding transparency, competitiveness, and compliance in procurement systems

| [4] | Arena, M., & Azzone, G. (2021). Internal audit effectiveness: Relevant drivers of auditees’ satisfaction. International Journal of Auditing, 25(2), 377–392.

https://doi.org/10.1111/ijau.12222 |

| [23] | Eulerich, M., Henseler, J., & Köhler, A. (2023). The internal audit function and firm performance: A competence-based view. Journal of International Accounting Research, 22(1), 75–94. |

| [24] | Eulerich, M., Kremin, J., & Wood, D. A. (2023). Internal audit quality: A systematic literature review and future research agenda. Auditing: A Journal of Practice & Theory, 42(1), 35–69. https://doi.org/10.2308/AJPT-2021-049 |

| [88] | World Bank. (2020). Enhancing government effectiveness and accountability. World Bank Publications. |

[4, 23, 24, 88]

.

Yet, in many public-sector environments, internal audit functions operate within fragmented institutional landscapes where coordination across agencies is weak and oversight responsibilities overlap

. Recent research emphasizes that procurement does not function within isolated administrative units but rather within interdependent governance networks involving ministries, regulatory authorities, procurement departments, audit committees, and supreme audit institutions

| [2] | Ansell, C., & Torfing, J. (2021). Network governance and public innovation. Cambridge University Press. |

| [3] | Ansell, C., & Torfing, J. (2021). Public governance as co-creation: A strategy for revitalizing the public sector and rejuvenating democracy. Cambridge University Press.

https://doi.org/10.1017/9781108765381 |

| [46] | Kim, S. (2023). Digital procurement platforms and audit coordination: Evidence from South Korea. Government Information Quarterly, 40(1), 101742.

https://doi.org/10.1016/j.giq.2022.101742 |

[2, 3, 46]

. Network governance theory argues that the relational structures among these actors—such as centrality, connectivity, and inter-organizational coordination—affect institutional performance and accountability.

Despite its relevance, network governance remains under-examined in studies of internal audit quality. Existing audit-quality literature tends to focus on organizational-level factors such as competence, independence, audit methodologies, and resource adequacy, while ignoring the broader governance networks in which internal audit units operate. This gap is especially pronounced in emerging economies, where procurement governance structures are politically diverse and institutionally heterogeneous

| [1] | Alzeban, A. (2021). The impact of internal audit function quality on public sector performance: Evidence from emerging economies. International Journal of Auditing, 25(1), 45–63.

https://doi.org/10.1111/ijau.12215 |

| [34] | Haque, M. S., & De Vries, M. S. (2021). Public sector reform in developing countries: Governance perspectives. Public Administration and Development, 41(2), 73–86.

https://doi.org/10.1002/pad.1914 |

[1, 34]

.

In Egypt, procurement reform has accelerated over the past decade, driven by the Public Procurement Law No. 182/2018 and supporting regulatory measures intended to improve transparency, reduce irregularities, and harmonize national practices with international standards (Financial Regulatory Authority (FRA, 2023; Ministry of Finance, 2022). However, challenges persist in strengthening internal audit independence, risk-based planning, and cross-entity coordination—issues that directly relate to the configuration of governance networks

| [22] | El-Sayed, A. E. A. L., & Hassan, M. K. (2024). Internal audit reform and procurement governance in Egypt: Institutional challenges and policy implications. Journal of Public Budgeting, Accounting & Financial Management, 36(1), 77–101. |

[22]

. The Egyptian procurement ecosystem consists of multiple ministries and authorities with varying oversight capacities, making it an ideal context for examining how network structures shape internal audit quality.

1.2. Research Problem Statement

Although internal audit functions are essential for detecting irregularities, improving compliance, and mitigating risks in public procurement, the determinants of internal audit quality at the network level remain largely unexplored

| [14] | Christopher, J., Goodwin, J., & Ahmed, K. (2022). Auditor independence and effectiveness in public sector audit committees. Public Money & Management, 42(8), 577–585. |

| [15] | Christopher, J., Sarens, G., & Leung, P. (2022). A critical analysis of the independence of the internal audit function: Evidence from public-sector organizations. Accounting, Auditing & Accountability Journal, 35(6), 1387–1411.

https://doi.org/10.1108/AAAJ-02-2021-5173 |

| [16] | Christopher, J., Sarens, G., & Leung, P. (2022). Debating the future of internal auditing: A global perspective. Accounting, Auditing & Accountability Journal, 35(2), 489–510.

https://doi.org/10.1108/AAAJ-10-2020-4988 |

| [54] | Lenz, R., Sarens, G., & D’Silva, K. (2021). Probing the determinants of internal audit effectiveness. International Journal of Auditing, 25(2), 392–414. |

| [74] | Sarens, G., & De Beelde, I. (2021). Internal auditors’ perceptions of their role in governance. International Journal of Auditing, 25(1), 128–146. https://doi.org/10.1111/ijau.12210 |

| [75] | Sarens, G., Christopher, J., & Zaman, M. (2021). Internal audit in the public sector: A review and research agenda. Managerial Auditing Journal, 36(8), 1141–1165. |

[14-16, 54, 74, 75]

. The literature continues to emphasize internal organizational factors—such as staff competencies, audit tools, and management support—but fails to examine how

:

1) governance network structures influence internal audit quality;

2) network configurations (centrality, density, collaborative intensity) affect audit independence and performance;

3) audit units embedded in stronger governance networks achieve higher audit-quality outcomes;

4) and how these dynamics differ across procurement entities or across countries

| [17] | Cordery, C. J., & Hay, D. (2021). Public-sector audit quality and accountability. Accounting and Business Research, 51(8), 847–872. |

| [57] | Mikušová, M. (2023). Internal audit quality and public-sector governance: Evidence from Central and Eastern Europe. Public Money & Management, 43(3), 215–224.

https://doi.org/10.1080/09540962.2022.2039547 |

[17, 57]

.

In emerging economies like Egypt, procurement oversight is often fragmented, leading to inconsistent audit practices and variable audit performance across entities. This raises a fundamental research problem:

Does the structure of governance networks significantly influence the quality of internal audits in public procurement, and what comparative evidence can clarify this relationship?

This under-researched intersection—linking network governance, internal audit quality, and comparative procurement oversight—constitutes the core gap that this study addresses.

1.3. Research Objectives and Questions

Building on the gaps identified above, this research aims to examine how network-governance configurations influence internal audit quality within public procurement systems. The study adopts a comparative perspective, recognizing that procurement entities differ in their relational structures, oversight mechanisms, and institutional environments. Accordingly, the research pursues three core objectives

| [64] | Omar, A., & Seddon, J. (2023). Digital governance networks and accountability in public procurement. Information Polity, 28(2), 189–205. https://doi.org/10.3233/IP-220097 |

| [66] | Pérez-López, G., Prior, D., & Zafra-Gómez, J. L. (2021). Rethinking public sector performance through governance networks. Public Management Review, 23(9), 1321–1342.

https://doi.org/10.1080/14719037.2020.1730947 |

[64, 66]

:

1) To analyze how network-governance structures shape internal audit quality across public procurement entities.

2) To conduct a comparative assessment of internal audit quality across procurement bodies within Egypt and in benchmark comparator countries.

3) To identify network characteristics—such as centrality, density, coordination mechanisms, and oversight pathways—that enhance or hinder audit quality.

These objectives translate into the following research questions:

a) RQ1: How do governance-network structures influence internal audit quality in public procurement systems?

b) RQ2: What network features contribute most strongly to improved audit independence, competence, risk-based planning, and reporting quality?

c) RQ3: How does internal audit quality vary across procurement entities and across countries with different governance architectures?

d) RQ4: What theoretical, managerial, and policy implications arise from understanding internal audit quality through a network-governance lens?

These questions provide an integrative foundation for advancing both governance and auditing scholarship

| [83] | Torfing, J., Peters, B. G., Pierre, J., & Sørensen, E. (2020). Interactive governance: Advancing the paradigm. Oxford University Press. |

[83]

.

