This study explores the impact of Human Capital Investment (HCI) on the financial performance of the top 25 companies listed on the Bombay Stock Exchange (BSE) over a ten-year period from 2014-15 to 2023-24. Financial performance is measured using three key indicators: Return on Assets (ROA), Return on Equity (ROE), and Return on Capital Employed (ROCE). Using regression and correlation analysis, the study identifies a significant positive relationship between HCI and all three financial metrics, with the strongest influence observed on ROCE. The findings suggest that companies investing consistently in employee training, development, and welfare tend to achieve higher profitability and operational efficiency. This underscores the strategic value of human capital as a critical asset in enhancing corporate performance. The study contributes to the growing body of evidence supporting the integration of HCI into core business strategy. It offers practical implications for corporate managers and policymakers to design and implement policies that prioritize human capital development as a means to achieve long-term financial sustainability and competitive advantage.

| Published in | European Business & Management (Volume 11, Issue 5) |

| DOI | 10.11648/j.ebm.20251105.12 |

| Page(s) | 95-103 |

| Creative Commons |

This is an Open Access article, distributed under the terms of the Creative Commons Attribution 4.0 International License (http://creativecommons.org/licenses/by/4.0/), which permits unrestricted use, distribution and reproduction in any medium or format, provided the original work is properly cited. |

| Copyright |

Copyright © The Author(s), 2025. Published by Science Publishing Group |

Human Capital Investment, Return on Equity, Return on Asset, Return on Capital Employed

