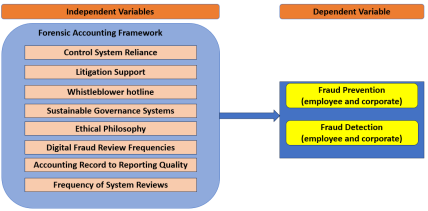

This study proposed a forensic accounting theory after examining how the impact of certain variables and their interplay on forensic accounting practices can contribute to developing integrated and robust fraud prevention strategies, enhance organizational accountability, and strengthen the overall integrity of financial and internal control systems. In literature, most studies on forensic accounting and fraud prevention have primarily focused on broader aspects such as governance, ethics, and accountability and are largely predicated on theories such as fraud diamond theory and agency theory that seek to understand the causes of fraud, highlighting the importance of forensic accounting in fraud prevention and detection, without suggesting practical forensic accounting frameworks. Also, the forensic accounting theory developed by Peterson Ozil in 2020 examines how the investigator’s attitude or mindset at the time of decision-making influences the outcomes of a forensic investigation. While these studies provide valuable insights into the overall context of fraud prevention, there is a scarcity of research on the specific forensic accounting processes that should be implemented to enhance the effectiveness of fraud prevention measures. This is the significant difference between the current study and previous studies. Therefore, the proposed Vutumu Forensic Accounting Theory serves as the guiding philosophy that underpins the integrated approach of combining control system reliance, litigation support, whistleblower hotlines, sustainable governance systems, ethical philosophy, digital fraud review frequencies, accounting record to reporting quality, and the frequency of system reviews, thereby enabling organizations to establish a proactive framework that addresses various dimensions of fraud prevention and detection. The implementation of the theory emerges as a formidable and comprehensive anti-fraud strategy, seamlessly integrating multiple elements to create a robust defense against fraudulent activities, safeguarding financial integrity, ethical conduct, and accountability within organizations. Furthermore, it is the researcher’s desire that this study serve as a foundation for further research and practical implementation of forensic accounting frameworks in strengthening the ability to detect and prevent fraud.

| Published in | International Journal of Accounting, Finance and Risk Management (Volume 9, Issue 4) |

| DOI | 10.11648/j.ijafrm.20240904.12 |

| Page(s) | 131-141 |

| Creative Commons |

This is an Open Access article, distributed under the terms of the Creative Commons Attribution 4.0 International License (http://creativecommons.org/licenses/by/4.0/), which permits unrestricted use, distribution and reproduction in any medium or format, provided the original work is properly cited. |

| Copyright |

Copyright © The Author(s), 2024. Published by Science Publishing Group |

Forensic Accounting, Fraud Prevention, Fraud Detection, Vutumu Forensic Accounting Theory, Internal Control

ACFE | Association of Certified Fraud Examiners |

AICPA | American Institute of Certified Public Accountants |

COSO | Committee of Sponsoring Organizations |

DMBs | Deposit Money Banks |

ICT | Information Communication Technology |

IT | Information Technology |

KPMG | Klynveld Peat Marwick Goerdeler |

PwC | PricewaterhouseCoopers International Limited |

R2R | Record to Reporting |

VFAT | Vutumu Forensic Accounting Theory |

| [1] | Shbeilat, M. K., & Alqatamin, R. M. (2022). Challenges and Forward-Looking Roles of Forensic Accounting in Combating Money Laundering: Evidence from the Developing Market. Journal of Governance and Regulation, 11(3), 103-120. |

| [2] | Ugbede, J., Ekpete, C., & Yahaya, A. (2021). Forensic Accounting as a Tool for Fraud Prevention in the Deposit Money Bank in Nigeria. (I. 2582-2306, Éd.) Journal of Applied Management and Advanced Research, 3(2), 50-59. |

| [3] | Agbo, E. I., & Obodoekwe, E. (2020). Correlation of Forensic Accounting Practice with Fraud Control and Corporate Governance in Nigerian Banks. Academic Journal of Current Research, 7(9), 128-144. |

| [4] | Eze, E., & Okoye, E. I. (2019). Forensic Accounting and Fraud Detection and Prevention in Imo State Public Sector. (2.-2. I.-2. ISSN, Éd.) Accounting and Taxation Review, 3(1), 12-26. |

| [5] | Dada, S. O., & Jimoh, F. B. (2020). Forensic Accounting and Financial Crimes in Nigerian Public Sector. Journal of Accounting and Taxation, 12(4), 118-125. |