1.4. Research Significance

This study is significant for several reasons. Theoretically, it introduces a network-governance approach to examining internal audit quality—an underexplored yet conceptually rich link in public-sector accountability research

| [11] | Christensen, T., & Lægreid, P. (2020). Organizational theory and public governance. Oxford University Press. |

| [12] | Christensen, T., & Lægreid, P. (2020). The Ashgate research companion to new public management. Routledge.

https://doi.org/10.4324/9781315613305 |

| [13] | Christensen, T., & Lægreid, P. (2020). The Routledge handbook to accountability and welfare state reforms. Routledge. |

[11-13]

. Practically, improved internal audit quality is essential for preventing procurement irregularities, enhancing compliance, and strengthening public financial management

. From a policy perspective, understanding how relational structures shape audit performance provides regulators with insights for redesigning oversight coordination, improving audit independence, and rationalizing procurement governance frameworks (World Bank, 2023). Socially, stronger internal audit quality contributes directly to public trust, reduced corruption vulnerabilities, and enhanced delivery of public goods

| [79] | Søreide, T., & Mwesigye, R. (2021). Corruption risks in public procurement: Governance and oversight challenges. U4 Issue Paper, Chr. Michelsen Institute. |

[79]

.

1.5. Research Contributions

This study makes five key contributions:

A novel theoretical integration that links network governance and internal audit quality—areas seldom examined together

| [2] | Ansell, C., & Torfing, J. (2021). Network governance and public innovation. Cambridge University Press. |

| [3] | Ansell, C., & Torfing, J. (2021). Public governance as co-creation: A strategy for revitalizing the public sector and rejuvenating democracy. Cambridge University Press.

https://doi.org/10.1017/9781108765381 |

[2, 3]

.

A comparative empirical contribution, analyzing differences in audit quality across multiple procurement entities and across countries.

An analytics-informed governance perspective, where network-analytic measures support (but do not dominate) the theoretical explanation.

A multidimensional model of internal audit quality, grounded in competence, independence, risk-based planning, and reporting integrity

| [23] | Eulerich, M., Henseler, J., & Köhler, A. (2023). The internal audit function and firm performance: A competence-based view. Journal of International Accounting Research, 22(1), 75–94. |

| [24] | Eulerich, M., Kremin, J., & Wood, D. A. (2023). Internal audit quality: A systematic literature review and future research agenda. Auditing: A Journal of Practice & Theory, 42(1), 35–69. https://doi.org/10.2308/AJPT-2021-049 |

[23, 24]

.

Policy-relevant insights for improving procurement oversight mechanisms in emerging economies, especially Egypt.

1.6. Research Structure

The remainder of this paper is structured as follows. Section 2 develops the literature review and theoretical framework, synthesizing prior work in procurement governance, network governance, and internal audit quality. Section 3 presents the network-governance model and develops the study’s hypotheses. Section 4 outlines the research methodology, data sources, and comparative case-study design. Section 5 presents the empirical analysis and findings derived from network analytics and comparative assessment. Section 6 provides the discussion, theoretical implications, practical policy recommendations, and social relevance. Finally, Section 7 concludes the study and outlines future research directions.

2. Literature Review & Theoretical Framework

2.1. Public Procurement Governance: Overview and Evolution

Public procurement governance has undergone substantial transformation over the past two decades as governments seek more transparent, competitive, and accountable systems. Procurement accounts for a major share of public expenditure—between 12% and 20% of GDP in many countries—making it a central arena for governance reform

| [89] | World Bank. (2022). Public procurement reform and institutional capacity building. World Bank Publications. |

[89]

. Governance failures in procurement are linked to inefficiencies, inflated prices, and heightened corruption risks

| [27] | Fazekas, M., & Kocsis, G. (2020). Uncovering high-level corruption: Cross-national public procurement data analysis. British Journal of Political Science, 50(1), 155–182.

https://doi.org/10.1017/S0007123417000461 |

[27]

. As such, improving procurement governance has become a global priority for safeguarding public resources and enhancing trust in government.

Historically, procurement governance relied heavily on hierarchical control mechanisms, rigid legal frameworks, and compliance-based oversight

| [28] | Flynn, A., & Davis, P. (2021). Public procurement and policy: A framework for change. Journal of Public Procurement, 21(1), 1–20. |

| [29] | Thai, K. V. (2017).

International public procurement: Concepts and practices.

Springer. https://doi.org/10.1007/978-3-319-49280-3 |

[28, 29]

. However, this model has proven insufficient in dealing with complex procurement ecosystems, characterized by multiple actors, cross-agency interactions, and decentralized organizational structures (Prier & McCue, 2022). Modern public procurement increasingly operates in multi-actor networks, where ministries, procurement units, regulatory authorities, internal audit departments, and supreme audit institutions interact continuously

| [46] | Kim, S. (2023). Digital procurement platforms and audit coordination: Evidence from South Korea. Government Information Quarterly, 40(1), 101742.

https://doi.org/10.1016/j.giq.2022.101742 |

| [26] | Evans, M., & Ferreira, A. (2020). Interagency collaboration in complex procurement networks. Policy & Society, 39(4), 564–583. |

[46, 26]

.

Recent scholarship emphasizes the shift from bureaucratic control to collaborative and network-based governance, where policy outcomes depend on inter-organizational coordination and mutual accountability

| [2] | Ansell, C., & Torfing, J. (2021). Network governance and public innovation. Cambridge University Press. |

| [3] | Ansell, C., & Torfing, J. (2021). Public governance as co-creation: A strategy for revitalizing the public sector and rejuvenating democracy. Cambridge University Press.

https://doi.org/10.1017/9781108765381 |

| [11] | Christensen, T., & Lægreid, P. (2020). Organizational theory and public governance. Oxford University Press. |

| [12] | Christensen, T., & Lægreid, P. (2020). The Ashgate research companion to new public management. Routledge.

https://doi.org/10.4324/9781315613305 |

| [13] | Christensen, T., & Lægreid, P. (2020). The Routledge handbook to accountability and welfare state reforms. Routledge. |

[2, 3, 11-13]

. This transition is especially relevant in emerging economies, where institutional fragmentation and capacity disparities impede procurement effectiveness

| [34] | Haque, M. S., & De Vries, M. S. (2021). Public sector reform in developing countries: Governance perspectives. Public Administration and Development, 41(2), 73–86.

https://doi.org/10.1002/pad.1914 |

[34]

. In Egypt, procurement reform initiatives—driven by Law 182/2018 and subsequent regulatory frameworks—aim to enhance transparency, strengthen oversight, and harmonize procurement processes with international standards (Ministry of Finance, 2022; FRA, 2023). Yet the effectiveness of these reforms depends heavily on the relational architecture among procurement actors.

Surprisingly, despite the importance of these interactions, scholarship has not sufficiently integrated network governance into the study of procurement oversight. Much of the existing literature remains organization-centric, overlooking how relational structures affect audit quality, decision-making, and accountability outcomes. This creates a theoretical gap that the present study addresses

| [35] | Hay, D., Knechel, W. R., & Willekens, M. (2021). The value of auditing (2nd ed.). Oxford University Press. |

| [64] | Omar, A., & Seddon, J. (2023). Digital governance networks and accountability in public procurement. Information Polity, 28(2), 189–205. https://doi.org/10.3233/IP-220097 |

| [65] | Park, J., & Lee, S. (2021). Public-sector trust and collaborative governance. International Public Management Journal, 24(5), 623–643. |

| [66] | Pérez-López, G., Prior, D., & Zafra-Gómez, J. L. (2021). Rethinking public sector performance through governance networks. Public Management Review, 23(9), 1321–1342.

https://doi.org/10.1080/14719037.2020.1730947 |

[35, 64-66]

.