Sl No. | Company Name | HCI | ROA | ROE | ROCE |

|---|---|---|---|---|---|

1 | Tata Consultancy Services Ltd. | 153305.61 | 27.20% | 38.60% | 48.28% |

2 | Infosys Ltd. | 92543.00 | 18.49% | 25.55% | 32.97% |

3 | State Bank Of India | 86982.18 | 0.50% | 8.20% | 6.22% |

4 | H C L Technologies Ltd. | 60299.05 | 16.73% | 24.20% | 28.66% |

5 | Wipro Ltd. It | 63471.78 | 11.91% | 18.34% | 22.44% |

6 | Coal India Ltd. | 73567.30 | 11.25% | 42.83% | 23.99% |

7 | Larsen & Toubro Ltd. | 39732.75 | 3.00% | 12.80% | 10.22% |

8 | Tata Motors Ltd. | 58917.77 | 0.97% | 0.76% | 9.33% |

9 | Tech Mahindra Ltd. | 34814.73 | 11.99% | 19.68% | 22.48% |

10 | Reliance Industries Ltd. | 24413.12 | 4.24% | 10.05% | 9.56% |

11 | Tata Steel Ltd. | 41673.41 | 2.45% | 6.62% | 10.99% |

12 | Ltimindtree Ltd. | 14850.60 | 17.12% | 23.63% | 30.10% |

13 | H D F C Bank Ltd. | 21324.74 | 1.73% | 16.17% | 7.38% |

14 | I C I C I Bank Ltd. | 18960.65 | 1.18% | 11.69% | 6.65% |

15 | Oil & Natural Gas Corp. Ltd. | 27114.56 | 5.39% | 11.52% | 12.33% |

16 | Bank Of Baroda | 15571.30 | 0.32% | 4.95% | 5.94% |

17 | Hindalco Industries Ltd. | 18863.40 | 2.73% | 7.38% | 8.77% |

18 | Axis Bank Ltd. | 11508.42 | 0.97% | 9.99% | 6.87% |

19 | Mahindra & Mahindra Ltd. | 17078.42 | 7.84% | 12.65% | 15.72% |

20 | Indian Oil Corp. Ltd. | 19684.73 | 4.79% | 13.84% | 15.32% |

21 | Bajaj FinServ Ltd. | 6719.51 | 1.64% | 13.41% | 12.33% |

22 | Kotak Mahindra Bank Ltd. | 9718.07 | 1.99% | 12.65% | 7.08% |

23 | Sun Pharmaceutical Inds. Ltd. | 10007.97 | 7.56% | 11.92% | 17.36% |

24 | N T P C Ltd. | 11879.42 | 4.29% | 11.27% | 8.21% |

25 | Grasim Industries Ltd. | 8532.89 | 2.56% | 7.58% | 8.65% |

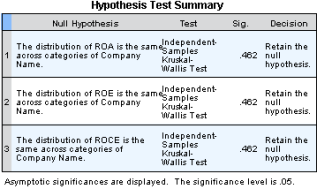

Tests of Normality | ||||||

|---|---|---|---|---|---|---|

Kolmogorov-Smirnova | Shapiro-Wilk | |||||

Statistic | df | Sig. | Statistic | df | Sig. | |

ROA | .217 | 25 | .004 | .821 | 25 | .001 |

ROE | .229 | 25 | .002 | .858 | 25 | .003 |

ROCE | .218 | 25 | .003 | .818 | 25 | .000 |

a. Lilliefors Significance Correction | ||||||

Correlations | ||||||

|---|---|---|---|---|---|---|

HCI | ROA | ROE | ROCE | |||

Spearman's rho | HCI | Correlation Coefficient | 1.000 | .362 | .345 | .418* |

Sig. (2-tailed) | . | .076 | .092 | .037 | ||

N | 25 | 25 | 25 | 25 | ||

ROA | Correlation Coefficient | .362 | 1.000 | .759** | .918** | |

Sig. (2-tailed) | .076 | . | .000 | .000 | ||

N | 25 | 25 | 25 | 25 | ||

ROE | Correlation Coefficient | .345 | .759** | 1.000 | .748** | |

Sig. (2-tailed) | .092 | .000 | . | .000 | ||

N | 25 | 25 | 25 | 25 | ||

ROCE | Correlation Coefficient | .418* | .918** | .748** | 1.000 | |

Sig. (2-tailed) | .037 | .000 | .000 | . | ||

N | 25 | 25 | 25 | 25 | ||

*. Correlation is significant at the 0.05 level (2-tailed). | ||||||

**. Correlation is significant at the 0.01 level (2-tailed). | ||||||

Variables Entered/Removeda | |||

|---|---|---|---|

Model | Variables Entered | Variables Removed | Method |

1 | Avg HCIb | . | Enter |

a. Dependent Variable: Avg ROA | |||

b. All requested variables entered. | |||

Model Summary | ||||

|---|---|---|---|---|

Model | R | R Square | Adjusted R Square | Std. Error of the Estimate |

1 | .661a | .437 | .412 | 5.364% |

a. Predictors: (Constant), Avg HCI | ||||

ANOVAa | ||||||

|---|---|---|---|---|---|---|

Model | Sum of Squares | df | Mean Square | F | Sig. | |

1 | Regression | 513.596 | 1 | 513.596 | 17.849 | .000b |

Residual | 661.829 | 23 | 28.775 | |||

Total | 1175.425 | 24 | ||||

a. Dependent Variable: Avg ROA | ||||||

b. Predictors: (Constant), Avg HCI | ||||||

Coefficientsa | ||||||||

|---|---|---|---|---|---|---|---|---|

Model | Unstandardized Coefficients | Standardized Coefficients | t | Sig. | Collinearity Statistics | |||

B | Std. Error | Beta | Tolerance | VIF | ||||

1 | (Constant) | 8.743 | 2.364 | 3.699 | .001 | |||

Avg HCI | .000 | .000 | .602 | 3.612 | .001 | 1.000 | 1.000 | |

a. Dependent Variable: Avg ROE | ||||||||

Variables Entered/Removeda | |||

|---|---|---|---|

Model | Variables Entered | Variables Removed | Method |

1 | Avg HCIb | . | Enter |

a. Dependent Variable: Avg ROE | |||

b. All requested variables entered. | |||

Model Summary | ||||

|---|---|---|---|---|

Model | R | R Square | Adjusted R Square | Std. Error of the Estimate |

1 | .602a | .362 | .334 | 7.963% |

a. Predictors: (Constant), Avg HCI | ||||

ANOVAa | ||||||

|---|---|---|---|---|---|---|

Model | Sum of Squares | df | Mean Square | F | Sig. | |

1 | Regression | 827.300 | 1 | 827.300 | 13.047 | .001b |

Residual | 1458.416 | 23 | 63.409 | |||

Total | 2285.716 | 24 | ||||

a. Dependent Variable: Avg ROE | ||||||

b. Predictors: (Constant), Avg HCI | ||||||

Coefficientsa | ||||||||

|---|---|---|---|---|---|---|---|---|

Model | Unstandardized Coefficients | Standardized Coefficients | t | Sig. | Collinearity Statistics | |||