| [6] | Ogunode, O. A., & Dada, S. O. (2022). Fraud Prevention Strategies: An Integrative Approach on the Role of Forensic Accounting. Archives of Business Research, 10(7), 34-50. |

| [7] | Basab, K. S. (2022). A Review of Forensic Accounting in India. Iconic Research and Engineering Journals, 5(12), 149-154. |

| [8] | Fiergbor, D. D. (2020). Managing Projects Using Forensic Accounting in Detection and Prevention of Fraud in Ghana. Global Economics Science, 1(2), 44-49. |

| [9] | Ozil, P. K. (2020). Forensic accounting theory. Finance, Insurance and Risk Management Theory and Practices, 1, 1-16. |

| [10] | Afriyie, S. O., Akomeah, M. O., Amoakohene, G., Ampimah, B. C., Oclooc, C. E., & Kyei, M. O. (2021). Forensic Accounting: A Novel Paradigm and Relevant Knowledge in Fraud Detection and Prevention. International Journal of Public Administration, 49(6), 615-624. |

| [11] | Ogiriki, T., & Appah, E. (2018). Forensic Accounting & Auditing Techniques on Public Sector Fraud in Nigeria. International Journal of African and Asian Studies, 47, 7-16. |

| [12] | Bangura, A. B. (2020). Forensic Accounting Techniques and Fraud Prevention in Sierra Leonean Deposit Money Banks. Asian Journal of Economics, Business and Accounting, 14(2), 20-50. |

| [13] | Bassey, B. E., & Ahonkhai, O. E. (2017). Effect of Forensic Accounting and Litigation Support on Fraud Detection of Banks in Nigeria. IOSR Journal of Business and Management (IOSR-JBM), 19(6), 56-60. |

| [14] | Alzoubi, A. B. (2023). Enhancing Internal Control Effectiveness through the Joint Role of Forensic Accounting and Corporate Governance. 2(27), 1-10. |

| [15] | Ugochukwu, N., & Okenwa, O. C. (2021). Effective Deploy of Digital Forensic Techniques and the Sustenance of Material Misstatement-Free Financial Reporting in Nigeria. Journal of Academic Research in Economics, 13(3), 442-470. |

| [16] | Olaniyan, N. O., Ekundayo, A. T., Oluwadare, O. E., & Bamisaye, T. O. (2021). Forensic accounting as an instrument for fraud detection and prevention in the public sector, Moderating on ministries Departments and agencies in Nigeria. Acta Scientiarum Polonorum Oeconomia, 20(1), 49-59. |

| [17] | Eneisik, G. E., & Ogbonna, F. I. (2021). Forensic Accountants as an Expert Witness in Nigeria: A Literature Reflection. International Journal of Economics and Financial Management, 6(2), 64-78. |

| [18] | Enofe, A., Ekpulu, G., & Ajala, T. O. (2015). The Litigation support of a forensic accountant involves the. European Scientific Journal, 11(7), 167-185. |

| [19] | Gbegi, D., & Habila, E. (2017). Effect of forensic accounting evidence on litigation services in the Nigerian judicial system. Nigerian Journal of Management Sciences, 6(1), 104-113. |

| [20] | Agu, S. I., & Okoye, E. I. (2019). Application of Forensic Accounting: A Bridge to Audit Expectation Gap in Nigerian Deposit Money Banks in Enugu Sta. International Journal of Science and Research (IJSR), 8(3), 46-55. |

| [21] | Okoye, E. I., & Ndubuisi, C. J. (2019). Forensic Accountant Expert Testimony and Objectivity of Forensic Investigation in Deposit Money Banks in Nigeria. EPRA International Journal of Multidisciplinary Research, 5(2), 124-132. |

| [22] | Dilshad, W., Irfan, M., Javed, S. M., & Aftab, Z. (2020). Empirical Evidence of Forensic Auditing and Whistleblower on Fraud Control, Organizational Performance; A Case Study of Public and Private Sectors of Pakistan. Journal of Accounting and Finance in Emerging Economies, 6(4), 955-966. |

| [23] | Albrecht, C. O., Holland, D. V., Skousen, B. R., & Skousen., C. J. (2018). The significance of whistleblowing as an anti-fraud measure. Journal of Forensic & Investigative Accounting, 10(1), 1-13. |