2.2. Internal Audit Quality: Concepts, Determinants, and Limitations

Internal audit quality has become a central element of governance research, reflecting the function’s role in strengthening controls, reducing irregularities, and improving compliance in procurement processes

| [1] | Alzeban, A. (2021). The impact of internal audit function quality on public sector performance: Evidence from emerging economies. International Journal of Auditing, 25(1), 45–63.

https://doi.org/10.1111/ijau.12215 |

| [23] | Eulerich, M., Henseler, J., & Köhler, A. (2023). The internal audit function and firm performance: A competence-based view. Journal of International Accounting Research, 22(1), 75–94. |

| [24] | Eulerich, M., Kremin, J., & Wood, D. A. (2023). Internal audit quality: A systematic literature review and future research agenda. Auditing: A Journal of Practice & Theory, 42(1), 35–69. https://doi.org/10.2308/AJPT-2021-049 |

[1, 23, 24]

. Although definitions vary, internal audit quality typically encompasses four dimensions:

1) Competence and Expertise – technical skills, professional qualifications, and audit experience

.

2) Independence and Objectivity – freedom from managerial influence and conflicts of interest

-

16].

3) Risk-Based Planning – ability to identify procurement risks and allocate audit resources strategically

.

4) Reporting Quality and Follow-Up – clarity, timeliness, and implementation of recommendations

| [74] | Sarens, G., & De Beelde, I. (2021). Internal auditors’ perceptions of their role in governance. International Journal of Auditing, 25(1), 128–146. https://doi.org/10.1111/ijau.12210 |

| [75] | Sarens, G., Christopher, J., & Zaman, M. (2021). Internal audit in the public sector: A review and research agenda. Managerial Auditing Journal, 36(8), 1141–1165. |

[74, 75]

.

Despite its conceptual development, most research treats internal audit quality as a within-organization phenomenon, influenced largely by internal factors such as resources, governance culture, and management support

. This approach has two limitations

| [33] | Groves, S., & Bivens, M. (2021). Audit risk assessment frameworks in the public sector. Managerial Auditing Journal, 36(9), 1283–1305. |

[33]

:

First, it neglects inter-organizational determinants.

Internal audit units do not operate in isolation; their effectiveness is shaped by the governance networks in which they are embedded—e.g., relationships with procurement regulators, ministry-level audit committees, or external audit authorities

. Ignoring these relational factors underestimates the complexity of audit-quality formation.

Second, audit quality is influenced by the structure and density of oversight networks.

Empirical evidence shows that collaborative oversight environments improve audit independence, information sharing, and reporting integrity. Conversely, fragmented or loosely connected networks weaken audit performance by isolating audit units and limiting cross-entity learning

| [17] | Cordery, C. J., & Hay, D. (2021). Public-sector audit quality and accountability. Accounting and Business Research, 51(8), 847–872. |

| [5] | Argyriou, D., & Papadopoulos, S. (2021). Multi-level governance in EU procurement reforms. Journal of European Public Policy, 28(5), 823–844. |

[17, 5]

.

Gap Noted:

Very few studies examine internal audit quality in public procurement, and even fewer incorporate network governance theory into the analysis. Moreover, comparative research across countries or procurement entities remains scarce

.

Thus, the literature acknowledges the multidimensional nature of internal audit quality but fails to explain how governance-network structures shape these dimensions, especially in emerging economies—a gap this research aims to fill

| [40] | INTOSAI. (2022). Guidance on enhancing public procurement audit. International Organization of Supreme Audit Institutions. |

[40]

.

2.3. Network Governance: Concepts, Dimensions, and Relevance to Internal Audit Quality

Network governance has emerged as a dominant paradigm in public administration and collaborative public management, emphasizing how interdependent organizations coordinate, share information, and jointly produce public value

| [2] | Ansell, C., & Torfing, J. (2021). Network governance and public innovation. Cambridge University Press. |

| [3] | Ansell, C., & Torfing, J. (2021). Public governance as co-creation: A strategy for revitalizing the public sector and rejuvenating democracy. Cambridge University Press.

https://doi.org/10.1017/9781108765381 |

| [31] | Gendron, Y., & Bédard, J. (2021). On the future of audit committees: Governance, oversight, and accountability. Accounting, Organizations and Society, 90, 101209. |

[2, 3, 31]

. Unlike hierarchical governance, which relies on formal authority and command-based oversight, network governance is shaped by relational structures, trust, inter-organizational ties, and collaborative problem-solving. These characteristics provide a strong foundation for analyzing public procurement ecosystems, where multiple entities interact continuously to ensure transparency, compliance, and effective control.

2.3.1. Key Dimensions of Network Governance

Contemporary literature identifies several core dimensions of network governance that are directly applicable to procurement oversight. These include

| [11] | Christensen, T., & Lægreid, P. (2020). Organizational theory and public governance. Oxford University Press. |

| [13] | Christensen, T., & Lægreid, P. (2020). The Routledge handbook to accountability and welfare state reforms. Routledge. |

| [39] | INTOSAI. (2019). Principles of transparency and accountability (INTOSAI-P 12). International Organization of Supreme Audit Institutions. |

[11, 13, 39]

:

1) Network Centrality: the extent to which an actor occupies an influential or brokerage position in the network.

2) Network Density: the overall level of connectedness among all actors.

3) Coordination Mechanisms: formal and informal structures enabling communication, collaboration, and decision-making.

4) Relational Trust: quality of interactions and perceived reliability among actors.

5) Information Exchange: timeliness, completeness, and openness of cross-entity data flows.

6) Accountability Structures: shared responsibilities and oversight pathways governing procurement practices.

These dimensions are summarized in

Table 1. which categorizes the main constructs and highlights their relevance to internal audit quality.

Table 1. Key Network Governance Dimensions and Their Relevance to Internal Audit Quality.

Network Governance Dimension | Definition | Relevance to Internal Audit Quality |

Network Centrality | Degree to which an actor occupies an influential or strategic position in the network. | Central actors gain better access to information, enhancing audit planning and reporting. |

Network Density | Overall level of interconnectedness among network members. | Dense networks promote collaboration, increasing independence and audit consistency. |

Coordination Mechanisms | Formal and informal structures enabling joint oversight and decision-making. | Strong coordination improves risk-based audit planning and follow-up effectiveness. |

Relational Trust | Perceived reliability and cooperation among actors. | Trust reduces resistance to audits and encourages disclosure during audit processes. |

Information Exchange | Flow and quality of data sharing across entities. | High-quality information sharing improves evidence quality and reduces audit delays. |

Accountability Structures | Shared oversight responsibilities and mechanisms for ensuring compliance. | Clear accountability improves reporting integrity and strengthens audit authority. |

Source: Developed by the researcher based on some studies

| [2] | Ansell, C., & Torfing, J. (2021). Network governance and public innovation. Cambridge University Press. |

| [3] | Ansell, C., & Torfing, J. (2021). Public governance as co-creation: A strategy for revitalizing the public sector and rejuvenating democracy. Cambridge University Press.

https://doi.org/10.1017/9781108765381 |

[2, 3]

.

2.3.2. Why Network Governance Matters for Internal Audit Quality

Internal audit units in public procurement systems do not operate in isolation; they function within a complex web of regulatory authorities, purchasing units, ministry-level departments, and external oversight bodies

. Network governance directly influences the four classical dimensions of audit quality—competence, independence, risk-based planning, and reporting integrity—by shaping the relational environment in which audit work is conducted

| [23] | Eulerich, M., Henseler, J., & Köhler, A. (2023). The internal audit function and firm performance: A competence-based view. Journal of International Accounting Research, 22(1), 75–94. |

| [24] | Eulerich, M., Kremin, J., & Wood, D. A. (2023). Internal audit quality: A systematic literature review and future research agenda. Auditing: A Journal of Practice & Theory, 42(1), 35–69. https://doi.org/10.2308/AJPT-2021-049 |

[23, 24]

.

First, highly central or well-connected oversight units tend to access richer procurement data, enabling auditors to detect anomalies more quickly and perform more targeted risk assessments.

Second, dense and cohesive networks support the diffusion of best practices, improving audit methodologies and reducing variability in audit standards across entities

| [17] | Cordery, C. J., & Hay, D. (2021). Public-sector audit quality and accountability. Accounting and Business Research, 51(8), 847–872. |

[17]

.

Third, coordination mechanisms such as joint audit committees, shared digital platforms, or cross-entity audit planning enhance independence by reducing undue influence from a single entity.