B | Std. Error | Beta | Tolerance | VIF | ||||

1 | (Constant) | 8.743 | 2.364 | 3.699 | .001 | |||

Avg HCI | .000 | .000 | .602 | 3.612 | .001 | 1.000 | 1.000 | |

a. Dependent Variable: Avg ROE | ||||||||

Variables Entered/Removeda | |||

|---|---|---|---|

Model | Variables Entered | Variables Removed | Method |

1 | Avg HCIb | . | Enter |

a. Dependent Variable: Avg ROCE | |||

b. All requested variables entered. | |||

Model Summary | ||||

|---|---|---|---|---|

Model | R | R Square | Adjusted R Square | Std. Error of the Estimate |

1 | .696a | .485 | .462 | 7.767% |

a. Predictors: (Constant), Avg HCI | ||||

ANOVAa | ||||||

|---|---|---|---|---|---|---|

Model | Sum of Squares | df | Mean Square | F | Sig. | |

1 | Regression | 1304.979 | 1 | 1304.979 | 21.633 | .000b |

Residual | 1387.462 | 23 | 60.324 | |||

Total | 2692.441 | 24 | ||||

a. Dependent Variable: Avg ROCE | ||||||

b. Predictors: (Constant), Avg HCI | ||||||

Coeffi cientsa | ||||||||

|---|---|---|---|---|---|---|---|---|

Model | Unstandardized Coefficients | Standardized Coefficients | t | Sig. | Collinearity Statistics | |||

B | Std. Error | Beta | Tolerance | VIF | ||||

1 | (Constant) | 7.590 | 2.306 | 3.292 | .003 | |||

Avg HCI | .000 | .000 | .696 | 4.651 | .000 | 1.000 | 1.000 | |

a. Dependent Variable: Avg ROCE | ||||||||

HCI | Human Capital Investment |

BSE | Bombay Stock Exchange |

ROA | Return on Assets |

ROI | Return on Investment |

ROCE | Return on Capital Employed |

| [1] | Moin, H. ul, & Qureshi, N. A. (2023). The Impact of Human Resource Accounting on Profitability: A Study of Listed Textile Firms on PSX. International Journal of Management Research and Emerging Sciences, 13(4), Article 4. |

| [2] | Ozioma, G. A., & P. (PhD), U. F. N. (2021). The Effect Of Human Resource Accounting (Hra) On Profitability: A Study Of Selected Firms Quoted On The Nigerian Stock Exchange. EPRA International Journal of Economics, Business and Management Studies (EBMS), 8(11), Article 11. |

| [3] | Parham, S., & Heling, G. (2015). The Relationship between Human Capital Efficiency and Financial Performance of Dutch Production Companies. Research Journal of Finance and Accounting, 6. |

| [4] | Kai Ming Au, A., Altman, Y., & Roussel, J. (2008). Employee training needs and perceived value of training in the Pearl River Delta of China: A human capital development approach. Journal of European Industrial Training, 32(1), 19-31. |

| [5] | Masuluke, M. F., & Ngwakwe, C. C. (2018). Relationship Between Human Capital Investments And Firm’s Net Profit. 08(01). |

| [6] | Onyekwelu, U., Fidelia, P., Scholar, & Osisioma, B. (2015). Impact Of Human Capital Accounting On Corporate Financial Performance-A Study Of Selected Banks In Nigeria. |

| [7] | Osho, A., & Obiazonwa, J. (2018). Human Capital Expenditure and Financial Performance of Quoted Manufacturing Companies in Port Harcourt. |

| [8] | Perera, A., & Thrikawala, S. (2012). Impact of Human Capital Investment on Firm Financial Performances: An Empirical Study of Companies in Sri Lanka. International Proceedings of Economics Development & Research, 54, 11-16. |

| [9] | Talan, G., Sharma, G. D., & Sehrawat, K. (2017). The Relationship between HR Expenditure and Firm’s Performance: Case of S&P BSE SENSEX 30 Companies. Global Journal of Enterprise Information System, 9(3), 59-64. |

| [10] | Ukenna, S., Ijeoma, N., Anionwu, C., & Olise, M. (2010). Effect of investment in human capital development on organisational performance: Empirical examination of the perception of small business owners in Nigeria. European Journal of Economics, Finance and Administrative Sciences, 93-107. |