| [24] | PwC. (2012). Whistle blowing - Effective Means to Combat Economic Crime. Mumbai: PricewaterhouseCoopers Private Limited. |

| [25] | SOX. (2002). Sarbanes-Oxley Act of 2002 - Corporate responsibility. Washington: Senate and House of Representatives of the United States of America in Congress assembled. |

| [26] | ACFE. (2022). Occupational Fraud 2022: A Report to the Nations. Association of Certified Fraud Examiners. |

| [27] | Chen, J. (2023). Corporate Governance Definition: How It Works, Principles, and Examples. |

| [28] | ICAEW. (2023). What is corporate governance? Récupéré sur Institute of Chartered Accountants in England and Wales. |

| [29] | KPMG. (2018). Sustainable Business & Corporate Governance. Institute of Chartered Accountants of Nigeria – Stakeholders Dialogue 1, pp. 1-13. |

| [30] | Girau, E. A., Bujang, I., Jidwin, A. P., & Mohamed, N. (2021). Corporate Fraud: Undetectable Poison in the Thriving Economy. Journal of Legal, Ethical and Regulatory Issues, 24(4), 1-13. |

| [31] | Nkama, N. O., & Onoh, J. O. (2016). Forensic Accounting and Board Performance in the Nigerian Banking Industry. Journal of Accounting and Financial Management, 2(2), 29-43. |

| [32] | Singh, N., & Anjali. (2022). Integration of forensic accounting with corporate governance: A weapon to combat financial frauds. World Journal of Advanced Research and Reviews, 16(3), 299–307. Récupéré sur |

| [33] | Sims, R. R. (1992). The Challenge of Ethical Behavior in Organizations. Journal of Business Ethics, 11(7), 505-513. |

| [34] | Onuora, J., Akpoveta, E. B., & Agbomah, D. (2018). Public Sector Accounting Fraud in Nigeria. International Accounting and Taxation Research Group, 125-135. |

| [35] | Nnedu, S. C., & Aggreh, M. (2023). Perceived Ethical Climate and Forensic Accounting Services: Evidence From the Nigerian Public Sector. Britain International of Humanities and Social Sciences (BIoHS) Journal, 5(1), 23-31. |

| [36] | Ademola, L. S., Ch-Ahma, A. B., & Popoola, O. J. (2017). The Forensic Accountants' Skills and Ethics on Fraud Prevention in the Nigerian Public Sector. Academic Journal of Economic Studies, 4(3), 77-85. |

| [37] | Adejuwon, J. A., & Oge, A. S. (2021). Forensic Auditing, Internal Control and Ethical Behaviour of Employees in the Banking Industry of Nigeria. IOSR Journal of Economics and Finance (IOSR-JEF), 12(5), 20-28. |

| [38] | Kılıç, B. İ. (2020, 2 10). The Effects of Big Data on Forensic Accounting Practices and Education. Contemporary Issues in Audit Management and Forensic Accounting. Emerald Publishing Limited, Leeds, 102, 11-26. |

| [39] | Akinbowale, O. E. (2018). Information communication technology and forensic accounting in Nigeria. International Journal of Business and Finance Management Research, 6(1), 1-7. |

| [40] | PWC. (2022). PWC's Global Economic Crime and Fraud Survey 2022. PWC. |

| [41] | Boraine, A., & Ngaundje, L. D. (2019). The Fight against Cybercrime in Cameroon. International Journal of Computer (IJC), 35(1), 87-100. |

| [42] | Baz, R., Samsudin, R. S., & Che-Ahmad, A. (2017). The Role of Internal Control and Information Sharing in Preventing Fraud in the Saudi Banks. Journal of Accounting and Financial Management, 3(1), 7-13. |

| [43] | Prempeh, A., Osei, B., Osei, F., & Kuffour, E. O. (2022). Accounting Records Keeping and Growth of Small and Medium Enterprises in Kumasi Metropolitan. Open Journal of Social Sciences, 10(13), 184-207. |

| [44] | Krishna, R. (2021). 10 Ways to Optimize Your Record-To-Report Function. |

| [45] | Bachmid, F. S. (2016). The Effect of Accounting Information System Quality on Accounting Information Quality. Research Journal of Finance and Accounting, 20(7), 26-31. |