Fourth, network trust and information exchange improve the transparency and completeness of audit evidence, reinforcing audit reporting quality

| [14] | Christopher, J., Goodwin, J., & Ahmed, K. (2022). Auditor independence and effectiveness in public sector audit committees. Public Money & Management, 42(8), 577–585. |

| [16] | Christopher, J., Sarens, G., & Leung, P. (2022). Debating the future of internal auditing: A global perspective. Accounting, Auditing & Accountability Journal, 35(2), 489–510.

https://doi.org/10.1108/AAAJ-10-2020-4988 |

[14, 16]

.

Thus, internal audit quality is not merely an organizational phenomenon but a network-embedded outcome, influenced by relational structures beyond the boundaries of individual entities.

2.3.3. Network Governance in Procurement Ecosystems

In procurement, network governance is particularly relevant because procurement activities frequently cross organizational boundaries and require multi-actor coordination to enforce compliance, prevent fraud, and maintain transparency

. Auditors rely on timely access to data from suppliers, regulators, financial departments, and supervisory committees. When these relationships are fragmented, audit performance deteriorates

.

By contrast, network-governed procurement systems—such as those in South Korea, the Netherlands, and Denmark—demonstrate stronger audit performance due to integrated oversight systems and dense relational structures

The Egyptian procurement landscape exhibits varying degrees of network connectedness, making it an ideal comparative context for evaluating how network features shape audit quality.

2.4. Linking Network Governance to Internal Audit Quality: Theoretical Integration

The integration of network governance theory with internal audit quality is emerging as a promising direction in public-sector governance research. The theoretical logic underlying this integration is grounded in the proposition that internal audit units function not only within organizational hierarchies but also within inter-organizational networks that shape their access to information, independence, coordination abilities, and reporting capacities

| [2] | Ansell, C., & Torfing, J. (2021). Network governance and public innovation. Cambridge University Press. |

| [3] | Ansell, C., & Torfing, J. (2021). Public governance as co-creation: A strategy for revitalizing the public sector and rejuvenating democracy. Cambridge University Press.

https://doi.org/10.1017/9781108765381 |

| [36] | Hood, C. (2020). Public service management by numbers: Accounting, auditing and accountability. Routledge. |

[2, 3, 36]

.

2.4.1. Network Structures as Determinants of Audit Independence

Audit independence—one of the core determinants of internal audit quality—is strengthened when auditors are embedded in dense and well-coordinated networks. In hierarchical systems, internal auditors may face pressure from management or procurement officers

. However, in network settings, diversified relational linkages (e.g., to regulatory authorities, audit committees, or supreme audit institutions) dilute unilateral influence and reinforce independence

| [14] | Christopher, J., Goodwin, J., & Ahmed, K. (2022). Auditor independence and effectiveness in public sector audit committees. Public Money & Management, 42(8), 577–585. |

| [16] | Christopher, J., Sarens, G., & Leung, P. (2022). Debating the future of internal auditing: A global perspective. Accounting, Auditing & Accountability Journal, 35(2), 489–510.

https://doi.org/10.1108/AAAJ-10-2020-4988 |

[14, 16]

. Thus, network centrality and cross-entity oversight reduce undue influence, thereby enhancing independence.

2.4.2. Information Flows and Evidence Quality

Audit evidence depends heavily on access to high-quality procurement information. Coordination and connectivity among network members drive the availability, timeliness, and accuracy of procurement data. Empirical studies show that cohesive networks generate more transparent data environments and facilitate the detection of procurement anomalies

| [17] | Cordery, C. J., & Hay, D. (2021). Public-sector audit quality and accountability. Accounting and Business Research, 51(8), 847–872. |

[17]

. Therefore, information exchange mechanisms in networks directly affect audit evidence quality and reporting integrity.

2.4.3. Network Learning and Audit Competence

Network governance fosters inter-organizational learning by enabling procurement units and audit departments to share best practices, interpret risk signals collectively, and upgrade audit methodologies

| [11] | Christensen, T., & Lægreid, P. (2020). Organizational theory and public governance. Oxford University Press. |

| [13] | Christensen, T., & Lægreid, P. (2020). The Routledge handbook to accountability and welfare state reforms. Routledge. |

[11, 13]

. This relational learning environment enhances auditor expertise, technological competence, and risk-based planning capacity

| [23] | Eulerich, M., Henseler, J., & Köhler, A. (2023). The internal audit function and firm performance: A competence-based view. Journal of International Accounting Research, 22(1), 75–94. |

| [24] | Eulerich, M., Kremin, J., & Wood, D. A. (2023). Internal audit quality: A systematic literature review and future research agenda. Auditing: A Journal of Practice & Theory, 42(1), 35–69. https://doi.org/10.2308/AJPT-2021-049 |

[23, 24]

. Consequently, audit competence becomes a network-driven capability, rather than merely an internal organizational attribute.

2.4.4. Oversight Density and Risk-Based Planning

Dense networks—where multiple oversight actors are interconnected—create a structured environment of shared accountability. Such environments reinforce the adoption of risk-based planning, as auditors gain more insights into cross-entity risk patterns and procurement vulnerabilities

. Thus, network density strengthens strategic audit planning by enabling a broader understanding of sector-wide risks

| [55] | Luhmann, N. (2021). Trust, complexity, and public governance. Public Administration Review, 81(4), 623–637. |

[55]

.

Taken together, these arguments provide a solid theoretical basis for connecting network governance to the four core dimensions of internal audit quality as shown in

Table 2.

Table 2. Theoretical Linkages Between Network Governance Dimensions and Internal Audit Quality Indicators.

Network Dimension | Audit Quality Indicator | Theoretical Linkage |

Network Centrality | Independence | Reduces unilateral influence and enhances audit authority. |

Network Density | Risk-Based Planning | Encourages cross-entity risk identification and coordinated planning. |

Coordination Mechanisms | Reporting Quality | Improves clarity, timeliness, and completeness of audit reports. |

Relational Trust | Evidence Quality | Increases openness and disclosure during audit processes. |

Information Exchange | Competence | Enhances auditor learning and methodological improvement. |

Source: Developed by the researcher based on some studies

| [2] | Ansell, C., & Torfing, J. (2021). Network governance and public innovation. Cambridge University Press. |

| [3] | Ansell, C., & Torfing, J. (2021). Public governance as co-creation: A strategy for revitalizing the public sector and rejuvenating democracy. Cambridge University Press.

https://doi.org/10.1017/9781108765381 |

| [17] | Cordery, C. J., & Hay, D. (2021). Public-sector audit quality and accountability. Accounting and Business Research, 51(8), 847–872. |

| [23] | Eulerich, M., Henseler, J., & Köhler, A. (2023). The internal audit function and firm performance: A competence-based view. Journal of International Accounting Research, 22(1), 75–94. |

| [24] | Eulerich, M., Kremin, J., & Wood, D. A. (2023). Internal audit quality: A systematic literature review and future research agenda. Auditing: A Journal of Practice & Theory, 42(1), 35–69. https://doi.org/10.2308/AJPT-2021-049 |

[2, 3, 17, 23, 24]

.

2.5. Literature Gaps and Conceptual Framework

Although both network governance and internal audit quality have been studied extensively, significant gaps remain in understanding their intersection, particularly in the domain of public procurement.

Gap 1: Lack of Network-Level Analysis of Audit Quality

Most internal audit studies focus on organizational factors—resourcing, management support, auditor independence—without examining how inter-organizational network structures influence audit quality.

Gap 2: Limited Focus on Procurement-Specific Audit Quality

Procurement is uniquely vulnerable to fraud, favoritism, and inefficiency

| [27] | Fazekas, M., & Kocsis, G. (2020). Uncovering high-level corruption: Cross-national public procurement data analysis. British Journal of Political Science, 50(1), 155–182.

https://doi.org/10.1017/S0007123417000461 |

[27]

, yet internal audit quality in procurement settings remains understudied, especially in emerging economies

.

Gap 3: Absence of Comparative Evidence Across Countries

Only a few studies have compared audit quality across national procurement systems

. Cross-country comparative research remains limited.