APA Style

Bhosale, A., Tamragundi, A. (2025). The Impact of Human Capital Investment on the Financial Performance of Selected BSE-Listed Companies. European Business & Management, 11(5), 95-103. https://doi.org/10.11648/j.ebm.20251105.12

ACS Style

Bhosale, A.; Tamragundi, A. The Impact of Human Capital Investment on the Financial Performance of Selected BSE-Listed Companies. Eur. Bus. Manag. 2025, 11(5), 95-103. doi: 10.11648/j.ebm.20251105.12

@article{10.11648/j.ebm.20251105.12,

author = {Arun Bhosale and Anjanadevi Tamragundi},

title = {The Impact of Human Capital Investment on the Financial Performance of Selected BSE-Listed Companies

},

journal = {European Business & Management},

volume = {11},

number = {5},

pages = {95-103},

doi = {10.11648/j.ebm.20251105.12},

url = {https://doi.org/10.11648/j.ebm.20251105.12},

eprint = {https://article.sciencepublishinggroup.com/pdf/10.11648.j.ebm.20251105.12},

abstract = {This study explores the impact of Human Capital Investment (HCI) on the financial performance of the top 25 companies listed on the Bombay Stock Exchange (BSE) over a ten-year period from 2014-15 to 2023-24. Financial performance is measured using three key indicators: Return on Assets (ROA), Return on Equity (ROE), and Return on Capital Employed (ROCE). Using regression and correlation analysis, the study identifies a significant positive relationship between HCI and all three financial metrics, with the strongest influence observed on ROCE. The findings suggest that companies investing consistently in employee training, development, and welfare tend to achieve higher profitability and operational efficiency. This underscores the strategic value of human capital as a critical asset in enhancing corporate performance. The study contributes to the growing body of evidence supporting the integration of HCI into core business strategy. It offers practical implications for corporate managers and policymakers to design and implement policies that prioritize human capital development as a means to achieve long-term financial sustainability and competitive advantage.

},

year = {2025}

}

TY - JOUR T1 - The Impact of Human Capital Investment on the Financial Performance of Selected BSE-Listed Companies AU - Arun Bhosale AU - Anjanadevi Tamragundi Y1 - 2025/09/25 PY - 2025 N1 - https://doi.org/10.11648/j.ebm.20251105.12 DO - 10.11648/j.ebm.20251105.12 T2 - European Business & Management JF - European Business & Management JO - European Business & Management SP - 95 EP - 103 PB - Science Publishing Group SN - 2575-5811 UR - https://doi.org/10.11648/j.ebm.20251105.12 AB - This study explores the impact of Human Capital Investment (HCI) on the financial performance of the top 25 companies listed on the Bombay Stock Exchange (BSE) over a ten-year period from 2014-15 to 2023-24. Financial performance is measured using three key indicators: Return on Assets (ROA), Return on Equity (ROE), and Return on Capital Employed (ROCE). Using regression and correlation analysis, the study identifies a significant positive relationship between HCI and all three financial metrics, with the strongest influence observed on ROCE. The findings suggest that companies investing consistently in employee training, development, and welfare tend to achieve higher profitability and operational efficiency. This underscores the strategic value of human capital as a critical asset in enhancing corporate performance. The study contributes to the growing body of evidence supporting the integration of HCI into core business strategy. It offers practical implications for corporate managers and policymakers to design and implement policies that prioritize human capital development as a means to achieve long-term financial sustainability and competitive advantage. VL - 11 IS - 5 ER -

Post Graduate Department of Studies in Commerce, Karnatak University, Dharwad, India

Post Graduate Department of Studies in Commerce, Karnatak University, Dharwad, India

Information