| [46] | Mardas, A., Zentar, S. M., & Loulid, M. (2022). La contribution du contrôle interne à la gouvernance des entreprises: Cas du secteur hôtelier. International Journal of Accounting, Finance, Auditing, Management and Economics - IJAFAME, 3(1-2), 121-133. |

| [47] | Ibrahim, M. (2017). Internal Control and Public Sector Revenue Generation in Nigeria: an Empirical Analysis. International Journal of Scientific Research in Social Sciences & Management Studies (IJSRSSMS), 2(1), 35-48. |

| [48] | Frazer, L. (2021). An empirical analysis of the effects of internal control on deviation. Journal of Behavioral Studies in Business in small restaurants, 10, 1-15. |

| [49] | Murti, A. K., & Kurniawan, T. (2019). Implementation and Impact of Internal Control in Preventing Fraud in The Public Sector. ICAS-PGS, 01-10. |

| [50] | Rahman, A. A., & Al-Dhaimesh, O. H. (2018). The effect of applying COSO-ERM model on reducing fraudulent financial reporting of commercial banks in Jordan. Banks and Bank Systems, 18(1), 107-115. |

| [51] | Erbuğa, G. S. (2022). Anti-fraud and Anti-Corruption Tools in the Struggle Against Fraudulent Acts in the Public Sector. Muhasebe Enstitüsü Dergisi - Journal of Accounting Institute, 67, 57-70. |

| [52] | Daigle, R. J., Tim Kizirian, L., & Sneathen, D. (2005). System Controls Reliability and Assessment Effort. International Journal of Auditing, 9, 79-90. |

| [53] | Ogwiji, J., & Lasisi, I. O. (2022). Internal Control System and Fraud Prevention of Quoted Financial Services Firms in Nigeria: A Smart PLS-SEM Approach. European Journal of Accounting, Auditing and Finance Research, 10(4), 1-33. |

| [54] | Oguda, N. J., Odhiambo, A., & Byaruhanga, J. (2015). Effect of Internal Control on Fraud Detection and Prevention in District Treasuries of Kakamega County. International Journal of Business and Management Invention, 4(1), 47-57. |

APA Style

Vutumu, A. (2024). Building the Foundation: Towards a Theoretical Framework for Forensic Accounting. International Journal of Accounting, Finance and Risk Management, 9(4), 131-141. https://doi.org/10.11648/j.ijafrm.20240904.12

ACS Style

Vutumu, A. Building the Foundation: Towards a Theoretical Framework for Forensic Accounting. Int. J. Account. Finance Risk Manag. 2024, 9(4), 131-141. doi: 10.11648/j.ijafrm.20240904.12

AMA Style

Vutumu A. Building the Foundation: Towards a Theoretical Framework for Forensic Accounting. Int J Account Finance Risk Manag. 2024;9(4):131-141. doi: 10.11648/j.ijafrm.20240904.12

@article{10.11648/j.ijafrm.20240904.12,

author = {Aloysius Vutumu},

title = {Building the Foundation: Towards a Theoretical Framework for Forensic Accounting},

journal = {International Journal of Accounting, Finance and Risk Management},

volume = {9},

number = {4},

pages = {131-141},

doi = {10.11648/j.ijafrm.20240904.12},

url = {https://doi.org/10.11648/j.ijafrm.20240904.12},

eprint = {https://article.sciencepublishinggroup.com/pdf/10.11648.j.ijafrm.20240904.12},

abstract = {This study proposed a forensic accounting theory after examining how the impact of certain variables and their interplay on forensic accounting practices can contribute to developing integrated and robust fraud prevention strategies, enhance organizational accountability, and strengthen the overall integrity of financial and internal control systems. In literature, most studies on forensic accounting and fraud prevention have primarily focused on broader aspects such as governance, ethics, and accountability and are largely predicated on theories such as fraud diamond theory and agency theory that seek to understand the causes of fraud, highlighting the importance of forensic accounting in fraud prevention and detection, without suggesting practical forensic accounting frameworks. Also, the forensic accounting theory developed by Peterson Ozil in 2020 examines how the investigator’s attitude or mindset at the time of decision-making influences the outcomes of a forensic investigation. While these studies provide valuable insights into the overall context of fraud prevention, there is a scarcity of research on the specific forensic accounting processes that should be implemented to enhance the effectiveness of fraud prevention measures. This is the significant difference between the current study and previous studies. Therefore, the proposed Vutumu Forensic Accounting Theory serves as the guiding philosophy that underpins the integrated approach of combining control system reliance, litigation support, whistleblower hotlines, sustainable governance systems, ethical philosophy, digital fraud review frequencies, accounting record to reporting quality, and the frequency of system reviews, thereby enabling organizations to establish a proactive framework that addresses various dimensions of fraud prevention and detection. The implementation of the theory emerges as a formidable and comprehensive anti-fraud strategy, seamlessly integrating multiple elements to create a robust defense against fraudulent activities, safeguarding financial integrity, ethical conduct, and accountability within organizations. Furthermore, it is the researcher’s desire that this study serve as a foundation for further research and practical implementation of forensic accounting frameworks in strengthening the ability to detect and prevent fraud.},