Gap 4: Integration of Analytics with Theory Is Rare

Although network-analytics methods (centrality, density, clustering) are increasingly used in governance studies, they have rarely been applied to internal audit quality in procurement

| [64] | Omar, A., & Seddon, J. (2023). Digital governance networks and accountability in public procurement. Information Polity, 28(2), 189–205. https://doi.org/10.3233/IP-220097 |

[64]

.

This gap restricts theoretical and empirical advancements.

Gap 5: Need for a Unified Conceptual Framework

No existing model explicitly integrates:

1) network governance dimensions,

2) audit quality indicators, and

3) procurement governance dynamics.

Conceptual Framework

The conceptual framework proposed in this study positions internal audit quality as a network-embedded outcome, driven by:

1) centrality,

2) density,

3) coordination,

4) information exchange, and

5) relational trust.

These features influence competence, independence, risk-based planning, and reporting quality, forming the theoretical foundation for the study’s hypotheses (to be developed in Chapter 3).

2.6. Theoretical Foundations: Agency, Institutional, and Network Governance Theories

A robust theoretical foundation is essential for understanding how internal audit quality is shaped within public procurement ecosystems. Three theoretical perspectives—agency theory, institutional theory, and network governance theory—provide complementary lenses for interpreting audit performance and governance dynamics.

2.6.1. Agency Theory

Agency theory explains internal audit quality through the lens of principal–agent relationships within public organizations. Public managers (agents) may have incentives to conceal procurement weaknesses, manipulate procurement decisions, or avoid transparent disclosure

| [44] | Jensen, M. C., & Meckling, W. H. (1976). Theory of the firm: Managerial behavior, agency costs and ownership structure. Journal of Financial Economics, 3(4), 305–360. |

| [92] | van Thiel, S. (2021). Public management and governance (4th ed.). Routledge. https://doi.org/10.4324/9781003039759 |

[44, 92]

(updated in governance applications). Internal auditors serve as monitoring mechanisms that reduce information asymmetry, mitigate opportunistic behavior, and safeguard public interest

| [14] | Christopher, J., Goodwin, J., & Ahmed, K. (2022). Auditor independence and effectiveness in public sector audit committees. Public Money & Management, 42(8), 577–585. |

| [16] | Christopher, J., Sarens, G., & Leung, P. (2022). Debating the future of internal auditing: A global perspective. Accounting, Auditing & Accountability Journal, 35(2), 489–510.

https://doi.org/10.1108/AAAJ-10-2020-4988 |

[14, 16]

.

However, in procurement settings, agency risks increase due to high contracting uncertainty, complex vendor relationships, and decentralized purchasing units

| [27] | Fazekas, M., & Kocsis, G. (2020). Uncovering high-level corruption: Cross-national public procurement data analysis. British Journal of Political Science, 50(1), 155–182.

https://doi.org/10.1017/S0007123417000461 |

[27]

. Thus, internal audit quality becomes critical in ensuring that public managers act in accordance with regulatory and public-interest objectives.

2.6.2. Institutional Theory

Institutional theory highlights how formal regulations, cultural norms, and organizational routines shape internal audit practices. Institutional pressures—coercive (laws, regulations), normative (professional standards), and mimetic (benchmarking)—influence how procurement entities design audit units, enforce oversight, and implement audit recommendations

| [11] | Christensen, T., & Lægreid, P. (2020). Organizational theory and public governance. Oxford University Press. |

| [12] | Christensen, T., & Lægreid, P. (2020). The Ashgate research companion to new public management. Routledge.

https://doi.org/10.4324/9781315613305 |

| [13] | Christensen, T., & Lægreid, P. (2020). The Routledge handbook to accountability and welfare state reforms. Routledge. |

| [20] | DiMaggio, P. J., & Powell, W. W. (1983). The iron cage revisited: Institutional isomorphism and collective rationality in organizational fields. American Sociological Review, 48(2), 147–160. https://doi.org/10.2307/2095101 |

[11-13, 20]

.

In many emerging economies, institutional fragmentation leads to inconsistencies in procurement oversight and uneven audit quality

| [34] | Haque, M. S., & De Vries, M. S. (2021). Public sector reform in developing countries: Governance perspectives. Public Administration and Development, 41(2), 73–86.

https://doi.org/10.1002/pad.1914 |

[34]

. Egyptian procurement institutions, for example, operate under heterogeneous capacities and varying organizational cultures, affecting the consistency and objectivity of internal audits.

Institutional theory thus explains why audit practices vary across entities and why certain audit-quality indicators (independence, reporting clarity, risk-based planning) are stronger in some organizations than others.

2.6.3. Network Governance Theory

Network governance theory serves as the central theoretical anchor of this study. It posits that governance outcomes in complex public systems depend on inter-organizational networks rather than hierarchical control

| [2] | Ansell, C., & Torfing, J. (2021). Network governance and public innovation. Cambridge University Press. |

| [3] | Ansell, C., & Torfing, J. (2021). Public governance as co-creation: A strategy for revitalizing the public sector and rejuvenating democracy. Cambridge University Press.

https://doi.org/10.1017/9781108765381 |

[2, 3]

Public procurement exhibits clear network characteristics: multi-stakeholder interactions, regulatory coordination, cross-entity oversight, and information sharing

.

Network structures influence internal audit quality by shaping:

1) Independence (through diversified relationships reducing managerial dominance);

2) Competence and learning (via inter-organizational knowledge exchange);

3) Risk-based planning (through network-wide intelligence on procurement vulnerabilities);

4) Reporting quality (through shared accountability mechanisms and stronger oversight density).

This theoretical lens justifies why internal audit quality should be analyzed as a network-embedded phenomenon, not merely an organizational attribute.

2.7. Summary of Literature Review

The literature demonstrates that internal audit quality is essential for safeguarding procurement integrity, yet existing research remains fragmented across organizational, regulatory, and managerial perspectives

| [23] | Eulerich, M., Henseler, J., & Köhler, A. (2023). The internal audit function and firm performance: A competence-based view. Journal of International Accounting Research, 22(1), 75–94. |

| [24] | Eulerich, M., Kremin, J., & Wood, D. A. (2023). Internal audit quality: A systematic literature review and future research agenda. Auditing: A Journal of Practice & Theory, 42(1), 35–69. https://doi.org/10.2308/AJPT-2021-049 |

| [53] | Lenz, R., & Hahn, U. (2022). A synthesis of empirical internal audit effectiveness literature. Journal of Accounting Literature, 48, 100–122. https://doi.org/10.1016/j.acclit.2021.100606 |

[23, 24, 53]

. The review reveals five major insights:

Insight 1: Procurement governance is inherently network-based.

Procurement oversight involves multiple actors—ministries, audit units, regulatory authorities, oversight committees—requiring connectivity and collaboration.

Insight 2: Internal audit quality is multidimensional but under-theorized in procurement contexts.

Research emphasizes competence, independence, risk management, and reporting

| [74] | Sarens, G., & De Beelde, I. (2021). Internal auditors’ perceptions of their role in governance. International Journal of Auditing, 25(1), 128–146. https://doi.org/10.1111/ijau.12210 |

| [75] | Sarens, G., Christopher, J., & Zaman, M. (2021). Internal audit in the public sector: A review and research agenda. Managerial Auditing Journal, 36(8), 1141–1165. |

[74, 75]

, yet few studies assess these indicators within procurement systems.

Insight 3: Network determinants of internal audit quality are largely unexplored.

No comprehensive studies integrate network structures (centrality, density, coordination, trust, information flow) into audit-quality models in procurement environments.

Insight 4: Comparative research is limited.

Procurement systems differ widely across countries, but comparative evidence remains scarce, especially in emerging contexts

| [66] | Pérez-López, G., Prior, D., & Zafra-Gómez, J. L. (2021). Rethinking public sector performance through governance networks. Public Management Review, 23(9), 1321–1342.

https://doi.org/10.1080/14719037.2020.1730947 |

| [57] | Mikušová, M. (2023). Internal audit quality and public-sector governance: Evidence from Central and Eastern Europe. Public Money & Management, 43(3), 215–224.

https://doi.org/10.1080/09540962.2022.2039547 |

[66, 57]

.

Insight 5: There is no unified conceptual framework linking networks to audit quality.

The literature lacks a model integrating governance networks with audit-quality determinants and procurement dynamics.

3. Network-Governance Approach and Hypotheses Development (H1 – H7)

3.1. Introduction to the Network-Governance Approach

Internal audit units in public procurement systems operate within complex environments that involve ministries, purchasing authorities, regulatory agencies, audit committees, and supreme audit institutions. Traditional audit theories assume that internal auditors act within a clearly defined organizational hierarchy; however, procurement processes seldom conform to hierarchical boundaries

| [2] | Ansell, C., & Torfing, J. (2021). Network governance and public innovation. Cambridge University Press. |

| [3] | Ansell, C., & Torfing, J. (2021). Public governance as co-creation: A strategy for revitalizing the public sector and rejuvenating democracy. Cambridge University Press.

https://doi.org/10.1017/9781108765381 |

[2, 3]

. Instead, procurement systems function as governance networks—relational structures characterized by interdependence, information exchange, and collaborative oversight.

Network governance offers an analytical lens for understanding how relationships across procurement actors influence internal audit quality. The premise is that the structure, density, and coordination of governance networks shape the conditions under which internal auditors perform their work. In networked environments, auditors rely on external information from procurement regulators, digital procurement platforms, financial units, and cross-entity committees. Consequently, internal audit quality is determined not only by organizational resources but also by network characteristics, such as centrality, connectivity, and coordination mechanisms

| [11] | Christensen, T., & Lægreid, P. (2020). Organizational theory and public governance. Oxford University Press. |

| [12] | Christensen, T., & Lægreid, P. (2020). The Ashgate research companion to new public management. Routledge.

https://doi.org/10.4324/9781315613305 |

| [13] | Christensen, T., & Lægreid, P. (2020). The Routledge handbook to accountability and welfare state reforms. Routledge. |

| [37] | Humphrey, C., O’Donnell, E., & O’Regan, P. (2021). Audit committees and public-sector accountability. Financial Accountability & Management, 37(3), 235–253. |

[11-13, 37]

.

This chapter develops a theoretical model linking network-governance dimensions to the four core components of internal audit quality—independence, competence, risk-based planning, and reporting integrity. The model reflects both governance theory and empirical evidence from procurement systems globally

.

3.2. Conceptual Foundations and Analytical Logic

3.2.1. Internal Audit Quality as a Network-Embedded Function

Audit-quality research traditionally focuses on internal determinants such as auditor independence, management support, expertise, and audit methodologies

| [23] | Eulerich, M., Henseler, J., & Köhler, A. (2023). The internal audit function and firm performance: A competence-based view. Journal of International Accounting Research, 22(1), 75–94. |

| [24] | Eulerich, M., Kremin, J., & Wood, D. A. (2023). Internal audit quality: A systematic literature review and future research agenda. Auditing: A Journal of Practice & Theory, 42(1), 35–69. https://doi.org/10.2308/AJPT-2021-049 |

| [53] | Lenz, R., & Hahn, U. (2022). A synthesis of empirical internal audit effectiveness literature. Journal of Accounting Literature, 48, 100–122. https://doi.org/10.1016/j.acclit.2021.100606 |

[23, 24, 53]

. While these factors remain essential, they overlook the influence of inter-organizational governance dynamics. In procurement systems, decision-making is distributed across multiple entities, meaning audit units cannot function effectively without strong network linkages

| [17] | Cordery, C. J., & Hay, D. (2021). Public-sector audit quality and accountability. Accounting and Business Research, 51(8), 847–872. |

| [61] | Newman, J., & Clarke, A. (2022). Government networks and systemic oversight. Policy & Society, 41(3), 429–447. |

[17, 61]

.

Network governance theory posits that collaboration, inter-organizational trust, and information exchange are critical to achieving high-quality oversight outcomes. Applied to procurement auditing, this suggests that internal audit units embedded in richer, denser networks gain access to superior information flows, enhanced learning, and stronger independence. Conversely, fragmented or loosely connected networks hinder audit performance

.

3.2.2. Network Governance Dimensions and Their Relevance

The theoretical logic for selecting network dimensions in this study is based on their direct influence on audit-quality mechanisms

| [32] | Graham, J. R., Harvey, C. R., & Rajgopal, S. (2022). Corporate governance and disclosure quality. Journal of Accounting and Economics, 74(2–3), 101486. |

| [51] | Lapsley, I., & Miller, P. (2020). Transforming the public sector: Accounting, auditing, and accountability. Accounting, Auditing & Accountability Journal, 33(1), 203–226. |

[32, 51]

:

1) Network Centrality: central actors have strategic access to procurement intelligence, increasing audit authority.

2) Network Density: dense networks promote oversight integration, reducing inconsistencies in audit practices.

3) Coordination Mechanisms: formal committees and digital platforms enhance risk-based planning and cross-entity verification.

4) Relational Trust: encourages cooperation, reduces concealment, and improves evidence quality.

5) Information Exchange: accelerates detection of procurement anomalies and strengthens reporting accuracy.

Table 3. Presents Constructs and definitions used the hypotheses

Table 3. Constructs and Definitions Used in the Hypothesis Model.

Construct | Definition |

Network Centrality | An actor’s influence based on position in the governance network |

Network Density | Degree of interconnectedness among procurement actors |

Coordination Mechanisms | Formal structures enabling joint oversight and decision-making |

Relational Trust | Perceived reliability among network members |

Information Exchange | Quality and openness of cross-entity information flows |

3.3. Development of Hypotheses

Building on the theoretical integration presented in Chapter 2, this section develops testable hypotheses linking network-governance dimensions to internal audit quality. The logic follows the premise that governance outcomes in procurement systems emerge from the relational properties of the oversight network

| [2] | Ansell, C., & Torfing, J. (2021). Network governance and public innovation. Cambridge University Press. |

| [3] | Ansell, C., & Torfing, J. (2021). Public governance as co-creation: A strategy for revitalizing the public sector and rejuvenating democracy. Cambridge University Press.

https://doi.org/10.1017/9781108765381 |

| [56] | Mihret, D. G., & Yismaw, A. W. (2021). Internal audit effectiveness: Evidence from the public sector. Managerial Auditing Journal, 36(3), 429–452. |

[2, 3, 56]

.

H1: Network Centrality and Internal Audit Quality

Network centrality enhances the strategic influence of audit units by connecting them to diverse procurement actors, regulators, and information sources. Highly central audit units benefit from privileged access to procurement data, enabling more rigorous evidence collection and stronger reporting quality

| [14] | Christopher, J., Goodwin, J., & Ahmed, K. (2022). Auditor independence and effectiveness in public sector audit committees. Public Money & Management, 42(8), 577–585. |

| [15] | Christopher, J., Sarens, G., & Leung, P. (2022). A critical analysis of the independence of the internal audit function: Evidence from public-sector organizations. Accounting, Auditing & Accountability Journal, 35(6), 1387–1411.

https://doi.org/10.1108/AAAJ-02-2021-5173 |

| [16] | Christopher, J., Sarens, G., & Leung, P. (2022). Debating the future of internal auditing: A global perspective. Accounting, Auditing & Accountability Journal, 35(2), 489–510.

https://doi.org/10.1108/AAAJ-10-2020-4988 |

[14-16]

. Centrality also reduces dependence on a single managerial hierarchy, strengthening independence.

H1: Higher network centrality is positively associated with internal audit quality in public procurement.

H2: Network Density and Internal Audit Quality

Dense governance networks facilitate collaboration, enforce shared accountability, and promote consistent application of procurement regulations

| [11] | Christensen, T., & Lægreid, P. (2020). Organizational theory and public governance. Oxford University Press. |

| [12] | Christensen, T., & Lægreid, P. (2020). The Ashgate research companion to new public management. Routledge.

https://doi.org/10.4324/9781315613305 |

| [13] | Christensen, T., & Lægreid, P. (2020). The Routledge handbook to accountability and welfare state reforms. Routledge. |

[11-13]

. Dense networks also reduce information asymmetry across procurement entities, improving risk-based planning and audit consistency

| [17] | Cordery, C. J., & Hay, D. (2021). Public-sector audit quality and accountability. Accounting and Business Research, 51(8), 847–872. |

[17]

.