year = {2024}

}

TY - JOUR T1 - Building the Foundation: Towards a Theoretical Framework for Forensic Accounting AU - Aloysius Vutumu Y1 - 2024/10/29 PY - 2024 N1 - https://doi.org/10.11648/j.ijafrm.20240904.12 DO - 10.11648/j.ijafrm.20240904.12 T2 - International Journal of Accounting, Finance and Risk Management JF - International Journal of Accounting, Finance and Risk Management JO - International Journal of Accounting, Finance and Risk Management SP - 131 EP - 141 PB - Science Publishing Group SN - 2578-9376 UR - https://doi.org/10.11648/j.ijafrm.20240904.12 AB - This study proposed a forensic accounting theory after examining how the impact of certain variables and their interplay on forensic accounting practices can contribute to developing integrated and robust fraud prevention strategies, enhance organizational accountability, and strengthen the overall integrity of financial and internal control systems. In literature, most studies on forensic accounting and fraud prevention have primarily focused on broader aspects such as governance, ethics, and accountability and are largely predicated on theories such as fraud diamond theory and agency theory that seek to understand the causes of fraud, highlighting the importance of forensic accounting in fraud prevention and detection, without suggesting practical forensic accounting frameworks. Also, the forensic accounting theory developed by Peterson Ozil in 2020 examines how the investigator’s attitude or mindset at the time of decision-making influences the outcomes of a forensic investigation. While these studies provide valuable insights into the overall context of fraud prevention, there is a scarcity of research on the specific forensic accounting processes that should be implemented to enhance the effectiveness of fraud prevention measures. This is the significant difference between the current study and previous studies. Therefore, the proposed Vutumu Forensic Accounting Theory serves as the guiding philosophy that underpins the integrated approach of combining control system reliance, litigation support, whistleblower hotlines, sustainable governance systems, ethical philosophy, digital fraud review frequencies, accounting record to reporting quality, and the frequency of system reviews, thereby enabling organizations to establish a proactive framework that addresses various dimensions of fraud prevention and detection. The implementation of the theory emerges as a formidable and comprehensive anti-fraud strategy, seamlessly integrating multiple elements to create a robust defense against fraudulent activities, safeguarding financial integrity, ethical conduct, and accountability within organizations. Furthermore, it is the researcher’s desire that this study serve as a foundation for further research and practical implementation of forensic accounting frameworks in strengthening the ability to detect and prevent fraud. VL - 9 IS - 4 ER -

School of Business Management, Meridian Global University, Buea, Cameroon; School of Business, Charisma University, Billings, USA

Biography: Aloysius Vutumu holds a PhD in Forensic Accounting and Audit from Charisma University (2024) and an MSc in Accounting and Finance from Ahmadu Bello University (1999). He is currently a lecturer at Meridian Global University, with prior teaching roles at Ahmadu Bello University (1997-2000) and the University of Buea (2001-2004, 2015-2016), focusing on Financial Accounting, Governance, Controls and Ethics. Vutumu has been a Fellow of the Institute of Chartered Accountants of Nigeria (ICAN) since 2011 and serves as Chief Invigilator for its examinations in Cameroon, a Fellow of the Institute of Management Consultants (IMC) since 2000, and a Fellow of the International Institute of Certified Forensic Investigation Professionals since 2022. He leads the Angloxazone education subcommittee at the Institute of Chartered Accountants of Cameroon (ONECCA). In the industry, he is the Finance Director of Castel Group in Cameroon, having previously held senior positions at Diageo Plc and PriceWaterhouseCoopers.

Research Fields: Forensic Accounting and Investigation, Business Management, Business Finance, Governance and Controls, Auditing

Information