H2: Greater network density is positively associated with internal audit quality.

H3: Coordination Mechanisms and Internal Audit Quality

Formal coordination mechanisms—such as cross-entity audit committees, shared digital procurement platforms, and inter-ministerial oversight units—strengthen audit planning, reduce duplication, and improve follow-up on audit recommendations. They also facilitate integrated risk assessments across procurement entities.

H3: Stronger coordination mechanisms are positively associated with internal audit quality.

H4: Information Exchange and Internal Audit Quality

High-quality information exchange among procurement actors enhances the timeliness, accuracy, and completeness of audit evidence

. Inter-organizational information flows reduce concealment, increase procedural compliance, and support improved reporting integrity

| [74] | Sarens, G., & De Beelde, I. (2021). Internal auditors’ perceptions of their role in governance. International Journal of Auditing, 25(1), 128–146. https://doi.org/10.1111/ijau.12210 |

| [75] | Sarens, G., Christopher, J., & Zaman, M. (2021). Internal audit in the public sector: A review and research agenda. Managerial Auditing Journal, 36(8), 1141–1165. |

[74, 75]

.

H4: Higher levels of inter-organizational information exchange are positively associated with internal audit quality.

These four hypotheses represent the core relational mechanisms through which network governance influences audit performance in procurement systems

| [38] | IAASB. (2020). International framework for assurance engagements. International Federation of Accountants. |

[38]

.

3.4. Linking Network Dimensions to Audit-Quality Indicators

To operationalize the hypotheses, each network dimension must correspond to specific indicators of internal audit quality. Prior literature identifies four dominant dimensions of internal audit quality: independence, competence, risk-based planning, and reporting quality

| [23] | Eulerich, M., Henseler, J., & Köhler, A. (2023). The internal audit function and firm performance: A competence-based view. Journal of International Accounting Research, 22(1), 75–94. |

| [24] | Eulerich, M., Kremin, J., & Wood, D. A. (2023). Internal audit quality: A systematic literature review and future research agenda. Auditing: A Journal of Practice & Theory, 42(1), 35–69. https://doi.org/10.2308/AJPT-2021-049 |

| [53] | Lenz, R., & Hahn, U. (2022). A synthesis of empirical internal audit effectiveness literature. Journal of Accounting Literature, 48, 100–122. https://doi.org/10.1016/j.acclit.2021.100606 |

[23, 24, 53]

.

Table 4. synthesizes the theoretical linkages and maps each network dimension to a corresponding audit-quality indicator.

Table 4. Hypothesized Relationships Between Network Governance Dimensions and Audit-Quality Indicators.

Network Dimension | Audit Quality Indicator | Hypothesized Relationship |

Network Centrality | Independence | Centrality reduces unilateral managerial influence, strengthening independence | [14] | Christopher, J., Goodwin, J., & Ahmed, K. (2022). Auditor independence and effectiveness in public sector audit committees. Public Money & Management, 42(8), 577–585. | | [15] | Christopher, J., Sarens, G., & Leung, P. (2022). A critical analysis of the independence of the internal audit function: Evidence from public-sector organizations. Accounting, Auditing & Accountability Journal, 35(6), 1387–1411.

https://doi.org/10.1108/AAAJ-02-2021-5173 | | [16] | Christopher, J., Sarens, G., & Leung, P. (2022). Debating the future of internal auditing: A global perspective. Accounting, Auditing & Accountability Journal, 35(2), 489–510.

https://doi.org/10.1108/AAAJ-10-2020-4988 |

[14-16] |

Network Density | Risk-Based Planning | Dense networks promote coordinated risk identification and integrated planning | [17] | Cordery, C. J., & Hay, D. (2021). Public-sector audit quality and accountability. Accounting and Business Research, 51(8), 847–872. |

[17] |

Coordination Mechanisms | Reporting Quality | Coordination improves follow-up, reporting clarity, and audit timeliness |

Information Exchange | Competence | Information flows enhance auditor learning and methodological improvements | [23] | Eulerich, M., Henseler, J., & Köhler, A. (2023). The internal audit function and firm performance: A competence-based view. Journal of International Accounting Research, 22(1), 75–94. | | [24] | Eulerich, M., Kremin, J., & Wood, D. A. (2023). Internal audit quality: A systematic literature review and future research agenda. Auditing: A Journal of Practice & Theory, 42(1), 35–69. https://doi.org/10.2308/AJPT-2021-049 | | [46] | Kim, S. (2023). Digital procurement platforms and audit coordination: Evidence from South Korea. Government Information Quarterly, 40(1), 101742.

https://doi.org/10.1016/j.giq.2022.101742 |

[23, 24, 46] |

Source: Developed by the researcher based on governance and auditing literature.

3.5. Extended Hypotheses (H5–H7)

While the initial four hypotheses focus on direct relationships between network-governance dimensions and internal audit quality, comparative procurement systems exhibit additional mechanisms that shape audit performance. Particularly in emerging economies, contextual governance factors, regulatory strength, and institutional maturity may reinforce or weaken the effects identified earlier

| [34] | Haque, M. S., & De Vries, M. S. (2021). Public sector reform in developing countries: Governance perspectives. Public Administration and Development, 41(2), 73–86.

https://doi.org/10.1002/pad.1914 |

| [66] | Pérez-López, G., Prior, D., & Zafra-Gómez, J. L. (2021). Rethinking public sector performance through governance networks. Public Management Review, 23(9), 1321–1342.

https://doi.org/10.1080/14719037.2020.1730947 |

[34, 66]

. Building on these insights, this section develops three extended hypotheses.

H5: Relational Trust and Audit Evidence Quality

Relational trust enhances cooperation between procurement entities and auditors, increases the openness of disclosures, and reduces defensive behaviors during audits. In procurement settings—often characterized by procedural complexity—trust promotes voluntary sharing of sensitive documentation and facilitates more transparent audit trails

| [14] | Christopher, J., Goodwin, J., & Ahmed, K. (2022). Auditor independence and effectiveness in public sector audit committees. Public Money & Management, 42(8), 577–585. |

| [15] | Christopher, J., Sarens, G., & Leung, P. (2022). A critical analysis of the independence of the internal audit function: Evidence from public-sector organizations. Accounting, Auditing & Accountability Journal, 35(6), 1387–1411.

https://doi.org/10.1108/AAAJ-02-2021-5173 |

| [16] | Christopher, J., Sarens, G., & Leung, P. (2022). Debating the future of internal auditing: A global perspective. Accounting, Auditing & Accountability Journal, 35(2), 489–510.

https://doi.org/10.1108/AAAJ-10-2020-4988 |

[14-16]

.

H5: Higher levels of relational trust among governance-network actors are positively associated with audit evidence quality.

H6: Accountability Structures and Reporting Quality

Shared accountability mechanisms distribute oversight responsibilities across procurement actors, creating an environment that encourages compliance and facilitates improved reporting integrity. Procurement systems with strong accountability pathways—e.g., empowered audit committees, inter-ministerial oversight units—tend to implement audit recommendations more consistently.

H6: Stronger accountability structures within procurement networks are positively associated with audit reporting quality.

H7: Multi-Level Coordination and Audit Competence

Multi-level coordination across national, sectoral, and organizational levels enhances learning, standardization, and methodological development in internal auditing

| [11] | Christensen, T., & Lægreid, P. (2020). Organizational theory and public governance. Oxford University Press. |

| [13] | Christensen, T., & Lægreid, P. (2020). The Routledge handbook to accountability and welfare state reforms. Routledge. |

[11, 13]

. When procurement entities participate in joint training, shared digital platforms, or harmonized audit methodologies, the competence of audit teams improves

| [23] | Eulerich, M., Henseler, J., & Köhler, A. (2023). The internal audit function and firm performance: A competence-based view. Journal of International Accounting Research, 22(1), 75–94. |

| [24] | Eulerich, M., Kremin, J., & Wood, D. A. (2023). Internal audit quality: A systematic literature review and future research agenda. Auditing: A Journal of Practice & Theory, 42(1), 35–69. https://doi.org/10.2308/AJPT-2021-049 |

[23, 24]

.

H7: Multi-level coordination mechanisms are positively associated with internal audit competence.

Together, hypotheses H1–H7 form a relational, multi-actor understanding of audit quality, extending beyond single-entity models.

3.6. Cross-Country Considerations and Moderating Effects

Comparative procurement governance offers additional analytical leverage for understanding how network features translate into audit-quality outcomes. Procurement systems differ widely across countries in terms of regulatory maturity, institutional capacity, and network structures

| [62] | OECD. (2020). Public procurement and integrity: A framework for preventing corruption. OECD Publishing.

https://doi.org/10.1787/9c17cd9a-en |

| [89] | World Bank. (2022). Public procurement reform and institutional capacity building. World Bank Publications. |

[62, 89]

. These variations create moderating effects in the relationship between governance-network characteristics and internal audit quality.

3.6.1. Institutional Maturity as a Moderator

Countries with mature procurement institutions—such as South Korea, the Netherlands, and Denmark—exhibit stronger inter-organizational coordination and more consistent audit practices

. In such systems, network density and information exchange may exert a stronger positive effect on audit quality. Conversely, in emerging economies with fragmented oversight (e.g., Egypt, Jordan, Tunisia), the same network features may produce weaker or more variable results.

Thus, institutional maturity moderates the strength of network-to-quality relationships.

3.6.2. Regulatory Strength as a Moderator

Regulatory frameworks that clearly define procurement oversight roles amplify the effects of network coordination and accountability structures. When rules are ambiguous or weakly enforced, the positive effect of network governance on audit outcomes diminishes. Therefore, regulatory strength moderates the relationship between coordination and audit quality.

3.6.3. Cultural and Structural Differences

Cross-country variation also emerges from differences in administrative culture, transparency norms, and centralization levels

| [11] | Christensen, T., & Lægreid, P. (2020). Organizational theory and public governance. Oxford University Press. |

| [12] | Christensen, T., & Lægreid, P. (2020). The Ashgate research companion to new public management. Routledge.

https://doi.org/10.4324/9781315613305 |

| [13] | Christensen, T., & Lægreid, P. (2020). The Routledge handbook to accountability and welfare state reforms. Routledge. |

[11-13]

. In more centralized systems, network centrality may reflect formal authority, while in decentralized systems it may reflect relational brokerage. These structural and cultural variations influence how network features shape audit outcomes

.

Implication for Model Development

Given these moderating conditions, the comparative design of this study allows testing not only the direct effects (H1–H7) but also how these effects vary under different governance configurations. This strengthens external validity and advances theory on network-embedded audit mechanisms.

3.7. Summary of the Hypotheses Model

The hypotheses developed in this chapter synthesize insights from network governance theory, internal audit quality research, and comparative procurement governance. Collectively, the seven hypotheses represent a multidimensional and relational approach to understanding internal audit quality as a network-embedded outcome. Unlike traditional organizational models that confine audit determinants to internal structures or managerial factors, the proposed hypotheses emphasize inter-organizational linkages, information flows, trust dynamics, and coordination mechanisms

| [23] | Eulerich, M., Henseler, J., & Köhler, A. (2023). The internal audit function and firm performance: A competence-based view. Journal of International Accounting Research, 22(1), 75–94. |

| [24] | Eulerich, M., Kremin, J., & Wood, D. A. (2023). Internal audit quality: A systematic literature review and future research agenda. Auditing: A Journal of Practice & Theory, 42(1), 35–69. https://doi.org/10.2308/AJPT-2021-049 |

| [53] | Lenz, R., & Hahn, U. (2022). A synthesis of empirical internal audit effectiveness literature. Journal of Accounting Literature, 48, 100–122. https://doi.org/10.1016/j.acclit.2021.100606 |

[23, 24, 53]

.

Summary of Hypotheses:

H1: Network centrality → higher audit quality

H2: Network density → higher audit quality

H3: Coordination mechanisms → higher audit quality

H4: Information exchange → higher audit quality

H5: Relational trust → improved audit evidence quality

H6: Accountability structures → improved reporting quality

H7: Multi-level coordination → improved audit competence

The overarching logic is that procurement oversight outcomes depend on how well actors are connected, coordinated, and embedded within governance networks

| [2] | Ansell, C., & Torfing, J. (2021). Network governance and public innovation. Cambridge University Press. |

| [3] | Ansell, C., & Torfing, J. (2021). Public governance as co-creation: A strategy for revitalizing the public sector and rejuvenating democracy. Cambridge University Press.

https://doi.org/10.1017/9781108765381 |

[2, 3]

.

This moves the literature beyond internal, organization-centric models and expands the theoretical frontier toward relational accountability and network-informed audit quality.

Moreover, the inclusion of cross-country moderating effects—such as institutional maturity, regulatory strength, and cultural-institutional variation—strengthens the external validity of the model and contributes to comparative governance scholarship

.

3.8. Conceptual Model (Narrative + Figure Description)

To guide the empirical analysis in subsequent chapters, this study proposes a conceptual model integrating all theoretical components into a coherent analytical framework. The model reflects how network-governance dimensions influence the four core indicators of internal audit quality within public procurement systems, moderated by institutional and cross-country factors.

3.8.1. Narrative Description

The model positions procurement governance as a multilayered network where internal audit units interact with ministries, procurement authorities, regulators, oversight committees, and external auditors

. Within this ecosystem:

1) Network Centrality provides audit units with strategic influence, access to richer data, and stronger independence.

2) Network Density reflects cohesive relational structures that promote shared risk identification and harmonized audit practices.

3) Coordination Mechanisms enable cross-entity planning, reduce duplication, and improve implementation of audit recommendations.

4) Information Exchange ensures timely flow of procurement intelligence needed for accurate evidence evaluation.

5) Relational Trust encourages openness and reduces concealment during audit processes.

6) Accountability Structures reinforce reporting integrity and ensure follow-up implementation.

7) Multi-Level Coordination enhances learning, competence, and methodological consistency across procurement entities.

These network features interact to shape the four internal audit quality indicators:

1) Independence,

2) Competence,

3) Risk-Based Planning,

4) Reporting Quality.

The relationships are moderated by differences in institutional capacity, regulatory frameworks, and administrative culture across countries

| [11] | Christensen, T., & Lægreid, P. (2020). Organizational theory and public governance. Oxford University Press. |

| [12] | Christensen, T., & Lægreid, P. (2020). The Ashgate research companion to new public management. Routledge.

https://doi.org/10.4324/9781315613305 |

| [13] | Christensen, T., & Lægreid, P. (2020). The Routledge handbook to accountability and welfare state reforms. Routledge. |

| [57] | Mikušová, M. (2023). Internal audit quality and public-sector governance: Evidence from Central and Eastern Europe. Public Money & Management, 43(3), 215–224.

https://doi.org/10.1080/09540962.2022.2039547 |

[11-13, 57]

.

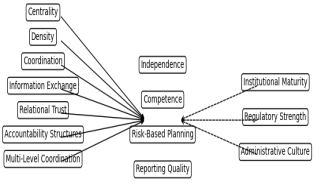

3.8.2. Conceptual Model – Figure Description

Figure 1 illustrates the proposed conceptual model linking network governance dimensions to internal audit quality indicators, with institutional and regulatory factors acting as moderating variables.

Figure 1. Conceptual Model of Network Governance and Internal Audit

1) Left side: Independent variables (network-governance dimensions)

a) Centrality

b) Density

c) Coordination

d) Information Exchange

e) Relational Trust

f) Accountability Structures

g) Multi-Level Coordination

2) Middle box: Internal audit quality indicators

a) Independence

b) Competence

c) Risk-Based Planning

d) Reporting Quality

3) Right side: Moderators

a) Institutional Maturity

b) Regulatory Strength

c) Administrative Culture

4) Arrows:

a) Directional arrows from each network dimension → each corresponding audit-quality indicator (reflecting H1–H7).

b) Moderation arrows crossing the relationships (showing contextual influence).

4. Research Methodology

4.1. Introduction